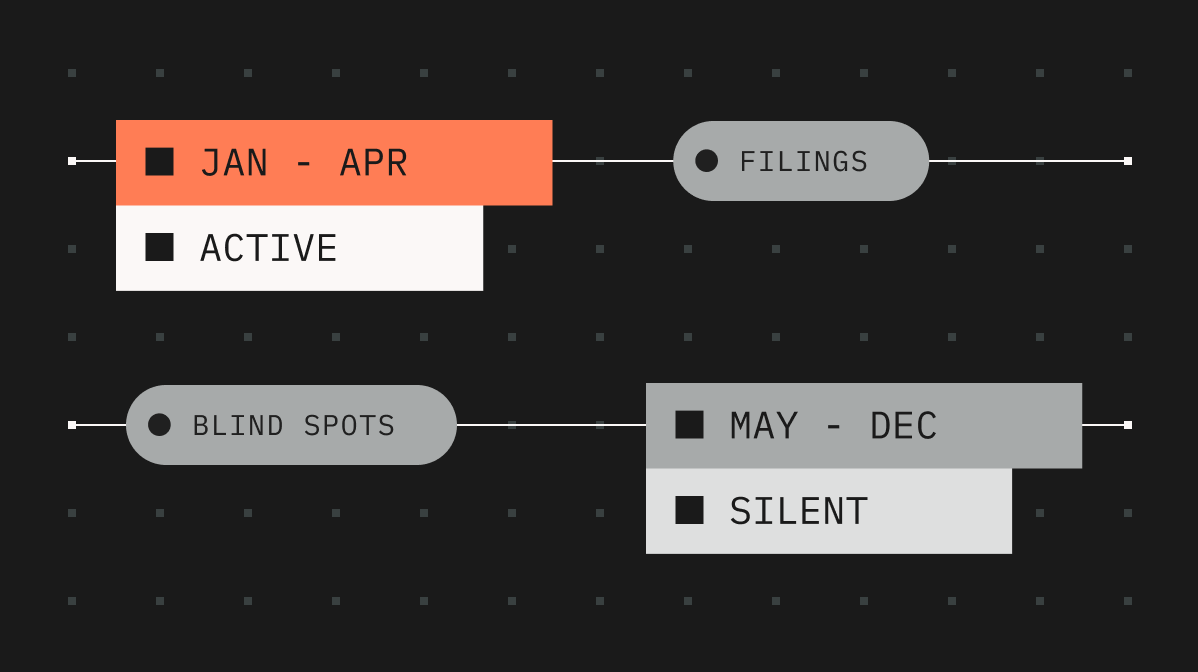

Your tax provider calls in September, or maybe October. That's when things start moving: signature packets, engagement letters, preliminary timeline discussions.

For the next few months, there's moderate activity: a request for documents here, a clarifying question there. Then in February and especially March, it accelerates as the March 15 partnership filing deadline approaches. The pressure often continues into early April as LPs and their accountants work toward their own filing deadlines, and then, after returns are filed and K‑1s go out, the relationship goes quiet again.

Until September.

This is the standard cadence for a VC fund with a traditional tax provider: two months of high activity, two months of moderate activity, eight months of silence. Your tax provider isn't thinking about your fund between May and August. Neither, probably, are you…at least not in a tax context.

That seasonal rhythm has a cost that most fund managers don't account for until they've already paid it.

What happens in the off-season

During the eight months your tax provider isn't engaged, your fund keeps generating activity. The work of preparing annual books specifically to share with an external team is the default model. It's also the problem.

Capital calls go out. Distributions get processed. New investments close. Portfolio companies raise new rounds, changing valuations and potentially affecting holding periods. Management fee calculations run each quarter. Some of these events have direct tax implications—implications that will not surface until your tax provider gets their first export of the year and starts asking questions.

By then, several things may have already gone wrong:

Timing decisions made without tax input. The decision to close a secondary sale or realize a gain in December versus January can have material implications for your LPs' tax liability. The structure of a co‑investment might affect carried interest treatment. If your tax provider isn't in the conversation when these decisions are being made, they can only react to them after the fact.

Errors that compound over time. When data isn't reviewed continuously, mistakes that would have been caught in month three don't surface until month thirteen. The longer an error sits in your books before your tax team sees it, the more work it takes to correct—and the more it can affect adjacent line items.

LP surprises. LPs who receive K-1s showing unexpected income or loss allocations—especially ones that weren't flagged in advance—have a legitimate grievance. Most tax providers do post-filing calls. Few do proactive mid-year briefings. If your LP relationship depends on no surprises at K-1 time, you're relying on the accuracy of a year-end snapshot rather than continuous oversight.

The difference between a vendor and a platform

The seasonal engagement model makes sense for a standalone tax vendor. Their value is in technical expertise: tax code knowledge, filing accuracy, and audit support. They don't need year-round access to your fund data to provide that expertise; they just need the year-end export.

But that model breaks down when you consider what you're leaving on the table.

A tax platform connected to your fund administration data doesn't have an off-season. The data is live. Your capital activity, your investment schedule, your valuation history—it's all current, all the time. Carta's tax team isn't waiting for an export to start understanding your fund. They're positioned to provide year-round guidance because they already have year-round visibility.

This changes the nature of the relationship. Instead of an annual vendor engagement that follows a predictable February-to-September cycle, you have a continuous partnership with a team that knows your fund throughout the year—not just during return preparation season.

Visibility isn't a bonus feature

One of the most common pain points fund managers describe is the absence of status visibility during tax season itself. Your returns are in process. You have no idea where they are. An LP calls. You have to ask. Your tax provider responds in a day or two. You relay the message.

Carta’s Tax Dashboard addresses this at the most basic level: it shows you where every return stands, in real time, without requiring you to contact your tax provider for an update. Expected due dates are visible. Current stages are tracked. Outstanding tasks—documents still needed, approvals still pending—are surfaced before they become delays.

This matters especially when you're managing multiple funds with staggered timelines. Instead of maintaining a mental model of where each entity is in its return preparation cycle, you have a single view.

But the deeper value of that visibility isn't convenience. It's the confidence that comes from having real information rather than estimates. When your LP asks when they'll receive their K-1, you can answer with a specific date rather than a guess. When your accountant asks whether the extension has been filed, you can check rather than assume.

Gifty Minhas from Carta's Fund Tax Operations team put it plainly: "Prior to the Tax Dashboard existing, clients would have to email for the status of returns and when they can receive them. With the dashboard, clients can track the status and ownership of all their returns in one place, providing visibility into the progress of the return and whether action is needed from you or your LPs.”

That shift—from reactive inquiry to proactive visibility—is one of the most concrete differences between an integrated platform and a seasonal vendor relationship.

What LPs experience on the other side

Your limited partners have their own tax timelines. Many of them are institutions with downstream reporting obligations. Family offices are coordinating multiple K-1s across multiple fund investments. Endowments and foundations have their own fiscal years and filing requirements.

When your fund's K-1s arrive late, your LPs absorb the delay in their own processes. But the earlier, less visible problem is the uncertainty. LPs don't know when to expect documents until you tell them, and you don't know until you ask your tax provider.

The LP portal in Carta's platform places K-1s in the same location where LPs already access their capital call notices and distribution statements. When their K-1 is ready, it appears there—no separate email, no password-protected PDF delivery service, no questions about whether they received it. It's available through the same interface they've been using throughout the life of the fund.

This isn't a minor convenience. LPs who manage multiple fund investments track a large volume of documents across a calendar year. Reducing the number of separate touchpoints—and eliminating one more communication loop during an already demanding tax season—matters to the administrators and CFOs on the other end.

A more useful question to ask your tax provider

The standard evaluation questions for a tax provider are: What are your rates? What's your turnaround time? Do you have experience with VC fund structures? These are necessary questions, but they're not sufficient ones.

The questions that reveal more about structural cost are:

How will your team access my fund data, and at what cadence?

What happens if I make a strategic decision in Q3 that has tax implications—how would I loop you in?

When I ask where my returns stand in February, what does that answer come from and how long will it take?

How many of my peers' K-1s did you deliver before the original March filing deadline last year?

The answers reveal whether you're evaluating a vendor or a platform—a team engaging with your fund seasonally, or one maintaining year-round visibility into your fund's activity.

The structural case for integration

The three posts in this series have described the same underlying problem from three different angles: K-1 delays driven by sequential handoffs; coordination overhead between two disconnected systems; and a seasonal engagement model that leaves tax questions unanswered for eight months of the year.

All three trace back to the same structural choice: running fund administration and tax preparation as separate functions, on separate systems, with a data handoff at year-end.

The alternative is a single platform where the fund data that powers your accounting also powers your tax preparation—where your books and your returns are maintained by teams working from the same underlying information, without the exports, the catch-ups, or the silence.

That's not a new idea in enterprise software. Integration has driven consolidation in every other area of financial operations. Fund tax has been slower to follow, partly because the traditional model has worked adequately, and partly because switching providers during tax season isn't something anyone wants to do.

But adequately isn't the same as optimally. And the cost of running two systems—in delays, in coordination time, in lost visibility—is real, even when it doesn't show up in any single fee agreement.

This is the final post in our series on the hidden cost of traditional tax providers. Read about why your K-1s are late and the meeting you're not counting as a tax cost.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.