A year ago, it appeared that the post-pandemic wave of bridge rounds that washed over the venture capital industry in 2022 and 2023 was beginning to abate.

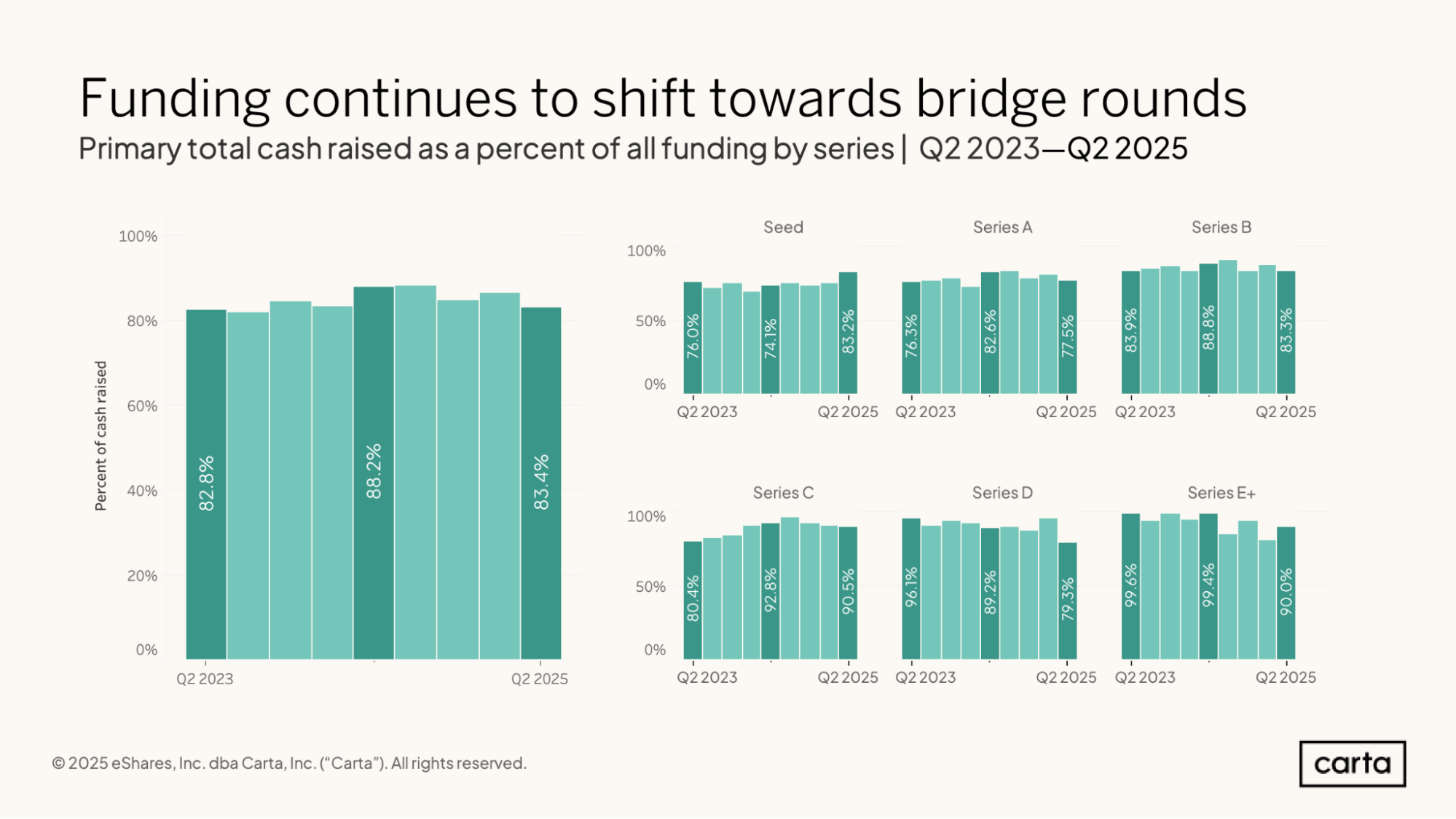

But the past 12 months proved any such presumptions premature. During the second quarter of 2025, about 16.6% of all cash raised by startups on Carta came via bridge rounds, up from an 11.8% rate a year earlier, according to Carta’s latest State of Private Markets report.

Most startup fundraising occurs through primary rounds, often with formal round names such as a Series A or Series B. These are also called priced rounds, because they involve the company receiving a new valuation. Bridge rounds, also called extension rounds, usually don’t involve a new valuation. Instead, in a typical bridge round, the company issues convertible notes to existing or new investors, or some of a company’s existing investors provide new capital structured as an add-on to the prior to round, to serve as a financial “bridge” to the next primary funding event.

During the venture bull market of 2021, bridge rounds typically accounted for less than 10% of all cash raised on Carta during any given quarter. Even after this recent increase, they’re still relatively uncommon. But it’s clear that bridge rounds have become an increasingly popular option in the startup toolkit.

In Q2, bridge rounds were the most common among Series A startups, where they accounted for 22.5% of cash raised (with the other 77.5% coming from primary rounds). Bridge rounds were also the source of more than 20% of all Q2 fundraising at Series D.

Why bridge rounds are still on the rise

In many instances, bridge rounds serve as a strategic alternative for startups that might have originally planned to pursue an exit or raise a new round of primary funding. In the past two years, both of these markets have tightened considerably. Annual IPO count in the U.S. fell by 62% from 2021 to 2024, while the annual count of new venture rounds declined by 36%.

These two slowdowns are linked. In general, investors across both public and private markets have raised their standard for what qualifies as an attractive investment. These reductions in other kinds of deal activity are likely linked to the increase in bridge rounds, too.

“The rise of bridge rounds over the last several years ultimately stems from reduced exit activity,” says Marc Schröder, founding and managing partner at MGV, an early-stage venture fund that focuses on the SaaS sector. “IPOs have become scarcer, and the trickle-down effect has been tighter capital at the growth stages for most companies.”

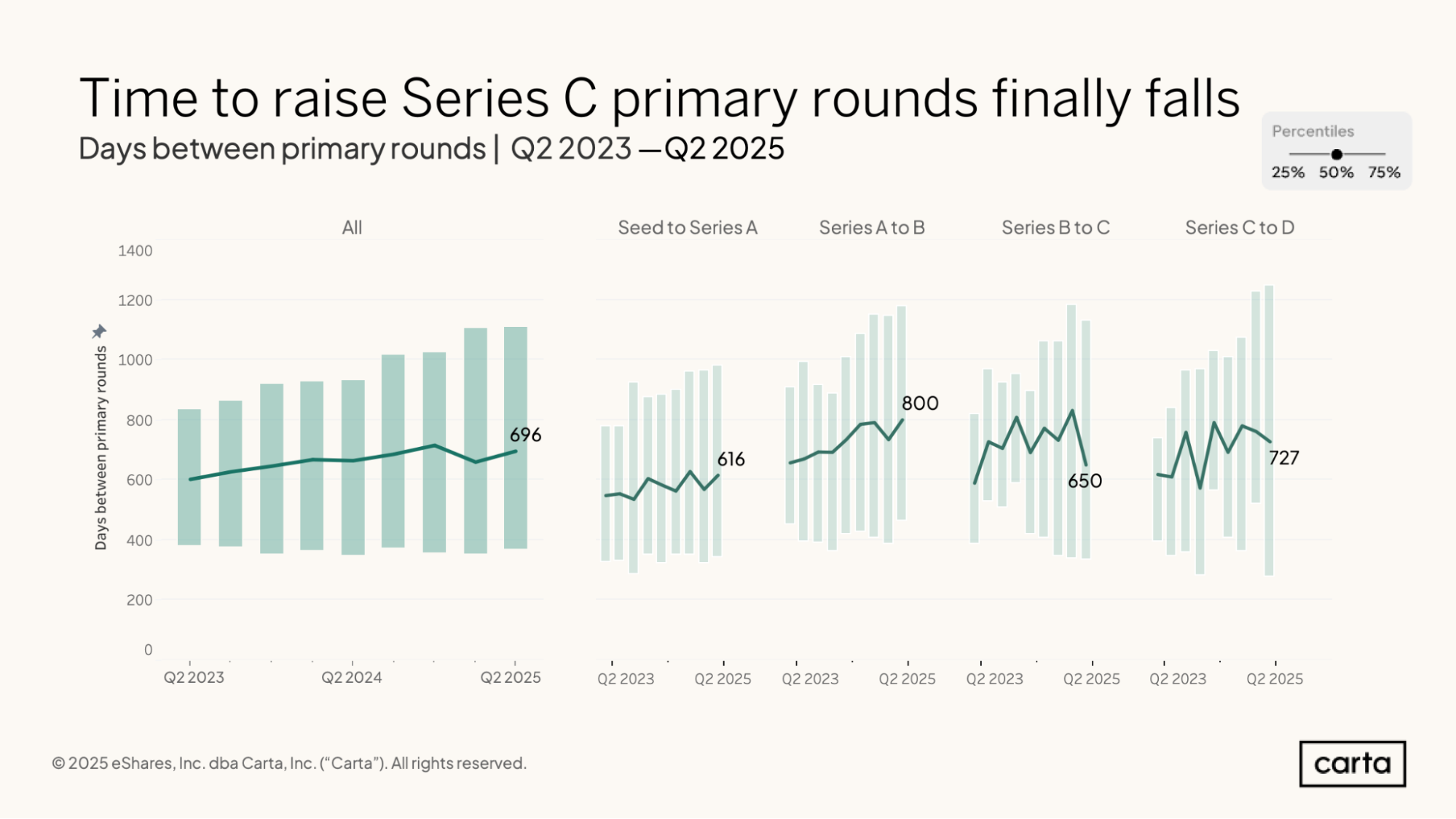

Raising a bridge round can allow a startup to restock its coffers and extend its fundraising timeline as it waits for more favorable market conditions. It makes sense, then, that as bridge rounds have grown more prominent, the typical time between primary funding rounds has been trending up.

Across all fundraising stages, the median interval between primary funding rounds was 696 days in Q2, the equivalent of about 23 months. Two years ago, the median wait between rounds was about three months shorter, at nearly 600 days.

“A lot of companies in the last two years tried to beef up their runway if they needed to by doing extensions or bridge rounds,” says Felix Hartmann, founder and managing partner at Hartmann Capital.

The future of bridge rounds

Because bridge rounds are often not a company’s first option, they have historically had something of a negative connotation among companies and investors. As bridge rounds have become more common, Schröder believes that they’ve also become more accepted.

“While many founders remain wary of bridge rounds, the truth is that the old stigma around them making it harder to raise subsequent rounds has lessened,” Schröder says. “If you’re a startup that needs some additional runway to build up your ARR and surpass that elevated growth round bar, you should probably go for it. Investors will be interested if you’ve got strong traction, regardless of whether it took a bridge round to get there.”

But that doesn’t mean this is a permanent change in the startup landscape. Hartmann believes that there is a causal link between recent market conditions and the rise in bridge rounds. In his view, when the markets for exits and VC-backed valuations warm back up, the percentage of capital raised that comes from bridge rounds will decline.

Why? Because IPOs and other exits are the main way that VC funds generate DPI and return capital to their LPs. And new primary rounds are still the main pathway to an exit. Once more companies are able to find an exit or raise new primary funding on attractive terms, they will, simply because it is more profitable for them and their investors.

“I don’t see this becoming an industry standard for the very simple reason that companies need to go up for VCs to make money,” Hartmann says. “Eventually, they need DPI.”

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.