In several different respects, the startup funding ecosystem is experiencing a bifurcation, with the gap between the bottom and the top of the market growing wider and wider.

This trend extends to the pre-seed funding market, where the breakdown of deal sizes is becoming both more bottom-heavy and more top-heavy, assuming a barbell shape—a barbell with more new weight being added to either end with every new quarter.

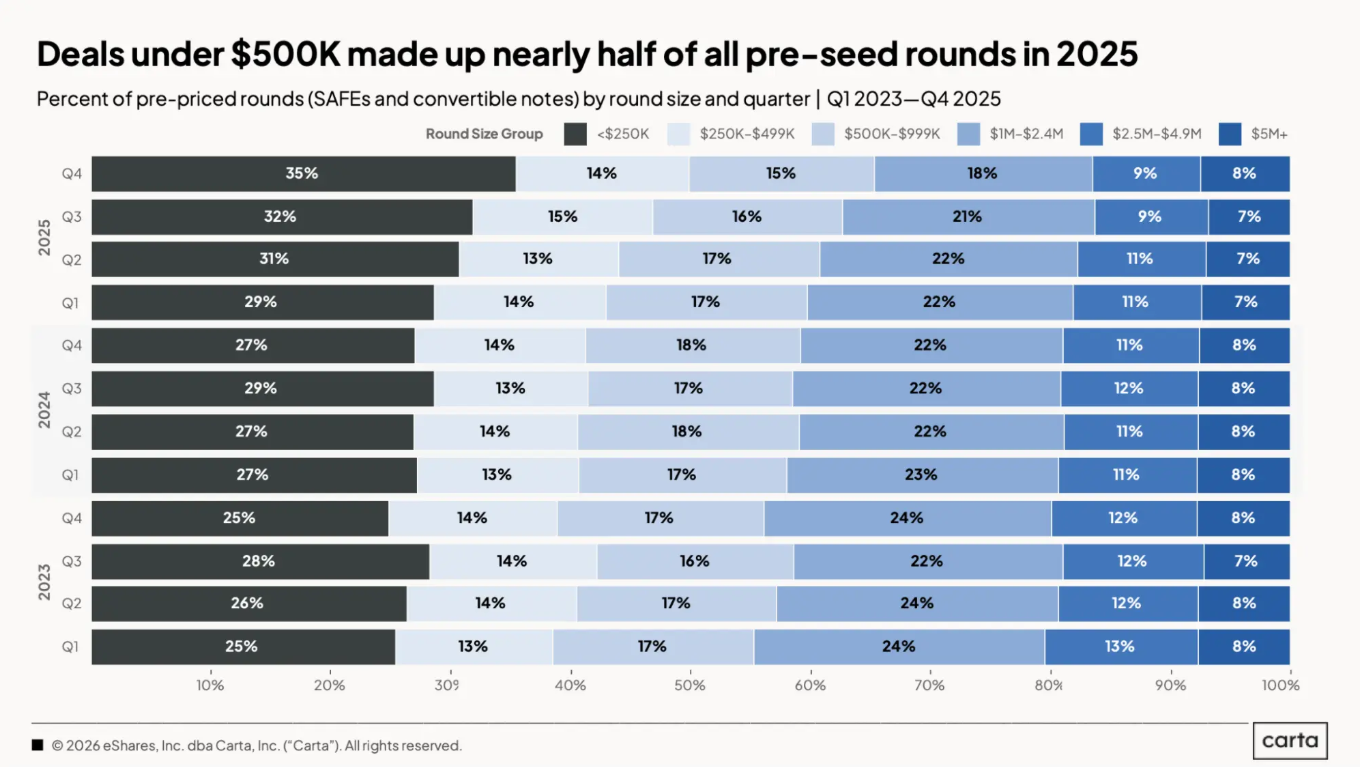

At the low end, the proportion of pre-seed rounds smaller than $250,000 raised on Carta climbed steadily throughout 2025, reaching a new high of 35% in Q4. And while the portion of rounds larger than $5 million remained mostly flat—landing at 8% in Q4—the size of the largest pre-seed financings keeps increasing. Among all SAFEs that raised at least $1 million, the average deal size on Carta reached $1.4 million in 2025, up from $1.1 million in 2024.

Pre-seed fundings have always been distributed unevenly, rather than landing along a smooth bell curve. But longtime players in the space say that this lopsided nature of the pre-seed market is intensifying.

“It has been this way since the market existed,” says Alexander Korchevsky, managing partner at I2BF Global Ventures and a co-founder of the Pre-Seed to Succeed program for early-stage startups. “It’s nothing new. But it has gone to further extremes.”

How AI is shaping pre-seed funding needs

One of the drivers of this ongoing shift in the pre-seed market is, of course, AI. The rapid rise of new AI tools and technologies is factoring into changes on both sides of the barbell.

In some cases, AI is allowing young startups to achieve more with less funding, reducing requirements for pre-seed cash. This is most prevalent in sectors that are built on software, such as SaaS and fintech. In other cases, the significant capital requirements of certain AI-based business models are leading to some mammoth pre-seed rounds.

“Different categories have different needs,” says Samyr Laine, co-founder of early-stage firm Freedom Trail Capital. “If you’re in AI, healthtech, defense tech, to get those off the ground can be a lot more capital-intensive. So you need more money and larger checks, and there are also more people throwing big dollars out there.”

These two ends of the barbell tend to rely on different investor archetypes, Laine says. For the smallest pre-seed rounds, startups frequently tap into funding from their friends and family and professional networks. The largest rounds, meanwhile, are much more likely to draw capital from professional investors.

“The larger end of that pre-seed market, you’re getting more institutional investors, funds, and family offices and the like,” Laine says. “Sometimes, you’re getting the more seasoned institutional investors, the bigger names.”

Regardless of size, SAFEs are the pre-seed standard

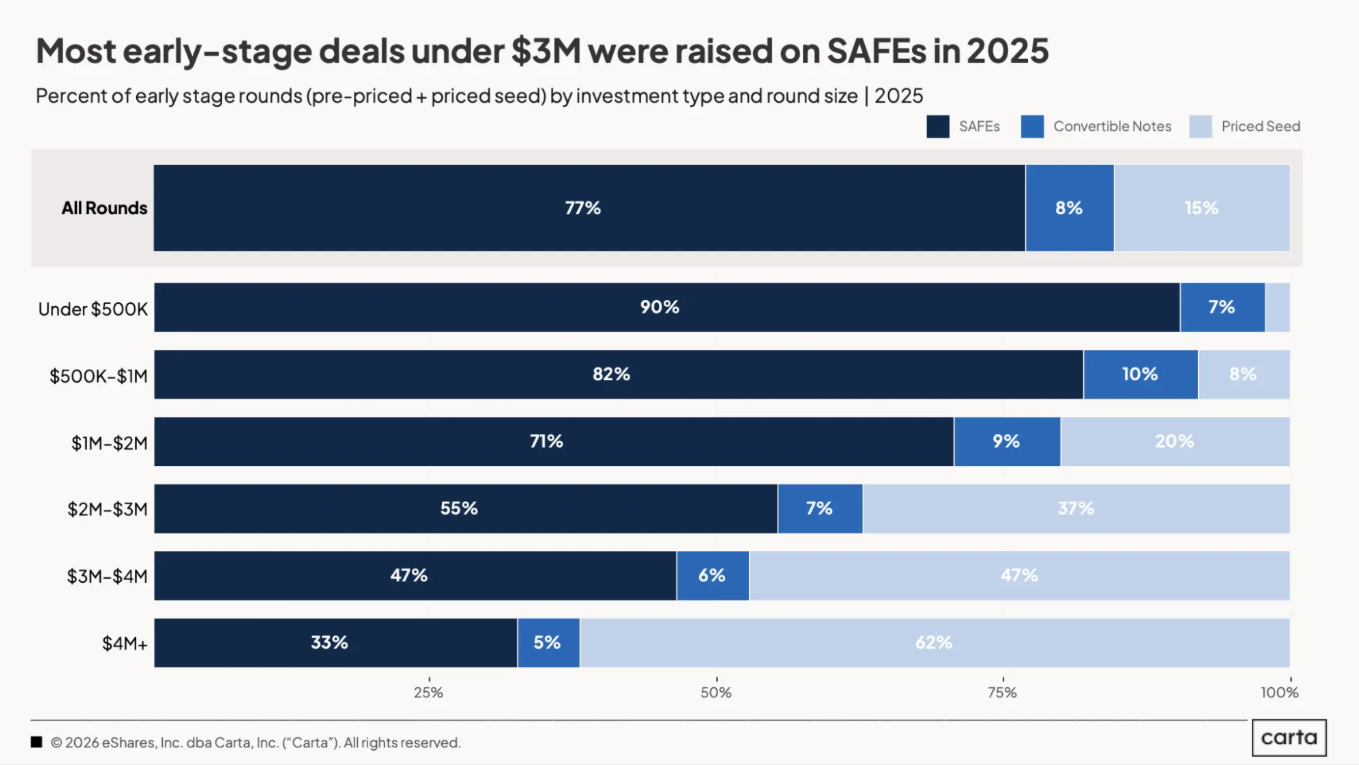

At either end of the spectrum, pre-seed financings are much more likely to be structured as SAFEs, rather than convertible notes. In 2025, 97% of rounds on Carta that raised less than $500,00 were pre-seed rounds, and 93% of those pre-seed rounds were on SAFEs. Among pre-seed deals larger than $4 million, about 87% were structured as SAFEs.

Four or five years ago, SAFEs had already emerged as the most common pre-seed instrument, but convertible notes were also still a popular option. Today, investors have come to accept SAFEs as the industry standard.

“Nowadays, a lot more institutional investors have gotten a lot more comfortable being on the SAFE,” Laine says. “When a founder says, ‘Let’s run a SAFE, and here’s the valuation cap,’ people are blinking a lot less.”

As round sizes increase, some founders have a choice to make: Raise a pre-seed round, or move onto a priced seed round at a set valuation?

Once the size of a financing reaches $3 million, priced rounds are just as common as pre-priced rounds. If a startup is raising more than $4 million, priced rounds are the most likely option. But on highly competitive early-stage rounds where founders hold the leverage, Korchevsky says he most frequently sees deals structured as SAFEs.

“Those founders can opt for terms they’re comfortable with,” Korchevsky says. “And I think the most comfortable terms for this stage is to structure rounds through SAFEs, because they don’t have any set timelines to conversion, and liabilities are limited.”

‘At some point, you’re betting on the jockey’

What sort of startups are raising the smallest pre-seed rounds, and what sort of startups are raising the largest?

The specific capital needs of the company’s sector are one factor. Reliance on AI is another. The startup’s plan for growth is a third: Do they aim to build lean, or are there key hires or investments the founders hope to make in the near term?

Like everything in venture capital, the ultimate size of a pre-seed round relies on the dynamics of supply and demand. Just because a startup thinks it needs to raise a $5 million pre-seed round doesn’t guarantee that it will be able to.

Before they will cut a check, pre-seed investors are looking for any sort of early signal that could indicate traction, such as revenue, customer acquisition, or initial product-market fit. If a startup is still too immature to have reached any of those landmarks, investors may rely on other, less tangible clues.

“A lot of what you’re betting on is who the founder is, where they’ve been in the past, who else is investing with them, what the team looks like,” Laine says. “The idea matters a whole lot. But a lot of it is, can this person that you’re giving money to execute this idea? At some point, you’re betting on the jockey as much as the horse.”

Increasingly, the window of time in which pre-seed investors must make their investment decisions is shrinking. Just as AI is contributing to the barbell shape of the overall pre-seed funding market, it’s also accelerating timelines for founders and VCs alike.

“Two or three years ago, you had founders who were open from the very beginning that they were still pre-product. They were open that it would take six months, and then it was up to you whether you buy the story or not,” Korchevsky says. “Now, those first proof points can happen much quicker.”

Subscribe to the Data Minute newsletter

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.