Last year, startups in the healthcare sector were responsible for more than a quarter of all venture capital funding raised on Carta. The only sector that raised more VC funding in 2024 was SaaS.

Healthcare is one of the most popular places for venture investment, and has been for many years. However, for the VCs writing the checks, investing in healthcare—which includes pharmaceuticals/biotech, healthcare technology, and medical devices—can look very different from other common sectors, like SaaS, fintech, or consumer.

Shalabh Gupta, the founder and CEO of Unicycive Therapeutics, points to three main ways that healthcare stands out for fundraisers.

First, building a startup in healthcare is often more capital-intensive, due to necessary spending on the R&D needed to create novel treatments or products. Second, healthcare startups often face a longer timeline to revenue generation and profitability. Combined with the capital needs of healthcare startups, this can mean investors must be willing to lock up a larger sum of capital for longer. And third, healthcare is hard: Investing smartly in many niches of healthcare can require specific industry knowledge that has little overlap with other common VC areas.

“In healthcare, the pathway to profitability is usually much longer,” Gupta says. “Generating revenue and being profitable is not something you need to immediately focus on, because the biggest thing is to get the drug or the product approved and on the market.”

For these reasons, healthcare startups raising new VC funding typically experience more dilution than their peers in other sectors do at the same stages of startup life. Healthcare startups often need more cash, a longer time commitment, and more hard-won expertise. In return, healthcare investors often receive a bigger piece of the ownership pie.

>> See Carta's Data Desk for more data and insights on private markets

The data on healthcare dilution

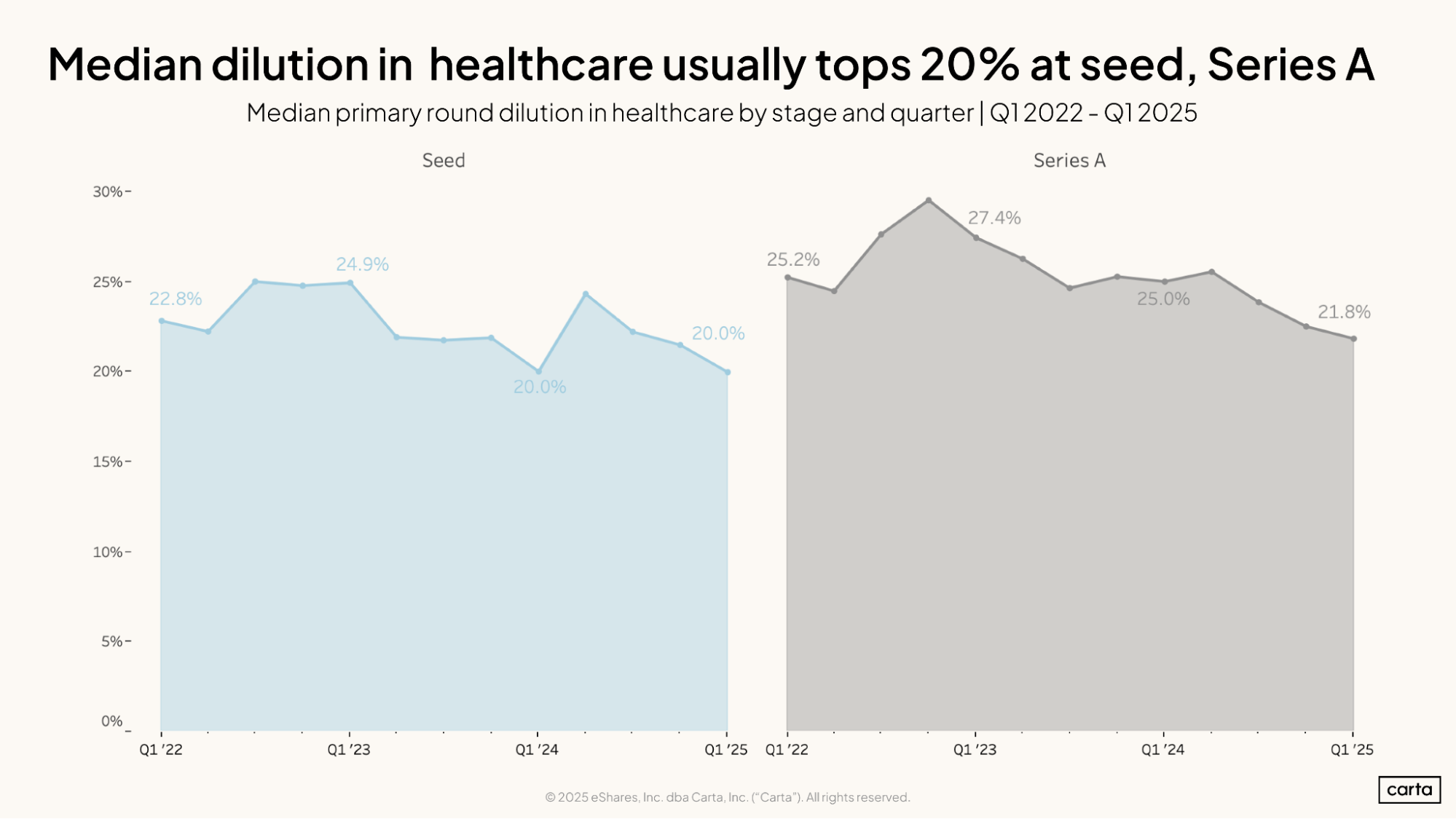

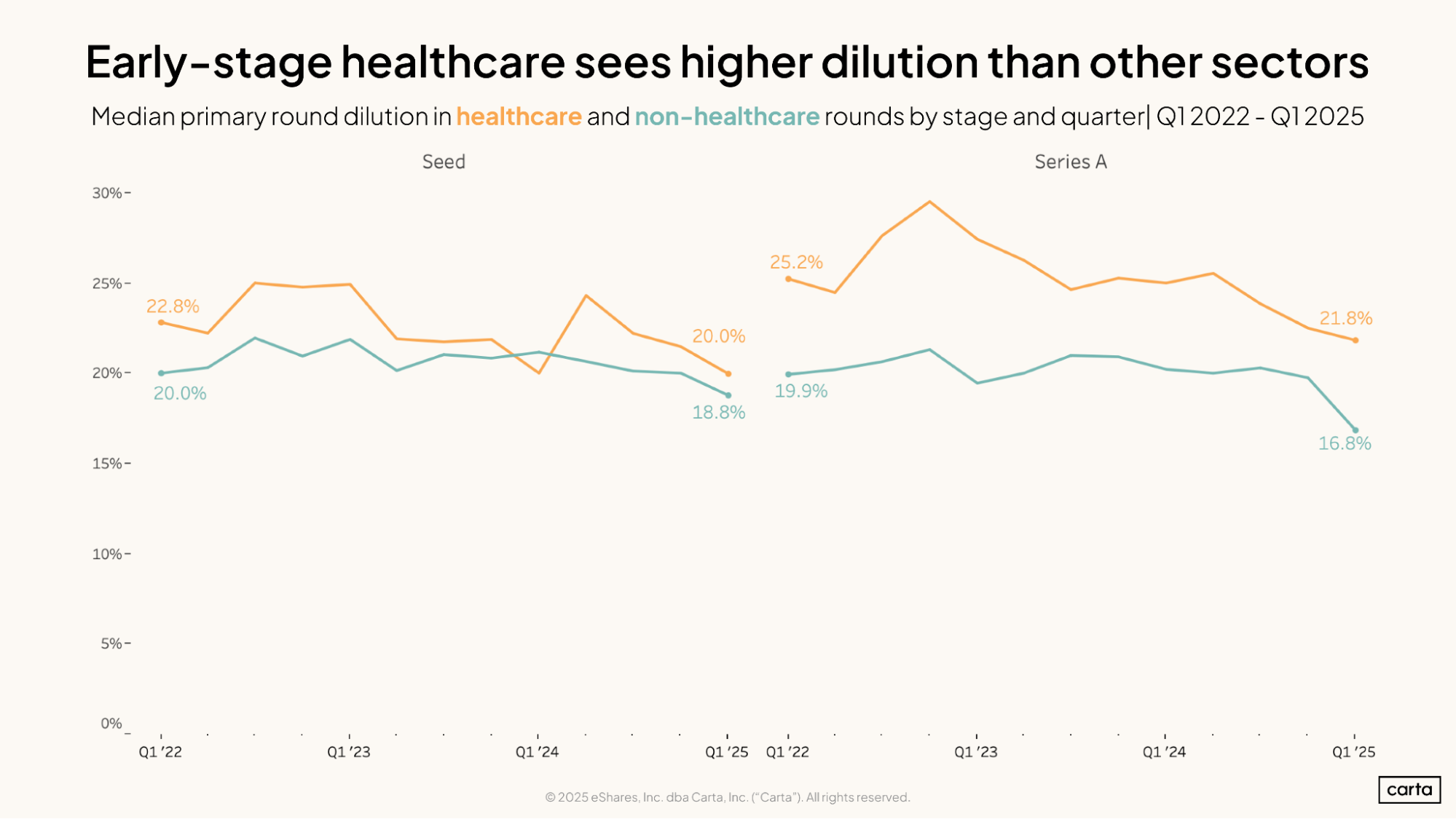

At the earliest stages, it’s typical for healthcare startups to experience dilution of around 20% in new primary funding rounds. In Q1 2025, the median dilution on seed rounds on Carta across the broader healthcare sector was an even 20%. At Series A, median dilution was 21.8%.

At both stages, that figure has declined in recent years and in recent quarters. Median dilution has been trending down significantly at Series A in particular. Still, even with these declines, dilution still tends to be higher in healthcare than in other sectors. At seed, median dilution in Q1 was 1.2 percentage points higher in healthcare investments compared to non-healthcare rounds. At Series A, median dilution was 5 percentage points higher in healthcare.

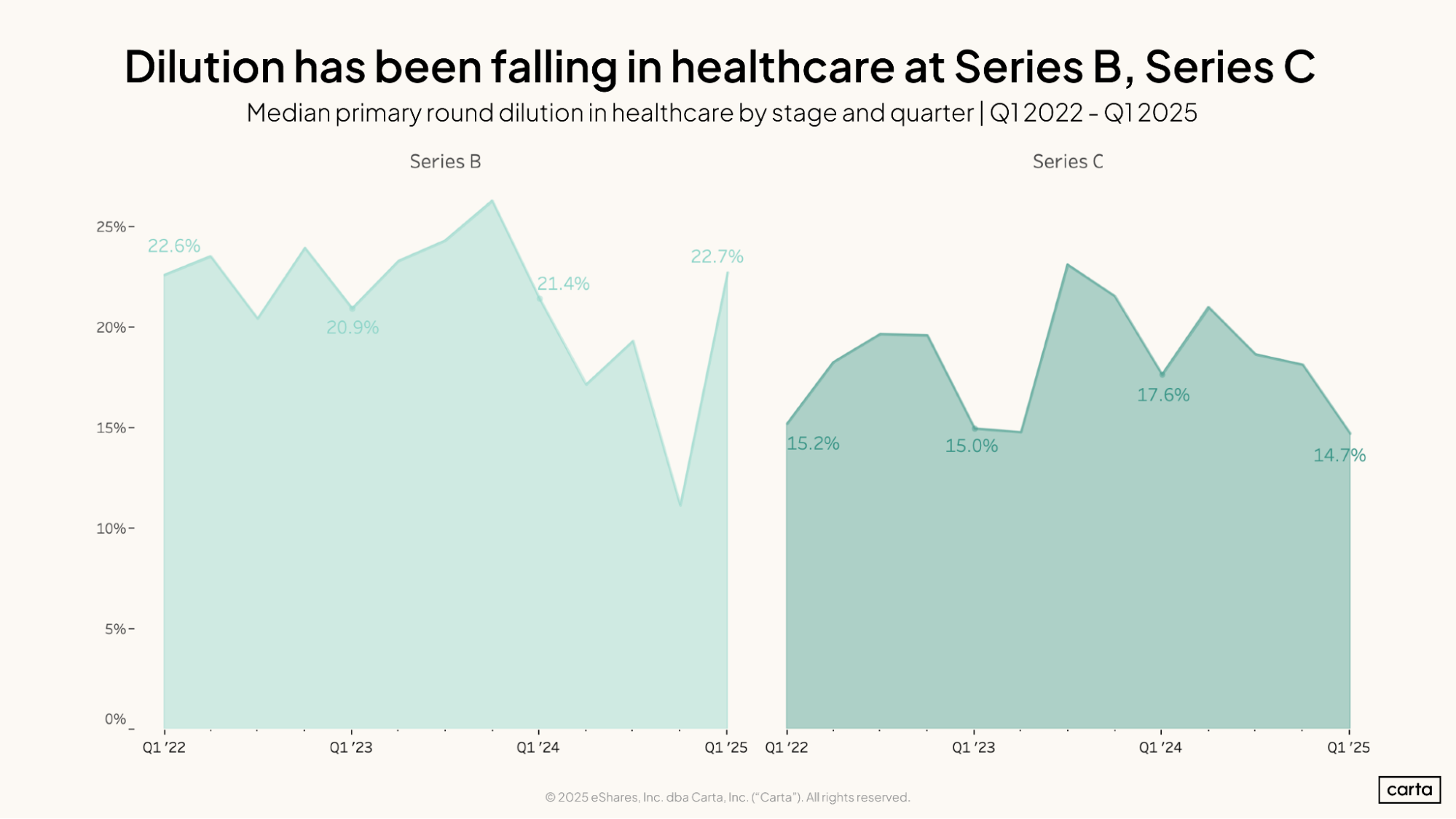

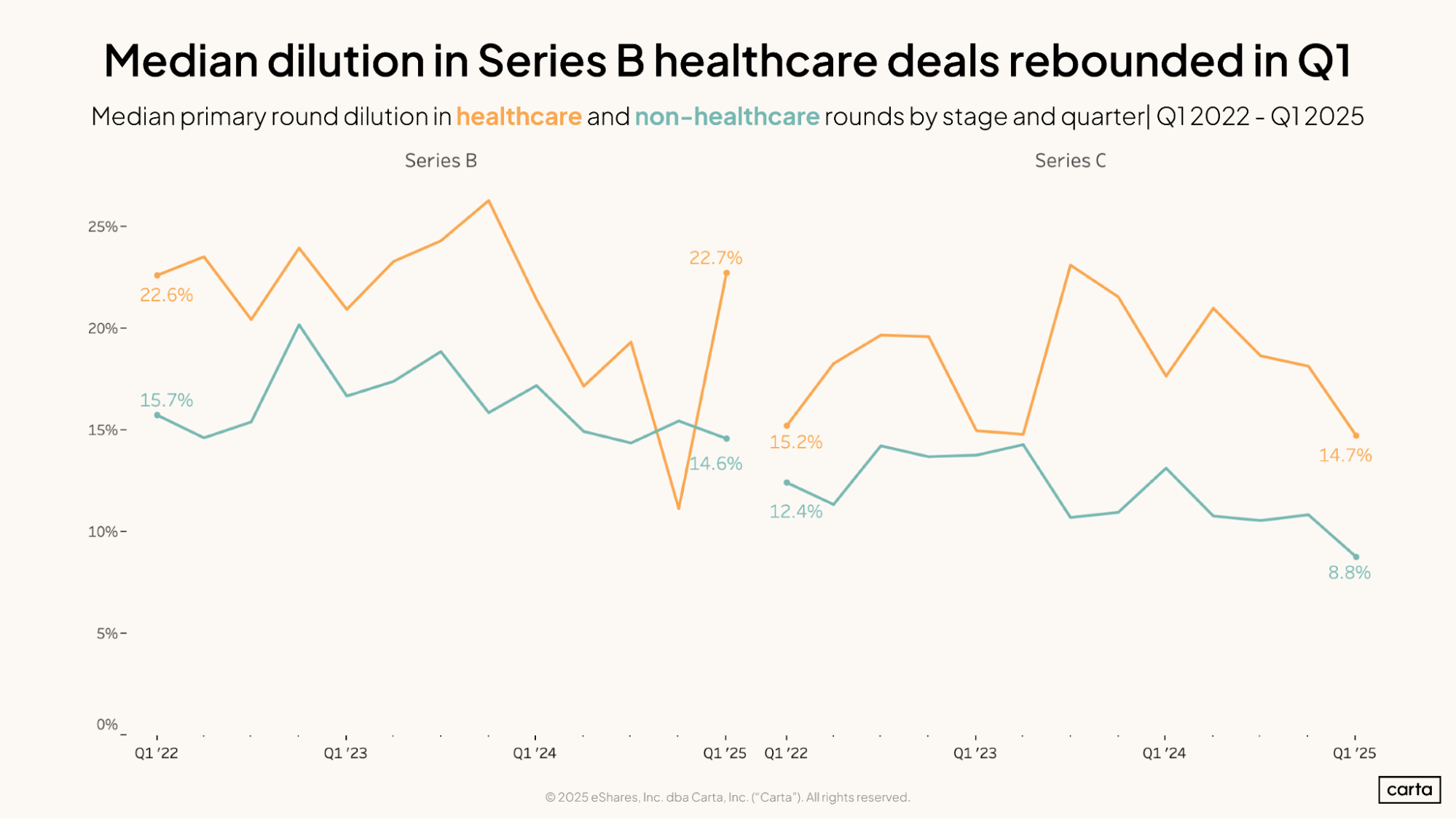

At later stages of investment, the data over the past three years is directionally similar, but not quite as consistent. Median dilution at Series B declined sharply during 2024, only to spike in Q1 2025, rising to 22.7%. Median dilution also fell in recent quarters at Series C, dropping to 14.7% in Q1.

Again, healthcare startups tend to see more dilution at these later stages than startups in other sectors. Since the start of 2022, median dilution has typically been at least a couple percentage points higher on healthcare rounds at both Series B and Series C, with one exception (Series B in Q4 2024).

For both healthcare startups and non-healthcare startups, and across every stage from seed through Series C, median dilution figures have generally been declining over the past three years. Part of this shift can be attributed to an increased emphasis on efficiency in the startup ecosystem in the wake of the 2021 venture boom. Many companies are trying to do more with less. When they succeed, they can require less VC funding to reach the same sort of valuation, which inherently results in lower dilution.

This thesis doesn’t apply to healthcare in quite the same way it does to other sectors. In terms of capital needs and the ability to streamline and automate processes, working with lab equipment can be different from writing code.

But the startup world’s focus on efficiency is certainly still a factor in healthcare, according to Gupta. Startups are seeking ways to maximize each dollar raised. A drug developer, for instance, might outsource certain elements of production that aren’t a part of the startup’s secret sauce.

“You want to be capital-efficient before you build up a huge team,” Gupta says. “You might want to outsource as much as you can outsource. If it’s not core to what you do, that may be the best way to create value for investors.”

How healthcare sub-sectors stack up

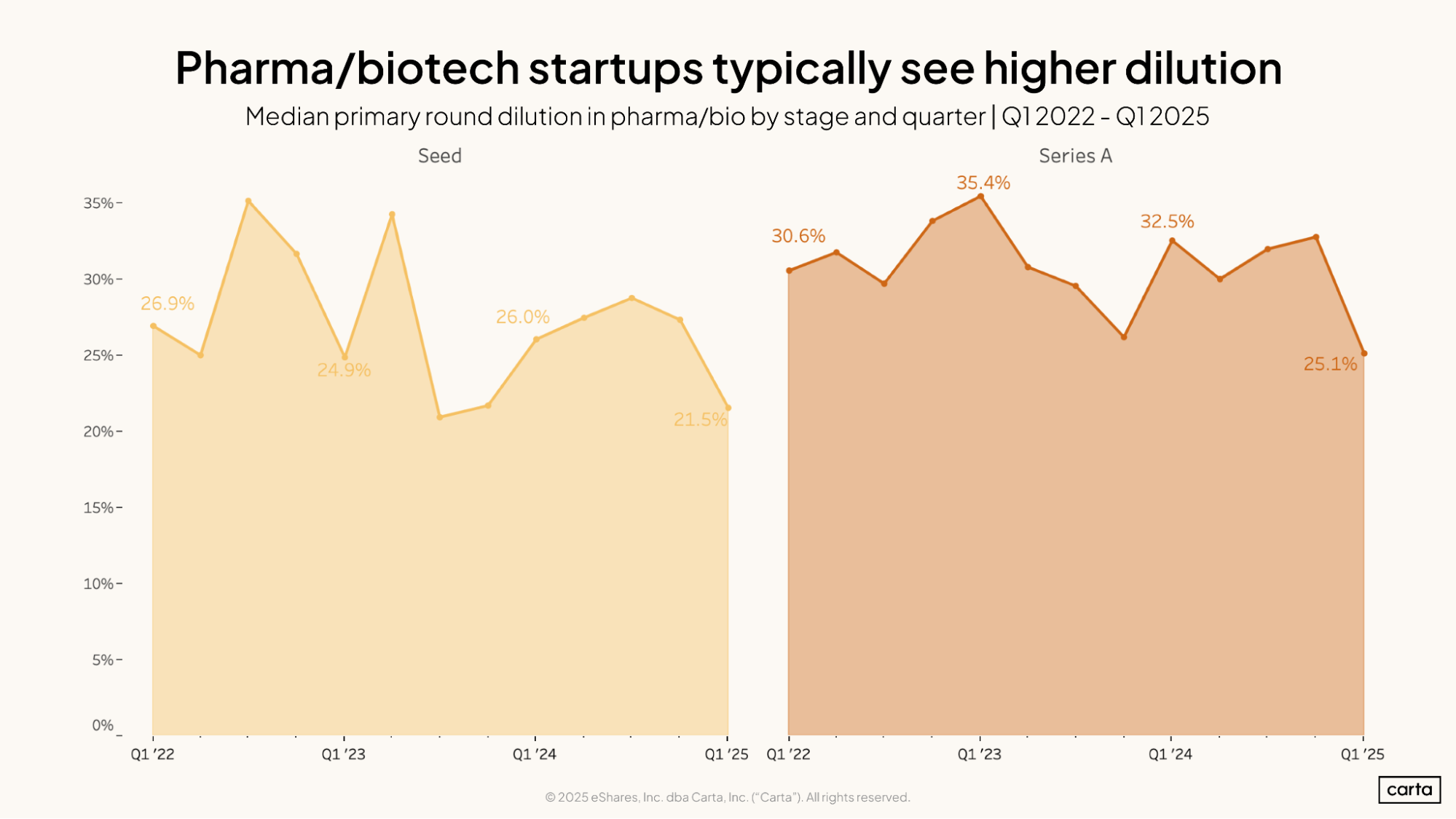

Dilution tends to be higher within the pharmaceuticals/biotech sub-sector than across healthcare as a whole. At Series A, for instance, median dilution was often above 30% over the past three years, before dropping to 25.1% in Q1 2025. As we saw above, median dilution at Series A was 21.8% across the broader healthcare sector in Q1 and 16.8% on non-healthcare rounds.

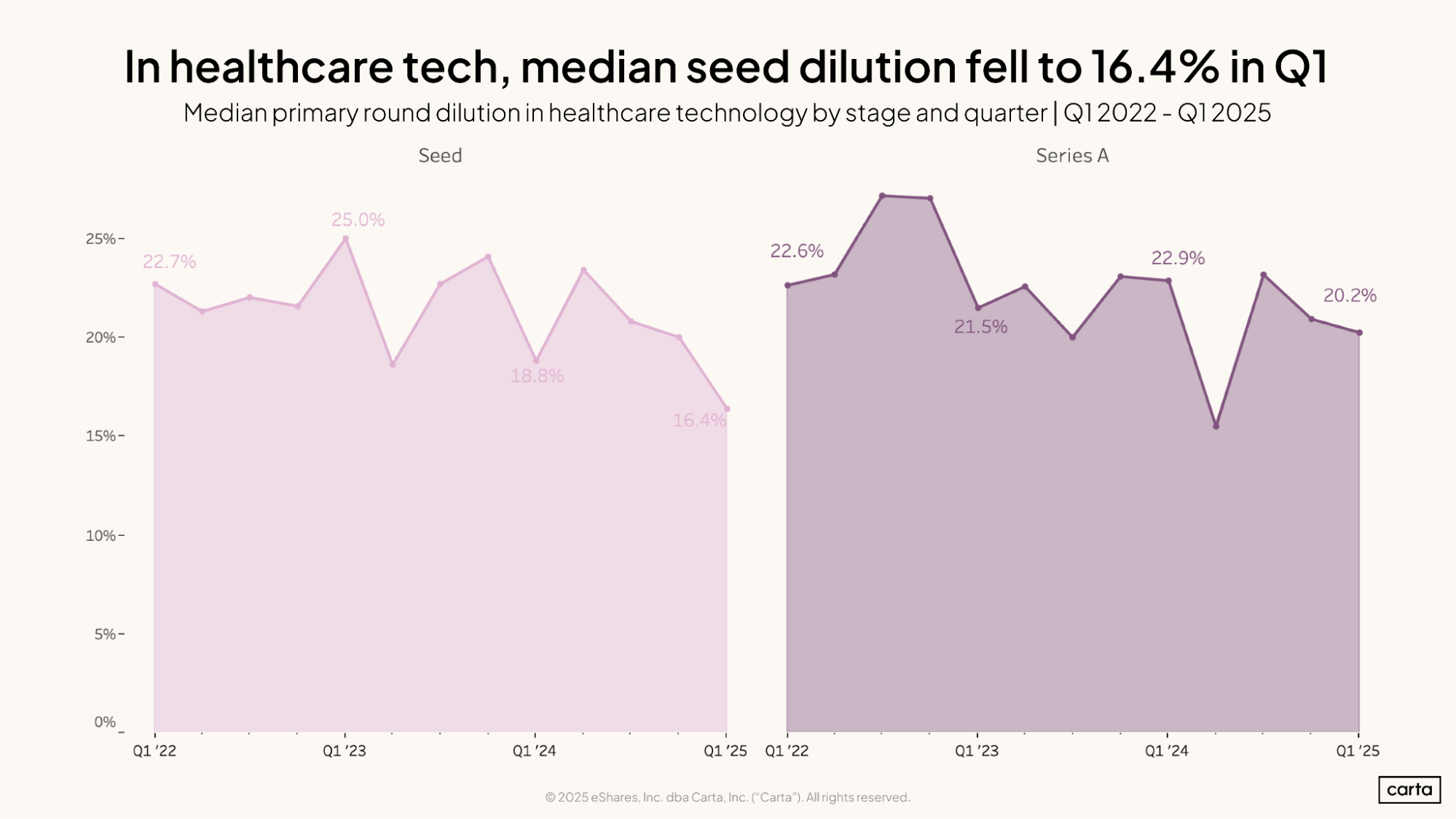

Within healthcare tech, meanwhile, dilution tends to be notably lower. At the seed stage, median dilution on healthcare tech rounds was 16.4% in Q1 2025. Compare that to 21.5% on seed rounds in pharma/biotech, 20% across all of healthcare, and 18.8% in non-healthcare deals.

For Gupta, this gap in dilution points to a key difference between different parts of healthcare. Compared to pharma/biotech or medical devices, building a startup in healthcare tech can often look more like it does in other sectors. Here, a company can succeed without intensive R&D or the elongated timelines of clinical trials, and marketing can be easier to get off the ground.

“Digital health technologies are where you can potentially create a product that has a shorter duration and is less onerous in terms of the cost, and potentially see more user adoption,” Gupta says.

No matter the sector and no matter the stage of investment, for a founder, determining how much dilution is right for their company is a delicate balancing act. Decisions on dilution could have major implications for anyone who is working toward a startup’s eventual success.

“There is no one right answer [on how to approach dilution],” Gupta says. “But once you have investors on your cap table, it’s not just you as a founder or you as a management team anymore. It’s you and your investors—you have to think about them, too.”

Sign up for the Data Minute newsletter

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.