Early-stage valuations are on a record-setting run. And in the fourth quarter of 2025, the red-hot market got even hotter.

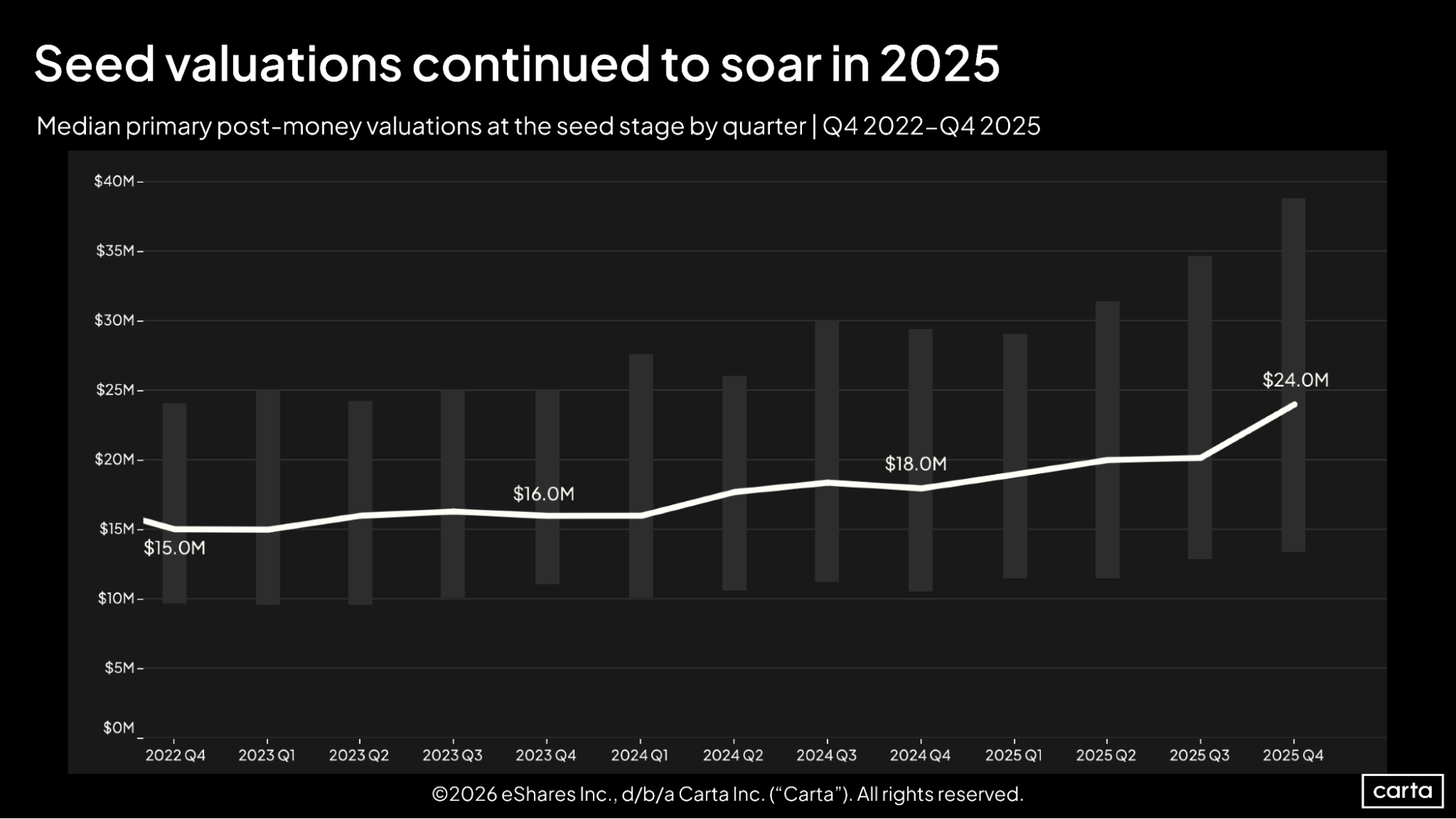

At the seed stage, the median post-money valuation on primary rounds rose to a new all-time high of $24 million in Q4. A year earlier, that figure was $18 million—which, at the time, was a record high—and two years ago, it was $16 million.

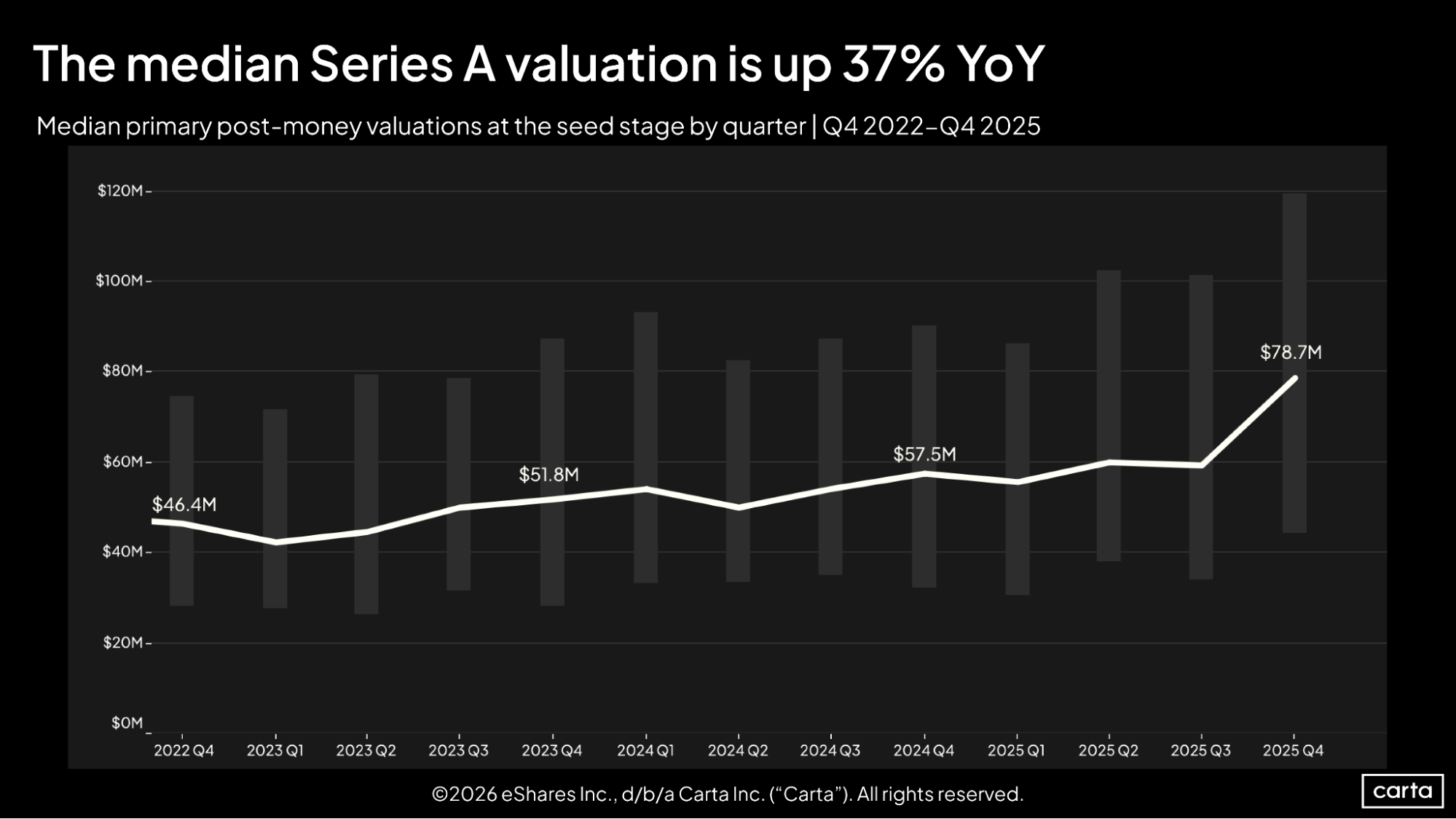

It’s a similar story at Series A, where the median post-money valuation rocketed to $78.7 million in Q4, up 37% year-over-year from a previous mark of $57.5 million. At both stages, it’s not just the median: The 25th percentile and 75th percentile valuations, shown in these charts by the fainter gray bars, are also rising to new highs, reflecting a broader uplift. At the low end of the market, the high end, and in the middle, early-stage valuations are climbing considerably higher than ever before.

These figures span all sectors of the startup economy. Of course, these days, most sectors involve at least some degree of AI. For Andy Triedman of Theory Ventures, this leads to two primary reasons why early-stage valuations have been surging.

One is that, with new AI tools at their disposal, many young companies have been able to generate revenue more efficiently than past generations of early-stage startups, increasing their appeal to VCs. The second is that with these efficiency gains—plus the relative nascency of the AI space—founders and investors alike are viewing some of these companies with near-boundless optimism, believing there’s a real chance that the current early-stage generation will eventually produce companies with market caps measured in the trillions of dollars.

“At the core, I think those two things are driving a lot of the investor posture toward being willing to be more aggressive on pricing,” Triedman says.

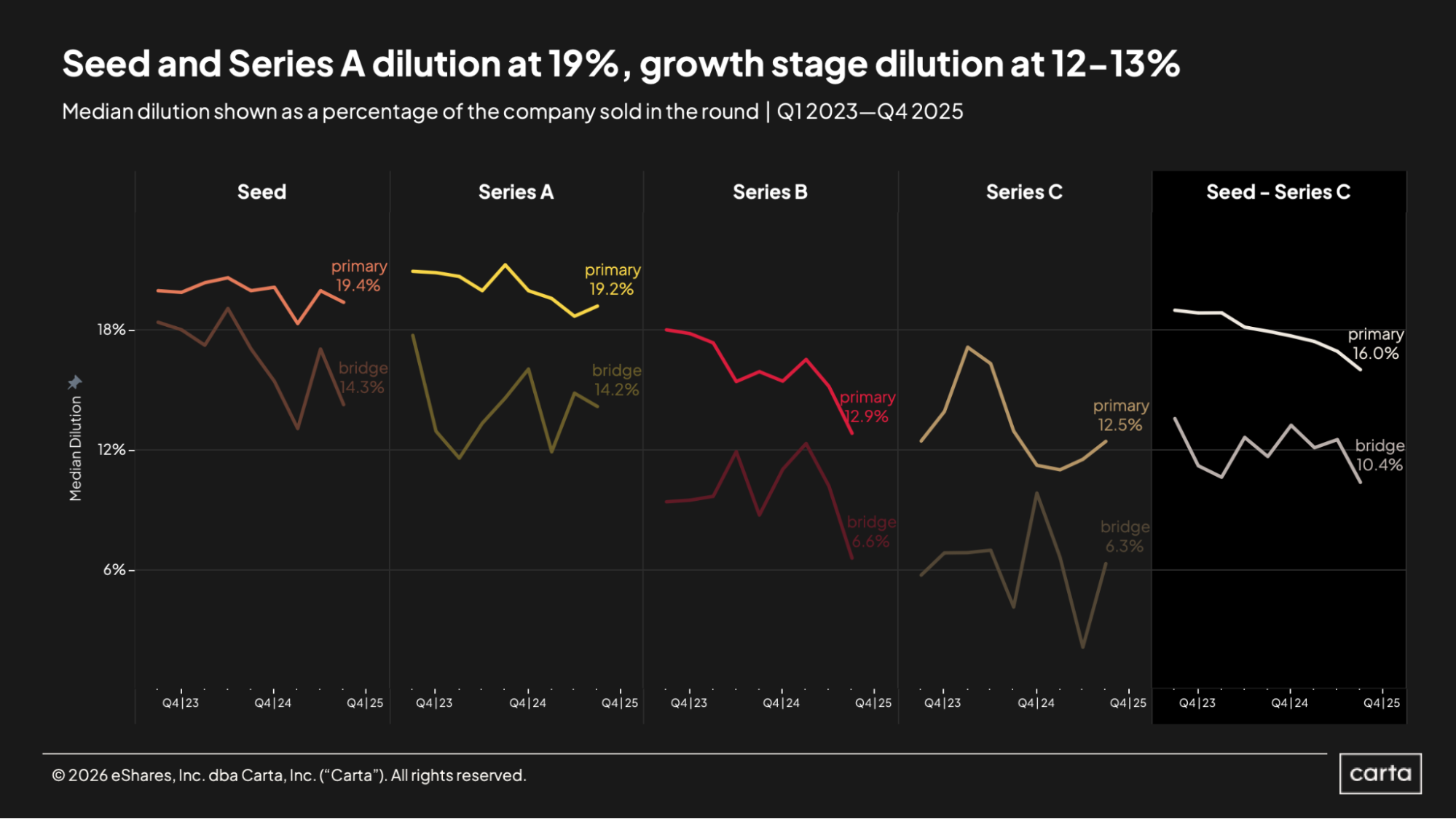

Steady dilution, rising valuations

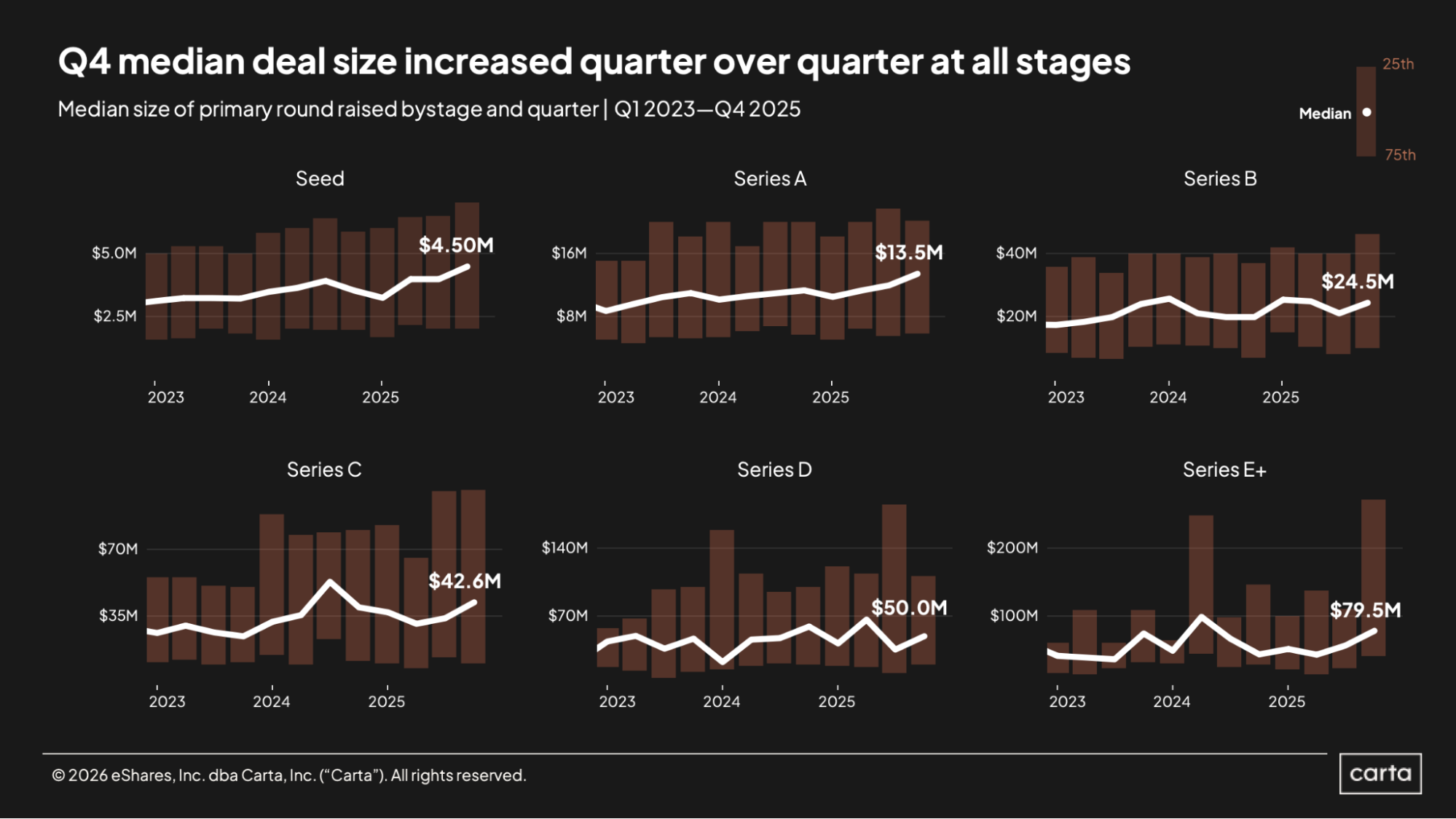

The economics of venture fundraising can sometimes look like an algebra equation, with three of the most critical variables—round size, valuation, and dilution—all dependent upon one another. For instance, if the size of a round increases and dilution stays the same, then by definition, the valuation will increase, too.

This is what’s happening in today’s venture market, Triedman says. Dilution at the seed stage and Series A has declined slightly over the past two years, but the medians at both stages are still between 19% and 20%, right around the industry’s historical standards. Early-stage round sizes, meanwhile, are trending up.

In some cases, this may be to pay for access to expensive AI chips and servers. In others, larger round sizes may be used to pay top dollar for increasingly in-demand AI talent. Some startups may also be choosing to raise more capital for the simple fact that VCs want to write larger checks and increase their exposure to exciting opportunities. Regardless of the motivation, the impact on valuations is inescapable.

“We’re seeing prices go up because round sizes are going up,” Triedman says. “The fixed dilution is really what’s driving up the prices.”

For Sandeep Menon, CEO of Auxia, an agentic marketing platform that helps marketing and product teams leverage first-party data to orchestrate personalized customer journeys, investor interest played a critical role in determining round size, which in turn was a key determinant of valuation. When Auxia closed $23.5 million in combined seed and Series A funding last year, it was more cash than the company initially anticipated raising.

“Our plan was to raise less than that,” Menon says. “There was some strong demand. And where we landed was, hey, at this point in time, we will take on a little bit of extra capital.”

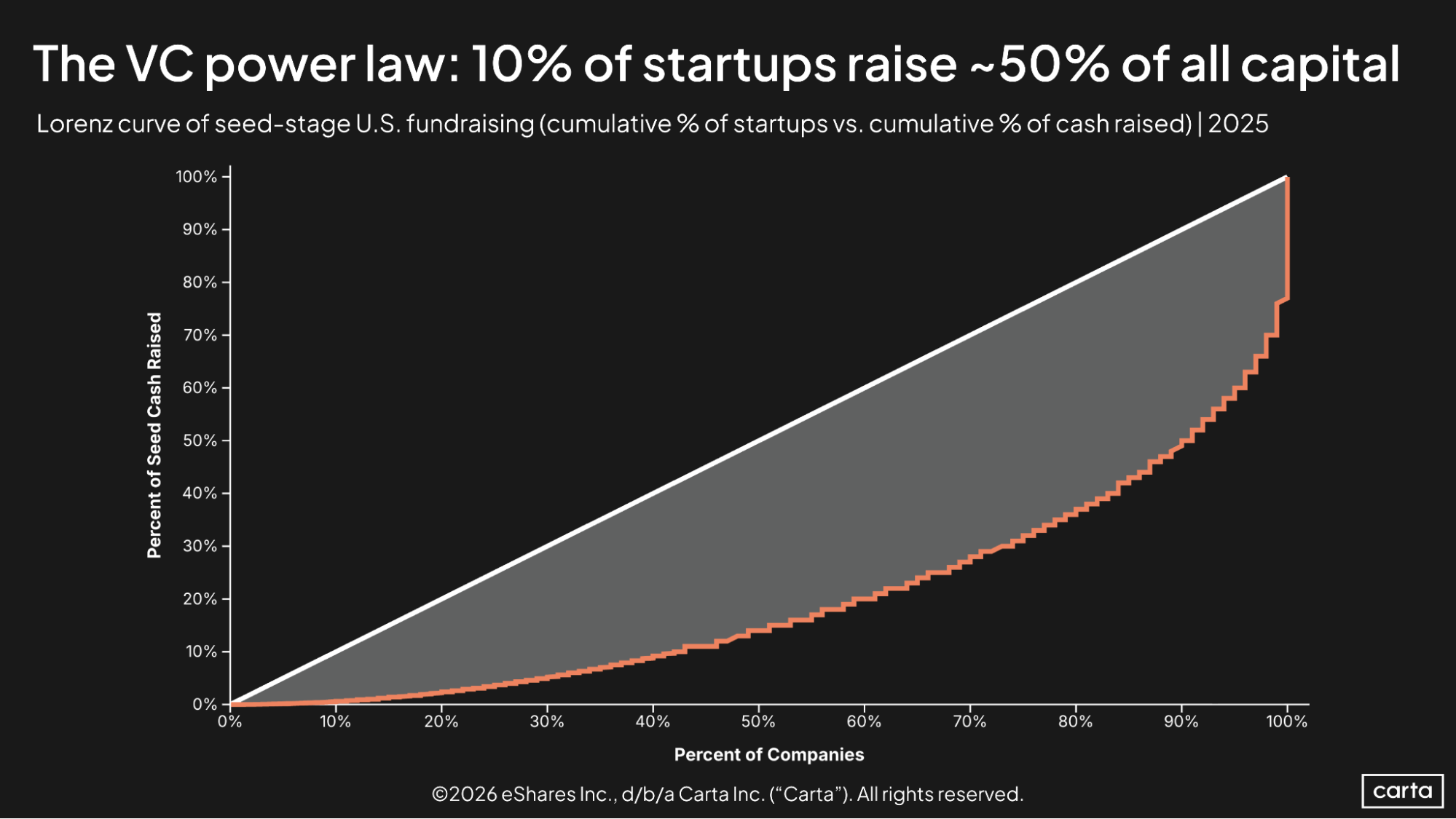

Concentrated capital

This desire among investors to devote more capital to their top targets is at the heart of another trend that’s contributing to higher early-stage valuations: The increasingly concentrated nature of VC spending.

The spray-and-pray approach has fallen out of style. After the market turmoil of the early 2020s, investors are choosing to make larger, more confident bets based on early conviction. When multiple VCs feel the same level of conviction about certain early-stage targets, this developing preference also leads to increased competition among investors.

“Instead of the VC giving three $3 million seed checks, they’re giving one $9 million seed check,” says Lindsey Mignano, co-founder at SSM Legal, which advises early-stage investors and their portfolio companies.

In 2025, the bottom 50% of U.S. startups on Carta that closed a round combined to bring in just 14% of all cash raised. The top 10% of startups, meanwhile, combined to raise about half of all capital.

On some level, this has always been the dynamic in VC, with a relatively small number of startups raising an outsized percentage of capital. But investor attitudes today can differ sharply from the investing climate of 2021, when VCs were writing a record-breaking number of new checks. After seeing some of the downsides of such a broad-based approach, investors now are moving in the other direction.

Of course, for some companies and investors, this different approach might create new problems of its own.

“We believe highly in the value and revenue these startups will generate,” Triedman says. “And at the same time, you see prices that in many cases are irrational or hard to justify.”

Haves and have-nots

This new dynamic that has emerged in the recovery from the 2022 market reset is similar to the broader economic response to COVID-era upheavals. Rather than a rising tide that lifts all boats, the funding environment has turned increasingly K-shaped.

“We have a real bifurcation of who’s getting attention and funding and who’s not,” Mignano says.

For those companies that are successfully raising new rounds, it makes for an appealing seller’s market. But what about those that are struggling to find their next funding?

“Some of them are making do and just not going to raise,” Mignano continues. “They might be exploring alternative options. For consumer-based companies, they might look into crowdfunding. They might tap their existing angel syndicates or family offices for a SAFE note bridge round, just to get them to the next milestone so that they can justify a raise.”

Mignano also points to another, less appealing option. Some founders are choosing to simply wrap up their finances and shut the company down, sometimes with limited pushback from their VCs, who might have been expecting such an outcome for a while.

Even as rounds get bigger, valuations get larger, and VCs get pickier, some things never change. No matter how much cash a company is raising or what valuation VCs are willing to pay, Sandeep Menon of Auxia says that founders should prioritize making sure that the economics of the round make sense for their own vision of their startup’s long-term future.

“The price you raise at is so important, because ultimately, you’re giving away your most precious equity at the early stages, right?” Menon says. “So you do need to value it correctly.”

Subscribe to the Data Minute newsletter

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.