As the 2020s unfold, venture capital funds are slowly but steadily shrinking.

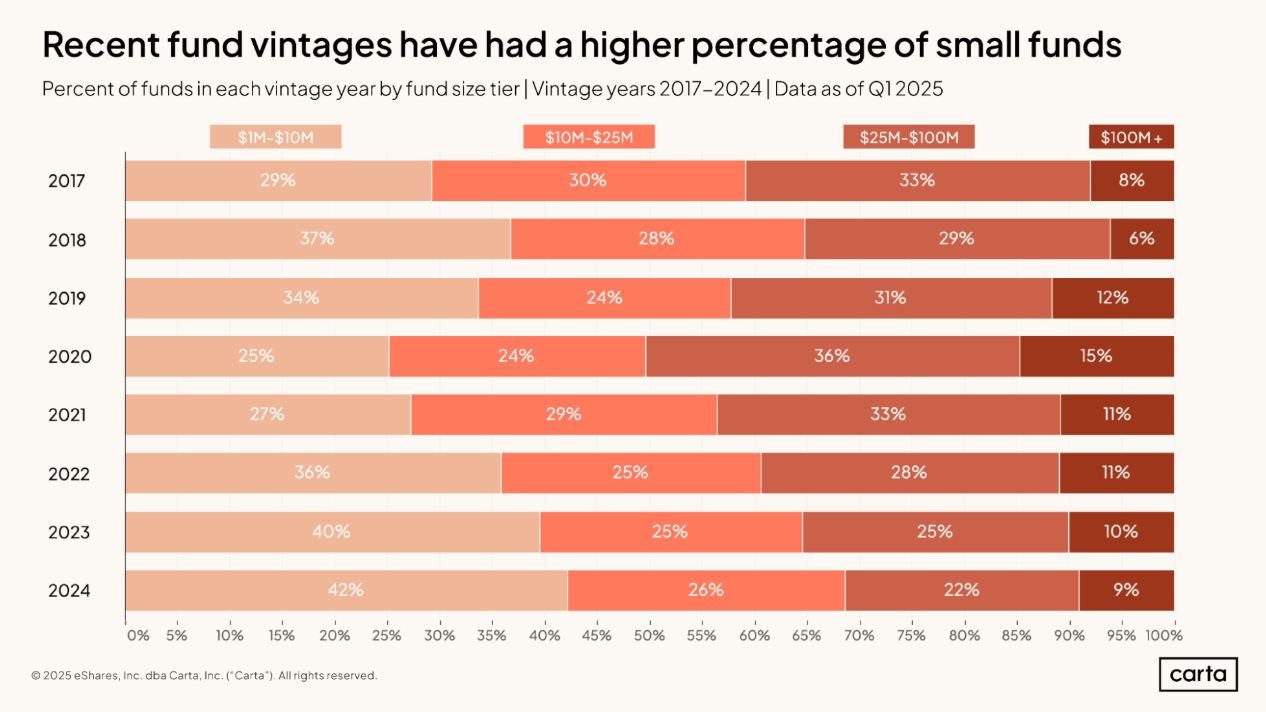

Back in the first year of the decade, 51% of all new venture funds tracked on Carta had $25 million or more in assets under administration, and 49% of funds were smaller than $25 million. By 2024, the balance had shifted considerably: Last year, just 31% of new VC funds were larger than $25 million, and 69% of all funds fell below that threshold.

Early-stage investors say that this change is symptomatic of larger transitions underway in the venture market. Over the past several years, the ranks of solo GPs and other emerging managers has expanded, in some cases driven by entrepreneurs and aspiring investors who minted their wealth during the IPO boom of 2020 and 2021. And many LPs are thinking about their VC portfolios in different ways. Some have pulled back from venture altogether. Others are shifting their allocations and making bets on different kinds of VCs than they have before.

“More founders are becoming angels. More angels are becoming GPs. More GPs are raising funds outside the traditional institutional pipeline,” says Anthony Georgiades, general partner at Innovating Capital, which invests across various deep tech industries. “What we’re seeing now is a fundamental reshaping of who gets to be a venture capitalist and who doesn’t.”

>> See Carta's Data Desk for more data and insights on private markets

The rise of the solo GP

As co-founder and CEO of BuildGroup, a VC firm founded in 2015 that focuses on AI-enabled workflow startups, Jim Curry keeps a close eye on the competition. Lately, he’s noticed a surge in the number of solo GPs choosing to hang up their own shingle.

“I’ve seen a lot more folks deciding to do their own thing,” Curry says. “Maybe that’s because their funds are not raising, or maybe they just decided now’s the time to strike out on their own.”

Compared to traditional multi-partner venture shops, these solo GPs are more likely to raise smaller funds. At a basic level, a smaller, less complex fund tends to be easier to manage for a solo practitioner. Solo GPs might also have less access to LPs who are used to writing large checks, and they might have less of their own personal wealth that they’re able to put into the fund as a GP commitment.

Today, the mechanics of a solo GP deciding to go it alone are easier than ever.

“The COVID catalyst in 2020 opened up the door for a lot of things,” Georgiades says. “You had this wave of digital-first entrepreneurship, everything in the cloud. And this created a much lower barrier to entry for founders, and then obviously for fund managers in return. There was this capital-as-a-product type mentality. And this made it super easy for solo GPs to launch these micro funds.”

The rise of solo GPs and other small funds was also aided by the flood of liquidity that swept over the startup world in 2020 and 2021, when annual IPO exit values soared to recent highs. Many investors and entrepreneurs who were already familiar with cutting-edge tech found themselves flush with cash. And some of them chose to pump some of those earnings back into the ecosystem.

“This created massive personal liquidity for operators and the like,” Georgiades says. “So there were a ton of these scout funds or solo GP funds that didn’t really have any institutions behind them. It was self-funded, high-net-worth individuals, post-exit founders, whatever it might be. And this micro-fund really became an asset class in its own right.”

The appeal of small funds

For LPs, investing in smaller fund sizes comes with some clear appeals. Smaller vehicles can be nimbler than larger funds. Small funds are often hyperspecialists that focus on a particular niche of the economy; this specialization and deep sector knowledge can help them identify opportunities earlier than larger generalist investors.

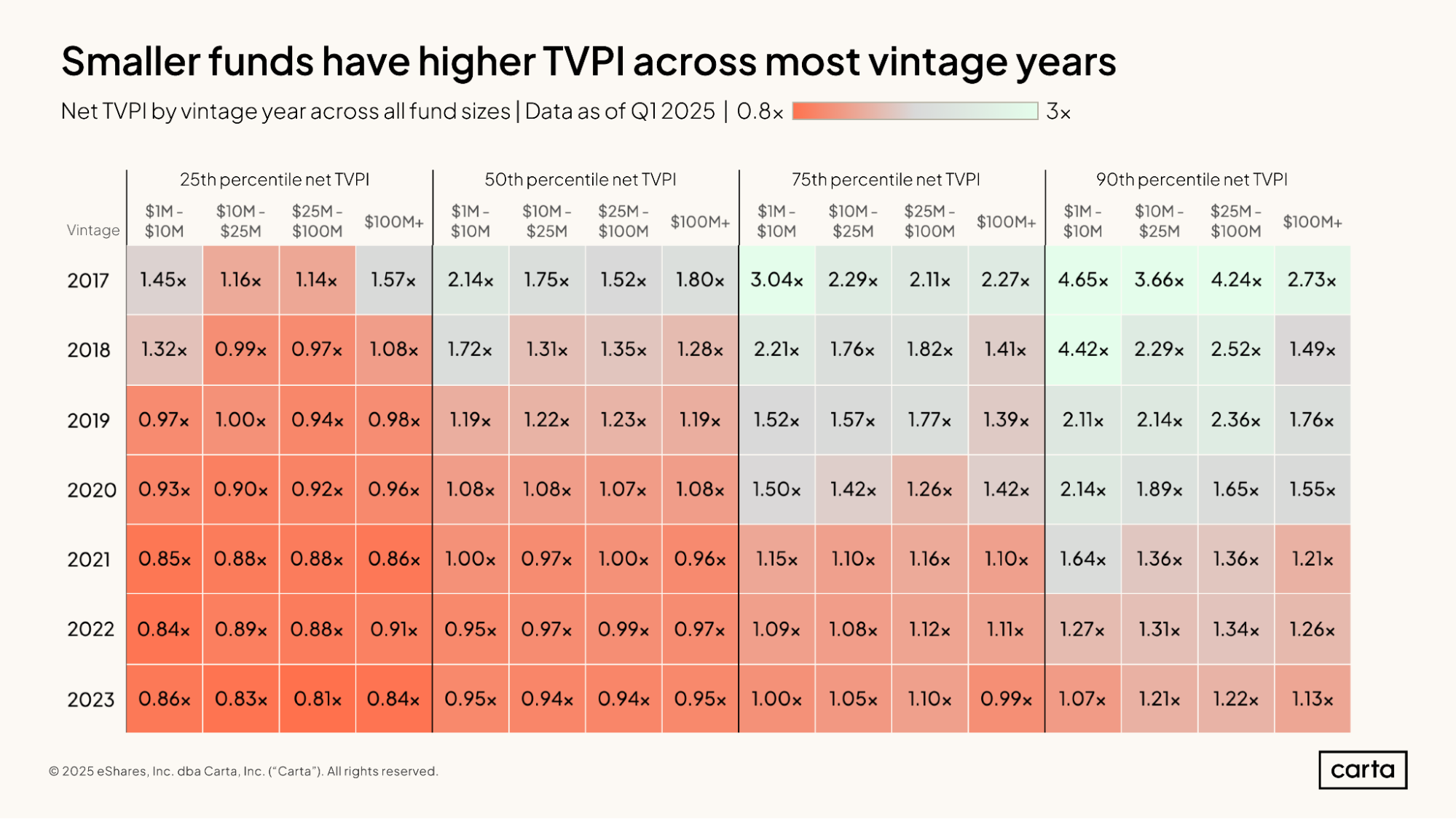

Most importantly, the economics of smaller funds can be quite attractive. As shown below, for recent fund vintages tracked on Carta, smaller VC funds are mostly producing stronger return multiples than larger funds. This holds with existing research that smaller VC funds tend to outperform their larger peers.

In some cases, these smaller funds are capable of creating strong returns without producing any uncommon successes. Consider a hypothetical $10 million VC fund that writes a $350,000 check to take a 7% stake in a seed-stage company at a $5 million valuation. If that company—or any of the other companies that the fund backs on similar terms—is able to eventually achieve a $50 million exit, the fund’s stake will be worth $14 million. That’s more than enough to return the fund.

Of course, a $50 million exit is not guaranteed. But for a VC, it can feel much more attainable than the much larger exits needed to sustain a larger fund.

“You have a lot of GPs who are saying, let’s start a smaller fund,” Georgiades says. “We know we can deploy capital here, and we can back into asymmetric returns—the $5 million entry points with $50 million exits.”

A new generation

As these smaller funds have grown more common in VC, mid-sized funds have fallen off. Georgiades says that, in his experience, LPs aren’t pulling capital away from the mega-cap VC funds. Instead, they’re pursuing a more barbell-shaped approach.

“Those $25 million to $100 million funds were the hardest hit,” Georgiades says. “Too big for the friends-and-family, high-net-worth money, but too small for institutional mandates. Those smaller micro-funds have persisted because they can raise these small checks super quick. They don’t rely on institutional capital, and you have all these services that can do all the overhead for you. You don’t need to set up an admin or back office team or any of that stuff.”

For mid-sized GPs who are feeling the fundraising squeeze, this might be an unfortunate turn of events. But Curry believes that the rise of new solo GPs and other emerging managers will ultimately prove beneficial for the industry as a whole. Competition, he feels, is a good thing.

“It’s no different from the startup market, right? You want to see young startups come in and push the established players to do a better job,” Curry says. “I think that’s what’s happening here. I’m excited about the people trying to strike out and raise a fund and prove that they can do a great job not only for the investors, but hopefully for the companies they work with.”

Sign up for the Data Minute newsletter

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.