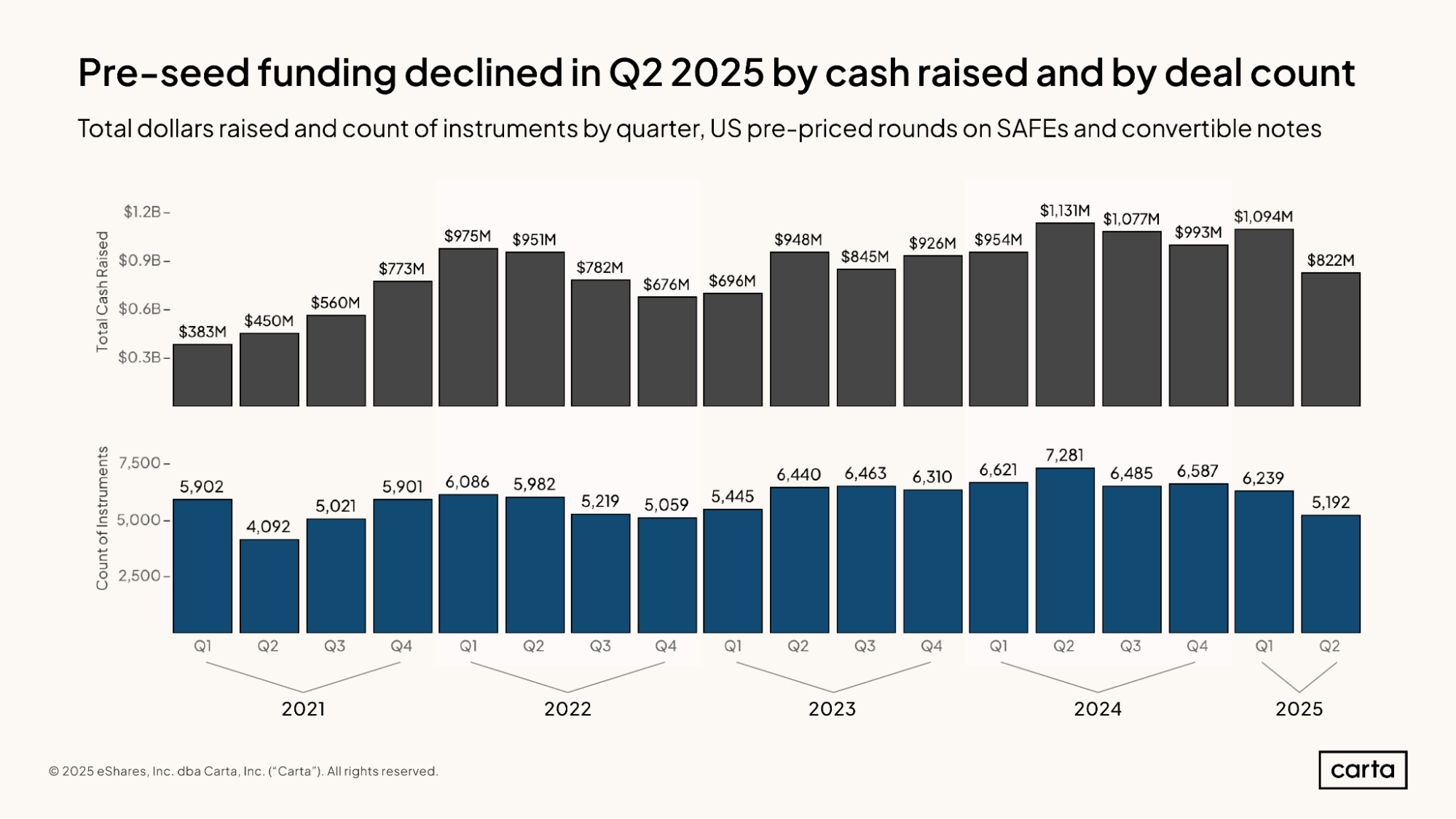

The overall landscape for pre-seed fundraising has been relatively stable since 2023, with quarterly investment remaining in the $800 million to $1.1 billion range. The number of SAFEs and convertible notes used in pre-seed deals each quarter has also not shifted widely, ranging from 5,000 to just over 7,000.

At the same time, some of the underlying dynamics of pre-seed fundraising—from valuation caps to deal sizes and sector trends—continue to evolve.

Where does Q2 of 2025 fit into the picture? Fundraising declined: Carta data shows that pre-seed funding for startups in the United States totaled $822 million in Q2, down from $1.1 billion in the previous quarter. Q2 pre-seed funding encompassed more than 5,000 SAFEs and convertible notes, a decrease for the second quarter in a row. This number is likely to be adjusted upward in the coming weeks as additional data becomes available.

Two other trends are worth calling out, even if top-level investment numbers haven’t changed drastically. First, this quarter saw a rise in the median valuation cap for smaller pre-seed rounds. For SAFE rounds under $250,000, the median valuation cap is now $7.5 million, up from $6.5 million last quarter. This may indicate that investors now foresee higher upside for very early-stage startups, likely influenced by productivity gains from AI.

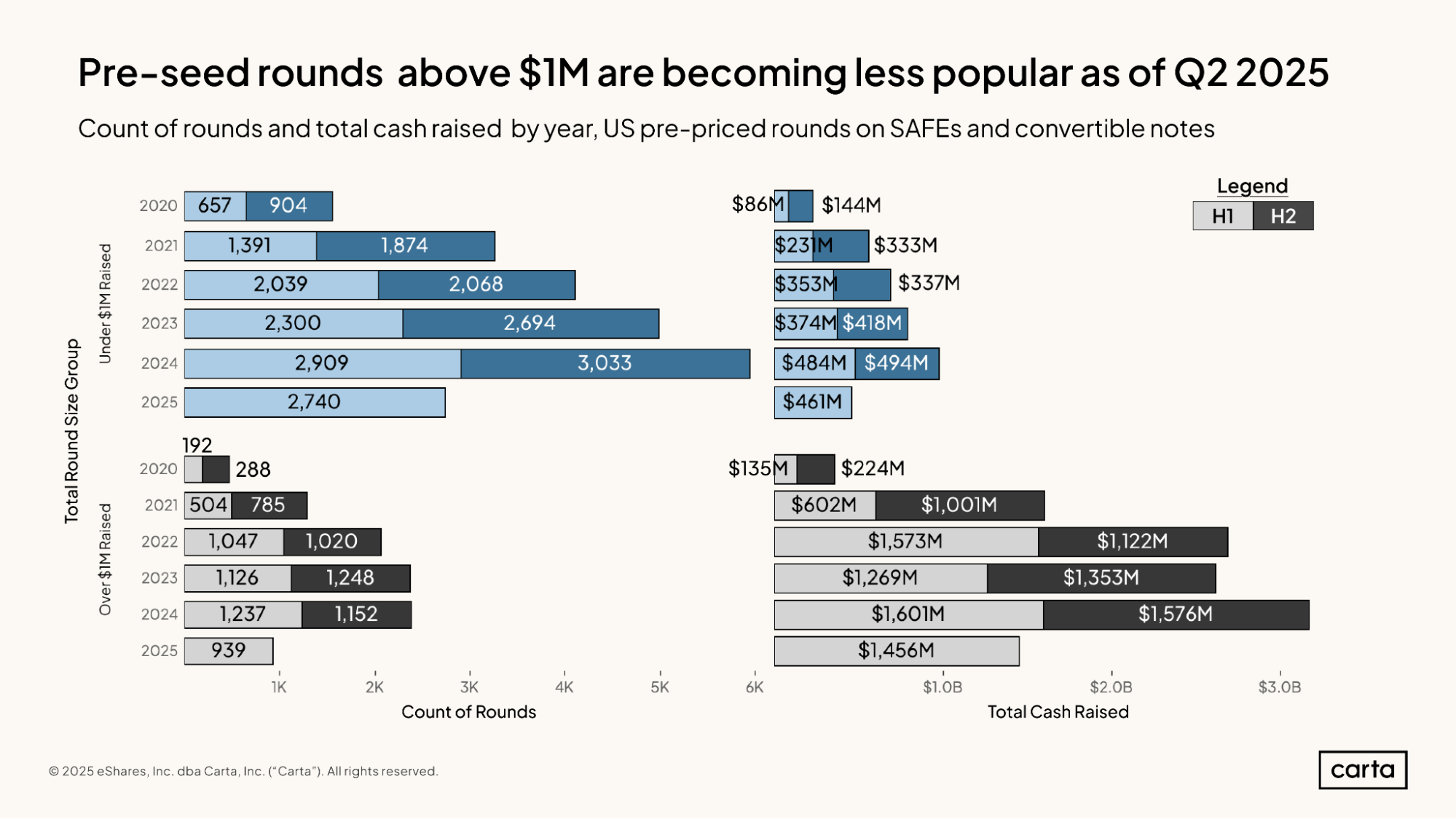

Also, SAFEs and convertible notes are being used in larger deals. Looking at all $3 million-$4 million rounds from the first half of 2025, a majority were raised on SAFEs or convertible notes, not priced equity. Previously, most companies switched to priced equity at deal sizes of around $3 million, but that threshold seems to have risen to $4 million. This is likely because SAFEs are easy to execute, though priced equity rounds are useful for companies further along their journey as they provide more clarity around ownership, valuation, and governance.

Continue reading for detailed data on industry, geography, round sizes, deal terms, and more.

Q2 2025 highlights

Decline in pre-seed activity: Pre-seed investment fell 25% in terms of cash raised this quarter, down from $1.1 billion in Q1 to $822 million in Q2. Similarly, the total number of pre-seed convertible instruments issued by startups to investors declined 17%, from 6,239 to 5,192 over the same period.

Convertibles are being used for larger rounds: The majority of early-stage rounds under $4 million were conducted on SAFEs or convertible notes, rather than priced equity, in the first half of 2025. In 2024, that was only true of rounds under $3 million.

Rise in valuation caps for small rounds: Valuation caps increased for smaller post-money SAFE rounds, reaching a median of $7.5 million for rounds under $250,000 and $10 million for rounds between $250,000-$500,000. Similarly, the median val cap for pre-money convertible note rounds under $250,000 rose to $7 million.

Industry dynamics: Startups in crypto/Web3 and biotech/pharma continue to have the highest median valuation caps in SAFE rounds. While crypto/Web3 companies comprise a relatively small portion of overall pre-seed funding, biotech/pharma represents the fourth-largest industry.

Nashville emerging as a pre-seed hub: After attracting $32 million over the past twelve months, Nashville broke into the top 20 U.S. metros for pre-seed fundraising.

Key trends

Full report available: Start reading now for free

Our complete State of Pre-Seed: Q2 2025 report includes 30 additional charts and analysis on SAFEs, convertible notes, dilution, discount percentages, and specific industries.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.