- Fund of funds: Navigating the operational complexities

- What is a fund of funds?

- How a fund of funds is structured

- Types of fund of funds in private markets

- Funds of funds and the secondary market

- Why GPs and LPs use a fund-of-funds strategy

- Fund of funds vs. direct fund investments

- The operational complexities of a fund of funds

- The double fee layer: Management and performance fees

- Look-through reporting and data aggregation

- Portfolio valuation and SOI aggregation

- Capital call and distribution management

- How Carta streamlines FoF administration

- A single source of truth for FoF operations

- A transparent LP experience

- Portfolio construction and forecasting for FoFs

- Take control of your FoF operations

- Frequently asked questions about funds of funds

What is a fund of funds?

A fund of funds (FoF) is an investment vehicle that pools capital from multiple investors to invest in other funds rather than directly in individual assets or securities. It earns a return for its investors by receiving a slice of the profits generated by each of the funds in which it invests. A FoF can invest in many types of funds, including exchange-traded funds (ETF), mutual funds, index funds, hedge funds, or alternative asset funds like private equity (PE), venture capital (VC), private debt, and real estate.

This approach is also known as a multi-manager investment strategy. Instead of having a single manager pick individual companies, the FoF manager performs due diligence on and selects other expert fund managers to invest in. The FoF manager's primary job is to identify, vet, and gain access to high-performing fund managers who align with the FoF's overall investment thesis.

This type of pooled investment vehicle is designed to provide investors with broader exposure to the asset class through diversification, market knowledge, access to fund managers in whom they would not otherwise be able to invest, and the potential for higher returns while mitigating investment concentration risk. By pooling investment capital to invest in a selection of other funds, a FoF can spread risk across multiple asset classes, sectors, vintage years, and investment styles. This layered approach helps reduce the impact of any single investment’s poor performance.

FoF managers actively allocate assets, especially on the public equity side, to align the portfolio with market conditions and investment objectives. In private markets, adjustments are more constrained and liquidity is typically driven by fund maturities. FoFs may at times seek liquidity by selling fund interests in the secondary market. Regular redemptions are common for retail-oriented evergreen or ETF-style FoFs, but are generally not available to institutional investors in traditional closed-ended FoFs.

How a fund of funds is structured

The legal framework of a FoF typically follows common fund structures, such as the limited partnership model. This structure involves two key parties.

First is the general partner (GP), who is the fund manager responsible for making all investment decisions and managing the day-to-day operations of the FoF.

Second are the limited partners (LPs), who are the investors that provide the capital for the fund to invest.

There are two main ways a FoF can be structured, which determines the universe of funds it is allowed to invest in.

Fettered funds: These FoFs only invest in other funds that are managed by the same parent company or a related entity. This structure keeps all management and fees within a single organization, often handled by dedicated management companies.

Unfettered funds: These FoFs have the freedom to invest in funds from any outside manager across the industry. This is the more common approach in private markets, as it allows the GP to search for and select the best-performing managers, regardless of their affiliation.

Types of fund of funds in private markets

While FoFs exist across many asset classes, they are particularly common in the private markets, a vast ecosystem where leading data providers track over $4 trillion in active fund net asset value (NAV). This is because accessing top-tier private funds can be difficult to nearly impossible for many investors (including high net-worth individuals and family offices), and achieving proper diversification across private assets is a significant challenge. A FoF can help solve both of these problems.

Here are the most common types of FoFs you'll find in private markets.

Venture capital fund of funds: This type of FoF builds a diversified portfolio by investing in a variety of venture capital (VC) funds. It provides LPs exposure to hundreds of early-stage startups across different industries, geographies, and stages of development, all through a single investment.

PE fund of funds: This FoF invests in a portfolio of different funds managed by PE firms. It allows LPs to indirectly invest in a range of mature private companies and strategies, such as leveraged buyouts or growth equity, which would otherwise require multiple, separate investments.

Hedge fund of funds: This FoF invests in a portfolio of different hedge funds. The goal is to blend various complex trading strategies, such as long-short equity or global macro, to generate returns that are not directly correlated with the public stock or bond markets.

Target-date fund: A target-date fund is a popular type of mutual fund that builds its strategy around a particular end date, typically the time when investors in the fund expect to retire. Over time, the fund rebalances its asset allocation across different asset classes to reduce risk as the target date draws closer. A target-date fund that invests in other funds, instead of directly in stocks, bonds, or other assets, is a FoF.

Funds of funds and the secondary market

FoFs are often active in the secondary market, serving as a source of liquidity for other LPs who made direct investments in VC or PE funds. If an LP is looking for liquidity from an investment in a fund that won’t be fully realized for several years, it might sell its stake in that fund to the secondary market where FoFs can be buyers. As such, FoFs can play an important role in increasing liquidity in the private markets.

Why GPs and LPs use a fund-of-funds strategy

Both investors and fund managers are drawn to the FoF structure because of its core strategic benefits. For LPs, it offers a simplified and efficient path to a complex asset class, with some industry analysts even providing adjusted returns to assist allocators in risk modeling. For GPs, it provides a vehicle to offer a unique value proposition to their investors that a direct fund cannot.

Instant diversification: A FoF provides investors with immediate exposure to a broad investment portfolio of underlying companies, different fund managers, and various vintage years (the year a fund begins investing), simplifying the portfolio construction process for the LP.

Access to top-tier funds: Many of the most successful and sought-after VC and PE funds are oversubscribed or have very high investment minimums, making them inaccessible to many investors. For example, according to Carta's 2025 Fund Economics Report, the median anchor check for VC funds between $100 million and $250 million reached $35 million in 2024. Compounding this high barrier to entry, the number of LPs in VC funds between $100 million and $250 million declined from 83 in 2022 to 47 by 2024—a drop of 43%. For the 2025 vintage, the median VC fund had just 23 LPs, less than half the median from four years earlier. Much like investment syndicates, a FoF can act as a key for LPs, pooling their capital to meet high minimums and gain entry into exclusive, hard-to-access opportunities.

Fund of funds vs. direct fund investments

As an investor looking to enter the private markets, your choosing between a FoF and investing directly into a venture or PE fund involves a series of tradeoffs. While both are valid paths to gain exposure to private companies, they offer different levels of control, volatility, diversification, and fee structures. Understanding these key differences is a key part of making an informed decision that aligns with your investment goals.

Fund of funds (FoF) | Direct fund investment | |

Diversification | High: You get exposure to multiple funds and hundreds of companies at once. | Low: Your exposure is concentrated in the portfolio of a single fund. |

Manager selection | The FoF manager selects a portfolio of underlying fund managers for you. | You are responsible for performing due diligence and selecting the fund manager. |

Fees | Two layers of fees: one for the FoF and one for each underlying fund. | One layer of fees: paid directly to the fund manager. |

Access | Can provide access to exclusive or high-minimum funds. | Access is limited by fund availability and your ability to meet minimums. |

Compared to a direct fund investment, a FoF usually indirectly owns much smaller stakes in a much longer list of companies. If any one company does very well or very poorly, the impact on a FoF is thus reduced.

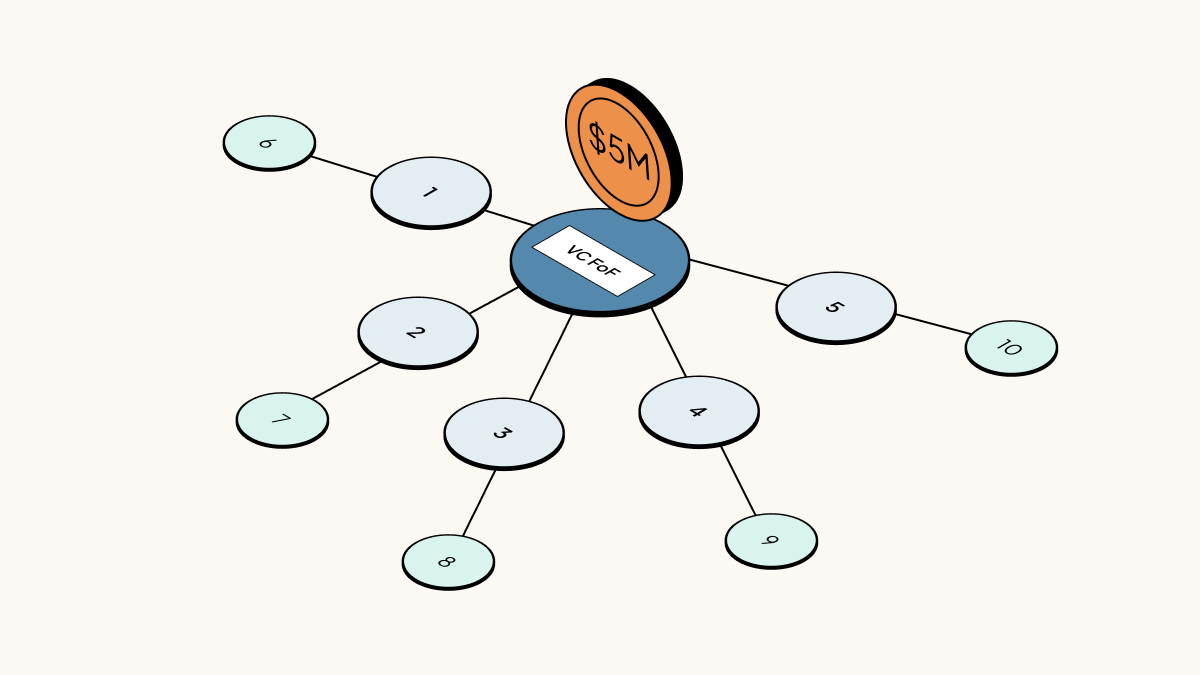

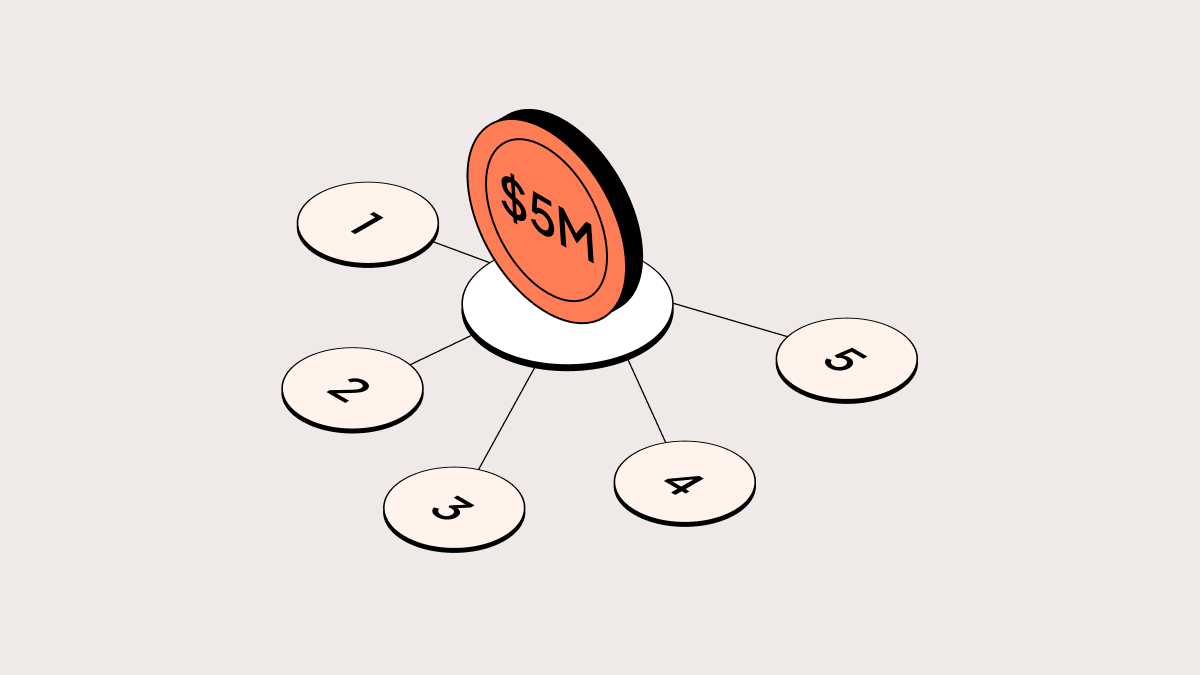

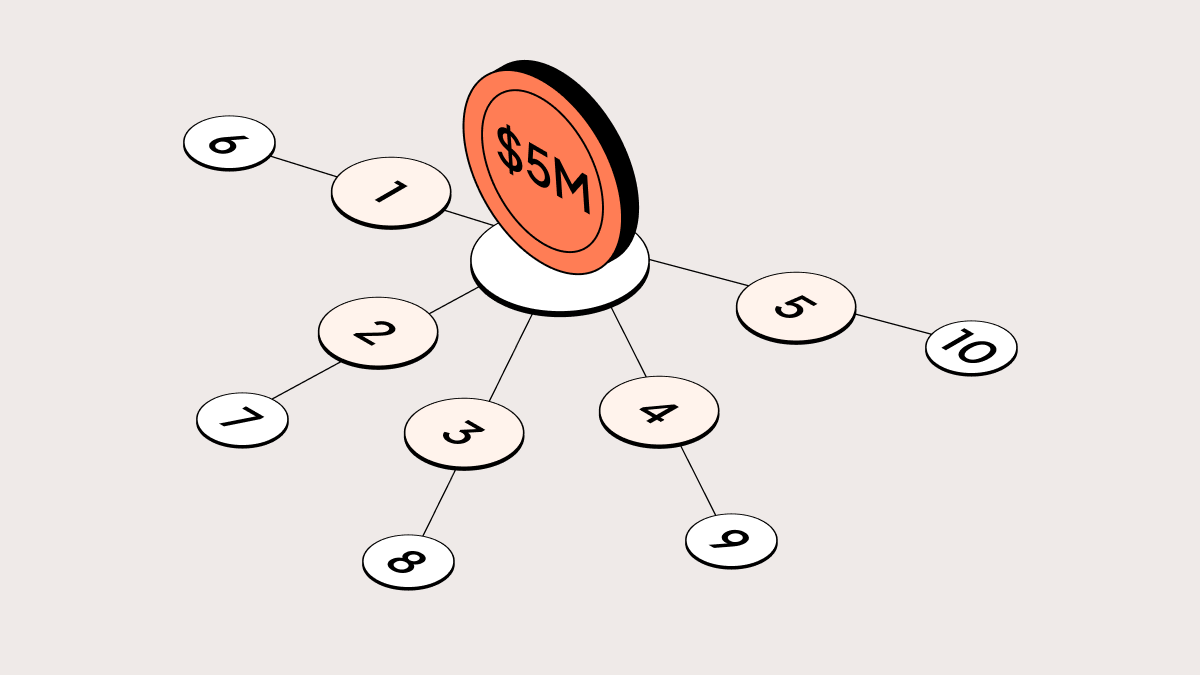

For example, if a hypothetical LP invests $5 million in a direct VC fund and the fund spreads that capital evenly over five investments, the LP will essentially have a $1 million stake in five different startups.

If that same LP invests $5 million in a FoF and that fund also spreads the capital evenly over five investments, the LP will essentially have a $1 million stake in five different funds. Each of those funds will still divide that capital further to make individual investments in startups. Spread across these different funds, that same initial $5 million investment might be able to acquire smaller stakes in many more companies.

This means a FoF is usually seen as a diversification play, offering investors exposure to a broader band of the marketplace than a direct fund. In general, investors expect a FoF to offer better downside protection but less upside potential than a fund that makes direct investments.

The operational complexities of a fund of funds

While the concept of a FoF is straightforward, its administration is uniquely demanding. The layered structure, with one fund investing in many other funds, creates a cascade of operational challenges for fund management that can overwhelm a fund CFO or controller who relies on manual processes and spreadsheets. These complexities require a high degree of precision, coordination, and sophisticated systems to manage effectively.

The double fee layer: Management and performance fees

A FoF has a distinct fee structure, including two layers of management fees, that fund managers must calculate and track with absolute precision. LPs in a FoF pay two layers of fees. The first layer goes directly to the FoF manager, and the second layer is indirectly paid to the managers of the underlying funds that the FoF invests in.

Both of these layers typically include two types of fees.

Management fee: This is a recurring fee, usually charged annually, based on the amount of assets under management. It covers the operational costs of running the fund.

Performance fee: Also known as carried interest, this is a share of the fund's profits that is paid to the manager, often after a preferred return or hurdle rate is met.

For this reason, some FoFs charge lower fees than the 2% management fee and 20% carry that is most common among direct VC funds.

Look-through reporting and data aggregation

LPs in a FoF expect to see "look-through" reporting. This gives them visibility into the underlying portfolio companies they are invested in through the various funds, a key component of effective portfolio monitoring. However, collecting the necessary financial data from dozens of different funds and their underlying portfolio companies is an immense challenge.

Each underlying fund may have its own reporting schedule and data format, with industry benchmarks often releasing preliminary quarterly returns that create a constant flow of new data points for the FoF manager to reconcile. Without the right technology, the FoF manager is left to manually chase down, normalize, and consolidate this information into a single, coherent report for their LPs. This process is not only incredibly time-consuming, as administrators must manage frequent updates to financial systems that create more complexity, but it’s also highly susceptible to errors.

For example, when it comes to valuing their investments, there is no widely accepted industry standard. This lack of consistency can undermine investor confidence, and as one investment partner notes, LPs may "question your credibility" if they perceive valuations to be too aggressive.

Portfolio valuation and SOI aggregation

A critical document for any fund is the schedule of investments (SOI), a financial statement that lists all of the fund's investments and their current values, which are determined through a process of portfolio valuation. For a FoF, creating an accurate SOI requires aggregating the SOIs from every single underlying fund in its portfolio. This is a monumental task of data collection, validation, and reconciliation.

The accuracy of the FoF's SOI is paramount, as it is the foundation for calculating the fund's overall NAV. Any delays or errors in obtaining valuation data from the underlying funds can create a significant bottleneck in the FoF's own financial reporting process, impacting all downstream outputs, including LP reports and the annual fund audit.

Capital call and distribution management

A capital call is when a GP requests committed capital from its LPs to make an investment; some firms use a capital call line of credit to bridge the timing gap. A distribution, which is governed by the fund's distribution waterfalls, is when a GP returns profits from a successful investment back to its LPs.

How Carta streamlines FoF administration

The operational burdens of FoF management demand a purpose-built platform, like fund administration software, designed to handle its unique complexities. Relying on spreadsheets and manual processes introduces unnecessary, higher risk and inefficiency. An integrated fund administration platform can turn these challenges into streamlined, automated workflows that provide control and clarity.

For firms like VCFA Group, which specializes in secondary investments, partnering with a trusted administrator provides a critical advantage. "We’d gotten a lot of feedback from certain investors that having an outside fund administrator involved would give them confidence in the reporting and in the security of communications," says David Tom of VCFA Group. "Carta is a known expert in the space, so it made those conversations easier."

A single source of truth for FoF operations

To solve the chaos of data aggregation, FoF managers need a centralized system that serves as a single source of truth for all fund activity. Carta's fund administration platform is built on an event-based fund accounting software that automates the consolidation of all financial activity from underlying funds.

This powerful infrastructure provides the FoF manager with a real-time, audit-ready view of the entire portfolio. It replaces the manual, error-prone process of chasing down and reconciling data from disparate sources, ensuring accuracy and freeing up the finance team to focus on more strategic work.

A transparent LP experience

Look-through reporting is a major pain point for FoF managers, but it's a critical expectation for their LPs who want to understand their investments. Carta LP Portfolio Analytics provides a direct answer to this challenge by giving investors a modern, transparent, and professional experience.

LPs receive a single, secure login where they can view their total commitment, see consolidated fund performance metrics, and access all of their documents in one place, including capital call notices and K-1s. These docs can be streamlined with a service like Carta Fund Tax: The portal creates a seamless experience that builds trust and reduces the administrative burden on the GP.

Portfolio construction and forecasting for FoFs

Beyond day-to-day administration, FoF managers need strategic tools to plan and manage their portfolios effectively. As Anubhav Srivastava, founder of Carta Fund Forecasting (formerly Tactyc), explains: "The type of questions my GPs would ask me would be, how much would we reserve for company A versus company B? The macro environment is changing, does our portfolio construction still stand? These are questions every fund manager asks themselves and the way these were answered were ad-hoc spreadsheets."

Fund Forecasting by Carta is a powerful forecasting and planning platform that replaces those ad-hoc spreadsheets. With fund forecasting software, FoF managers can model complex cash flows, plan for future capital needs, and forecast the performance of their entire portfolio of funds. This gives them the data-driven insights needed to make smarter capital allocation decisions and ultimately maximize returns for their LPs.

Take control of your FoF operations

Fund of funds offer a powerful strategic approach for accessing and diversifying within the private markets. However, their operational complexity means traditional, manual administration methods are no longer sufficient. Relying on spreadsheets and disconnected processes creates risk, inefficiency, and a poor experience for your LPs.

Carta’s Fund of Funds solution consolidates fund administration, portfolio analytics, and document management into a single platform—so you can finally replace the endless portal-juggling with a unified, technology-driven approach. Key capabilities include:

Agentic AI for accounting automation: Carta’s proprietary AI ingests and normalizes data from capital call notices, partner capital account statements (PCAP), and other key documents, automatically updating the general ledger and eliminating manual re-keying to streamline close and reporting cycles.

Deep portfolio look-through analysis: Analyze exposure and ownership data across your entire portfolio in one interface, manage compliance with the 5% GAAP disclosure rule, and run side-by-side GP valuation comparisons—all without manual aggregation.

Centralized capital activity hub: Track and act on all capital calls, distributions, and transfers from a single hub, replacing the fragmented experience of managing dozens of LP portals.

Comprehensive visual accounting: Trace capital flows from investment vehicle to individual asset with deal-level detail, giving you a real-time, audit-ready view of your entire portfolio.

Request a demo to see how Carta can streamline your fund of funds operations.

Frequently asked questions about funds of funds

After learning the basics of FoFs, you may still have some follow-up questions. Here are answers to a few common inquiries that can help clarify some of the finer points.

What is the difference between a fund of funds and an ETF?

A FoF is typically a private, actively managed fund that invests in other private funds, while an exchange-traded fund (ETF) is a publicly traded security that usually tracks a passive index of stocks or bonds.

What are the typical fee structures for a private equity fund of funds?

A PE FoF usually charges its own management and performance fees on top of the fees charged by the underlying PE funds, which each have their own PE fund structure and terms.

Can a fund of funds make direct co-investments?

Yes, many FoFs reserve a portion of their capital for co-investment opportunities, allowing them to invest directly into a portfolio company alongside one of their underlying fund managers.

How does look-through reporting work for LPs in a fund of funds?

Look-through reporting provides LPs with a detailed view of their indirect ownership in the individual companies held by the FoF's underlying funds, though compiling these reports is a major administrative challenge for the fund manager.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.