The timelines of VC funds tend to extend for a decade or more, so vehicles formed in the early 2020s still have plenty to produce the sort of attractive returns that their backers expect. So far, however, they’re off to a very slow start.

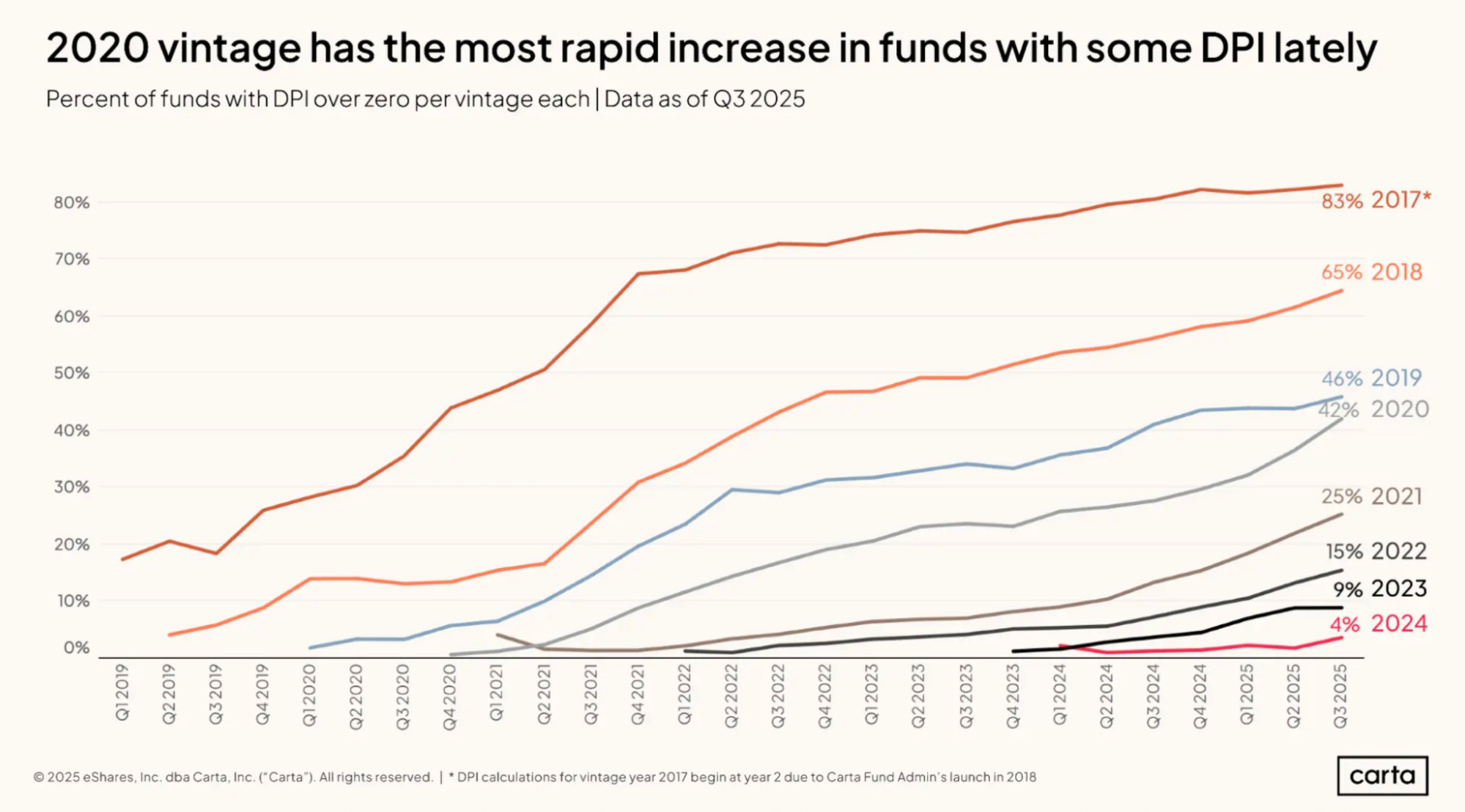

Through the end of Q3 2025, just 25% of funds in the 2021 vintage of VC funds on Carta had begun to generate any DPI, the primary metric by which fund managers measure their returns to LPs. In the 2022 vintage, only 15% of funds have any DPI to speak of.

The percentage of funds in these vintages that have begun to generate DPI has begun to rise over the past few quarters, according to Carta’s latest Fund Performance Report. But the vast majority of 2021 and 2022 funds are still waiting for their first concrete returns.

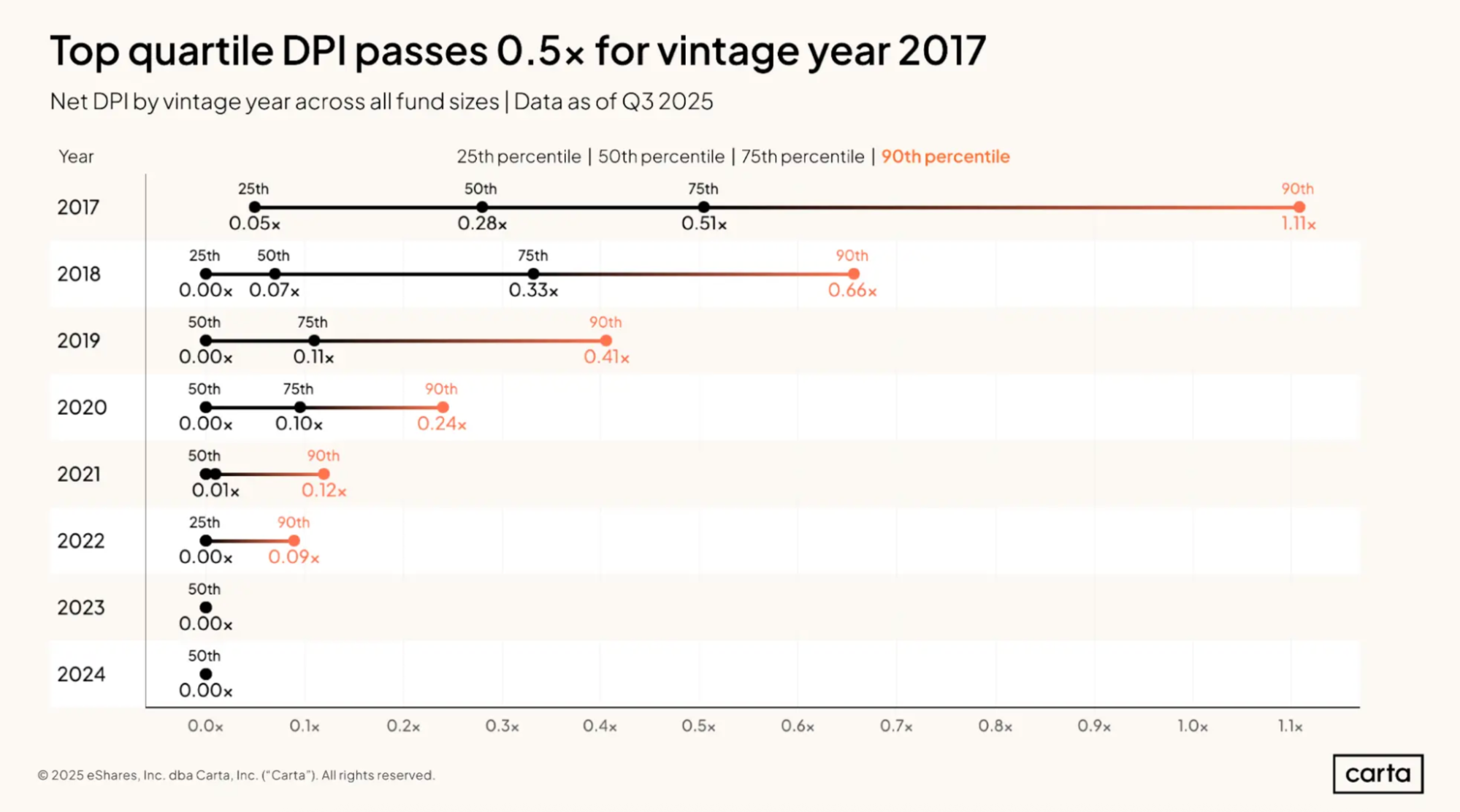

For those funds from 2021 and 2022 that have begun logging DPI, the scope of their returns to LPs has been minimal. In the 2021 vintage, the 90th percentile for DPI stood at 0.12x as of the end of Q3 2025, meaning that a top-decile fund from that year has returned a mere 12% of the initial capital that was paid in by investors. In the 2022 vintage, the 90th percentile for DPI is a touch lower, at 0.09x.

These low return profiles for such recent funds are expected, to a point. Venture funds typically have an initial investment period that lasts for five years, during which time they are primarily focused on finding new deals and helping their portfolio companies grow. It’s not until later in the fund lifecycle that generating returns through exits becomes a top priority. The above chart shows that the 2017 vintage—which is now nearly a decade old—is the only one from the past nine years where the median fund has begun to generate significant DPI.

For a range of macroeconomic factors, however, the 2021 and 2022 vintages—particularly 2021—may have real reason for concern.

These funds were raised during the peak of the recent venture bull market, when valuations across all stages of fundraising soared to new highs. And many of them deployed their cash very quickly, trying to strike while the iron was hot. In the middle of 2022, though, a widespread valuation reset occurred across tech, leaving many portfolio companies underwater from their previous valuations. Some of these startups have struggled ever since to get back to their peak valuations. And those struggles are exacerbated by the rise of AI, which left many companies that were formed prior to the AI revolution behind the technological curve.

As they were investing in what proved to be a challenging market, these funds also faced plentiful competition, making it harder to access the best deals. Year over year, the number of new venture funds formed on Carta increased by 132% in 2021. And in the years since, the exit environment for VC-backed startups has chilled.

The end result? A group of VC funds that invested in companies at exaggerated valuations and has found fewer options than expected for realizing any kind of return.

“The 2021 and 2022 vintages, those were probably years of irrational exuberance on the venture pricing side,” says Andy Triedman, a partner at Theory Ventures who invests in early-stage AI and machine learning startups. “I would say it matches this current era in exuberance, but probably without as strong of a fundamental technology story for why that cohort of businesses should generate a larger number of outsized returns and exits.”

Too soon for distress?

Triedman acknowledges that, for an investor in these VC vintages, this may be an intimidating combination of variables. But he also believes that there’s plenty of time to make up for a rough start—and that 2026 and 2027 will tell us a lot more about the eventual fate of these funds.

“In the overall DPI story, I am pretty optimistic,” Triedman says. “As this technology era continues to heat up and we have a lot of companies that are generating really amazing growth, I would expect we’re going to see a bunch of major exits in the next couple years. And that starts to really drive that DPI up quickly.”

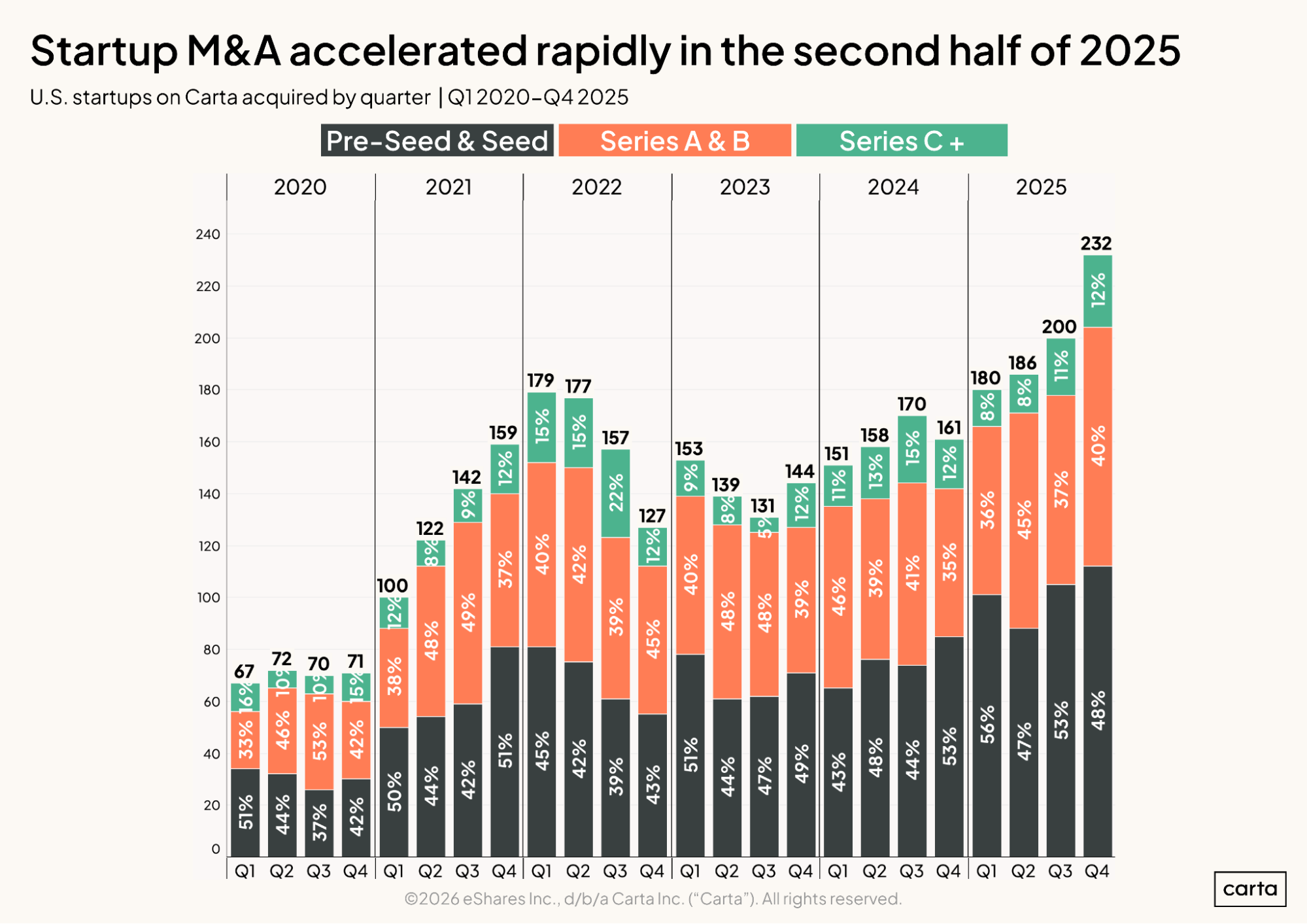

Perhaps the most promising fact for 2021 and 2022 managers is that the exit environment has already begun to revive. There were 202 IPOs in the U.S. in 2025 from companies that debuted with a market cap north of $50 million, marking a four-year high and a 35% increase over IPO count from 2024. Acquisition activity has also spiked: There were 25% more M&A deals targeting startups on Carta in 2025 than in 2024. In Q4 alone, there were 232 such deals, the highest total for any quarter so far this decade.

In her work with SSM Legal, which represents both VC funds and tech startups, co-founder Lindsey Mignano has seen this dynamic begin to play out. She says that for now, at least, the prospect of increased exit activity is taking the heat off 2021 and 2022 vintage funds.

“Anecdotally, I’m not hearing that [those funds are] facing a lot of pressure right now. But they also have time on the clock,” Mignano says. “We’ll see what happens this year. We know statistically that a lot of seed and Series A companies are getting acquired. We’ll see what that means economically—if that’s enough of their portfolio to make a meaningful return to LPs.”

Mignano also notes, however, that selling portfolio companies at the seed stage or Series A isn’t likely to result in the sorts of returns for VC funds that their investors expect. In many cases, she says, LPs anticipate a return between 3x and 5x on their venture fund allocations. To meet that benchmark, funds will need to find the sort of larger-scale exit opportunities that typically only exist at later stages.

“Acquisitions at Series A aren’t going to move the needle that much,” Mignano says. “They’re going to need a unicorn or two to make those numbers work. It’s just a math game.”

Changing startup timelines

The relative lack of exits in recent years is due in part to the valuation reset, which has caused many startups to delay their timelines in hopes that a friendlier pricing environment will emerge in the near future. But another factor is also at play: The top VC-backed companies today generally stay private for longer than ever before.

“There’s a secular trend toward the largest, the best companies, staying private longer,” Triedman says.

For both fund managers and their LPs, these longer timelines to exit could force an adjustment of expectations. It may take longer for funds from recent vintages to exit their most valuable positions than might have initially been anticipated, which means it may also take longer for significant returns to be realized.

The full picture of fund performance

Of course, there are ways to measure fund performance other than DPI, such as TVPI and IRR. But for active vintages, these other metrics rely in large part on estimates of company value, rather than proven market prices.

For funds that hold positions in foundational AI startups and other elite private companies—those that were busy raising billion-dollar rounds in 2025—strong TVPI and IRR numbers can assuage investor concerns. Other funds aren’t so lucky. And for every fund manager, in the end, DPI is the most concrete measure of success.

“If you were a 2021 or 2022 vintage fund and you made an early investment in a company that’s sitting at a really nice mark, I think LPs would be willing to accept limited DPI,” Triedman says. “But if a fund made a lot of investments in companies at pretty high valuations, and none of them are doing particularly well, and there’s no DPI, then I think it becomes a challenging environment.”

It’s worth emphasizing again that funds from 2021 and 2022 might be less than halfway through their lifespans. Fund performance can change drastically over time. It can also change drastically from one vintage to the next. In terms of IRR, for instance, the top funds from the 2023 vintage are already showing significant promise.

This sort of variability is what investors expect. If the 2021 vintage ends up with poorer returns than most, it won’t be great for the managers of those funds and their LPs. But the broader VC ecosystem will be just fine.

“That’s why LPs care a lot about time diversity, because they understand that fund returns are extremely correlated to their vintage year,” Triedman says. “There are some vintages where every fund does great, and some vintages where almost no funds made any money.”

Subscribe to the Data Minute newsletter

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.