Interest rates are falling again. And VCs are paying close attention.

The Federal Reserve approved its third consecutive cut in December, reducing its target borrowing rate to a range of 3.5% to 3.75%. That’s down from a recent range of 5.25% to 5.5% that was in place across much of 2023 and 2024—the highest effective Fed rate in more than 20 years.

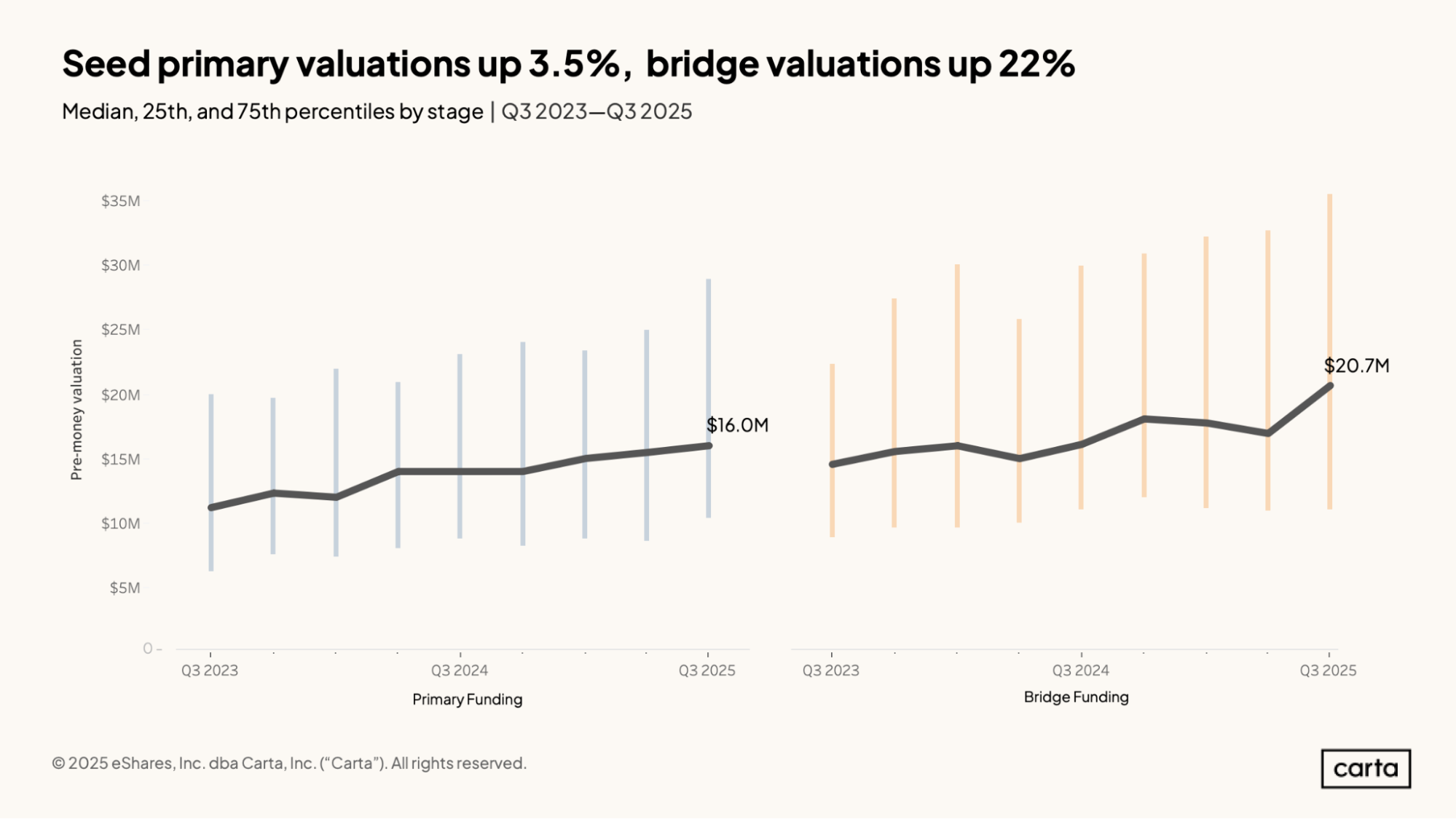

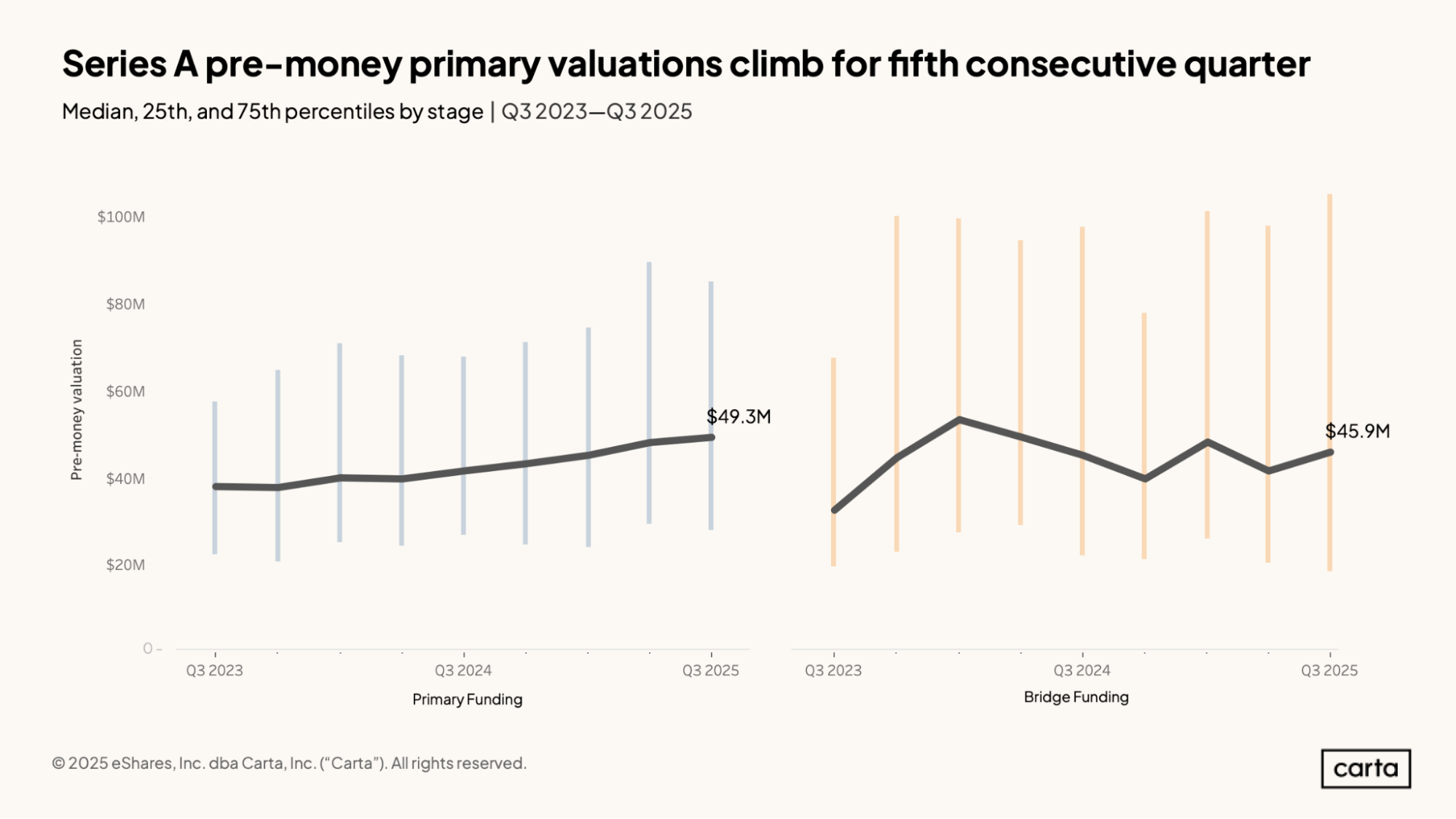

At the same time, early-stage venture valuations have been on the rise, climbing to record highs. For instance, the median valuation for new primary seed rounds on Carta was $16 million in Q3 2025, up 14% year over year. At Series A, the median valuation rose by 19% over the same span.

For private investors, there’s a clear connection between these twin trends. Historically, when interest rates decline, venture-backed valuations tend to rise.

The market experienced an extreme version of this inverse correlation in the early 2020s, when interest rates dropped to near zero in the wake of the COVID panic. This coincided with a record-breaking time in the venture industry, with deal activity and valuations soaring to new highs.

When Blueprint Equity Managing Partner Bobby Ocampo considers the venture landscape today, he sees some familiar signs.

“With rates doing what they’re doing and a lot of money flowing into the category as a whole, you’re seeing pricing certainly move up,” Ocampo says. “It’s sort of mirroring the period of 2021 and the beginning of 2022—you’re seeing that with pricing. It is pretty aggressive right now.”

Why interest rates and valuations are connected

Interest rates are often a key variable that helps determine where investors of all kinds choose to deploy their capital. When rates are high, capital tends to flow into shorter-term asset classes that are in some way pegged to interest rates, such as private credit, short-term bonds, or other types of fixed income. When rates are lower, these assets can grow less attractive, leading investors to seek higher yields via other avenues.

One of these alternatives is venture capital, which is traditionally seen as a high-risk asset class that operates on much longer time horizons—the opposite of something like short-term bonds.

“When rates decline, the relative attractiveness of long-duration assets improves,” says David Roos, a partner at Core Innovation Capital. “And startups and private companies are among the longest-duration assets out there.”

This flight of capital into VC in the face of falling interest rates is exactly what happened in 2020 and 2021. But recent history also shows how quickly the market can reverse course. The era of near-zero rates came to an end, and the Fed rate started to escalate rapidly in 2022 and 2023. This coincided with a widespread slowdown in venture activity, as some of the investors who had rushed into the space in previous years decided to pull back.

With less capital and less competition across the VC market, valuations broadly declined.

This pullback left many of the funds that had been racing to deploy capital in 2020 and 2021 overexposed, holding assets that were no longer as valuable as they used to be. While the current lowering of rates may very well draw more investors back into venture, Ocampo believes they shouldn’t get carried away.

“A lot of people put a lot of money to work in that one vintage year (in 2021), and we found that it’s coming back to bite funds,” Ocampo says. “And so we’re trying to be very cautious.”

Why today’s market is different

While today’s venture environment may rhyme with that of four years ago, there are also several significant ways in which it differs. At least for now, it seems unlikely that the market is headed for a beat-for-beat repeat of the early 2020s.

One reason is that current interest rates are still relatively high—higher than they were at any point during the whole of the 2010s—and the pace of rate cuts seems set to slow down in 2026. Even though rates have begun to decline, there are still plenty of places other than venture capital where investors can find yield.

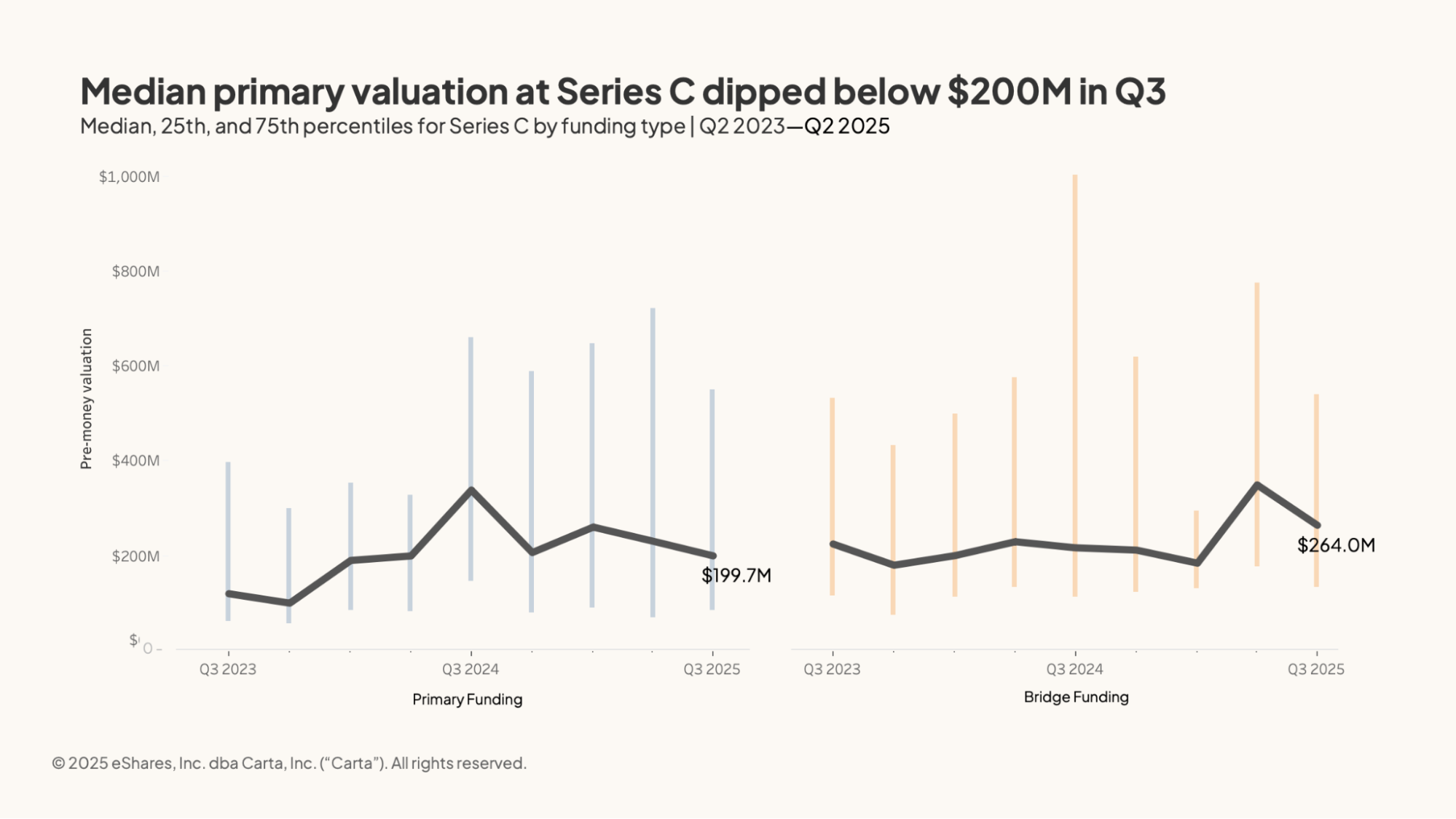

Another point of contrast is that, while early-stage valuations are currently on the rise, later-stage valuations have been holding steady, or even declining. The median primary valuation on Carta at Series C, for instance, is down 41% year over year.

Plus, venture deal counts have not been skyrocketing like they did in the early 2020s. In fact, quarterly deal activity is currently mired in a downward trend. The market-wide froth that permeated the venture industry in 2021 does not exist today.

Another key difference: What froth that does exist in the current market can largely be attributed to booming valuations and ongoing bullishness around AI. There doesn’t appear to be a broader secular trend of increased market interest in VC so much as aggressive optimism around the future of one particular set of technologies.

“There are clear echoes of 2021 in today’s market, especially in the way capital is chasing AI,” Roos says. “[But] most sectors are not experiencing 2021-style pricing. LPs are highly selective, and management teams are still operating with a strong focus on efficiency and burn control.”

Finally, as Roos indicates, there’s the attitudes and strategic approach of investors. Some of the investors who poured capital into VC during the recent boom time quickly came to regret their aggression, and the early 2020s are still close enough that investors remember well the lessons they learned.

“The big difference is discipline,” says Andrejka Bernatova, the founder, CEO, and chairman of Dynamix, an energy-focused investor. “In 2020 and 2021, near-zero rates collided with a huge amount of capital and very little focus on fundamentals. …Today, investors are much more conscious of entry price, real cash generation, and the need to be operationally involved.”

Roos agrees. At least for now, the VC market’s renewed focus on fundamentals has remained in place.

“The scars from the last correction are fresh, and that’s keeping most of the market grounded,” he says. “Even with declining rates, we’re not returning to an era of ‘free money.’”

What it means for startups and investors

Venture investors can have a wide range of opinions on many market-related matters, but most of them agree that it’s difficult to predict the future. Interest rates might continue to fall in the months to come. They might stay where they are. Or they might once again start to rise.

Regardless of what comes to pass, the current status of the market has some notable implications for startups and investors.

One of these, Ocampo says, is that it could be a good time for some startups to pursue venture debt funding on more attractive terms than could be found in 2023 and 2024. In some cases, startups might raise debt funding because they need capital. But venture debt can also be a strategic move: A startup might try to strike while the iron is hot by securing a line of credit at relatively low rates that it can tap in the future.

“Because of what rates are doing, securing venture debt or lines of credit can be very attractive,” Ocampo says. “That’s probably one area where we’re more focused—can we lock in these really attractive rates right now, more so than raising relatively cheap equity at high prices.”

The combination of falling interest rates and rising early-stage valuations may look familiar to VCs. But if investors continue to practice prudence and focus on the underlying economics of the companies that come to market, it seems unlikely that history will repeat itself.

“Falling rates are not a license to repeat 2021,” Bernatova says. “They should be viewed as an opportunity to reset around fundamentals. The managers who will outperform are the ones that are truly hands-on, bring in the right operating teams, and focus on turning companies into profitable, durable businesses.”

Sign up for the Data Minute newsletter

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.