Historically, it’s been difficult to glean much detailed information about the hows, whats, and whys of private fund economics. This is because these funds are, well, private. The public might be aware of how much capital a private fund raises, or what companies it invests in, or even some information about how the fund performs. But many of the details of how private funds operate have remained behind the curtain until now.

With this 2025 Fund Economics Report—the first of its kind—Carta aims to provide a never-before-seen glimpse at some of the latest data on how venture capital and private equity investors manage and operate their funds.

Who do fund GPs raise capital from? How much of their own capital do they contribute? How quickly do fund managers call down capital—and how quickly do LPs respond? What are the typical management fees and carried interest rates for recent venture funds? How do fees change over time? What are the largest fund-related expenses that GPs and LPs must consider?

Leveraging data from some 2,000 private funds that rely on Carta for fund administration, this report offers a look under the hood at many of the key financial and operational details that are critical to raising, managing, and investing in private funds. With these insights in hand, fund managers and their LPs can make better, more informed decisions about how and where to invest in an ever-evolving private capital landscape.

Highlights

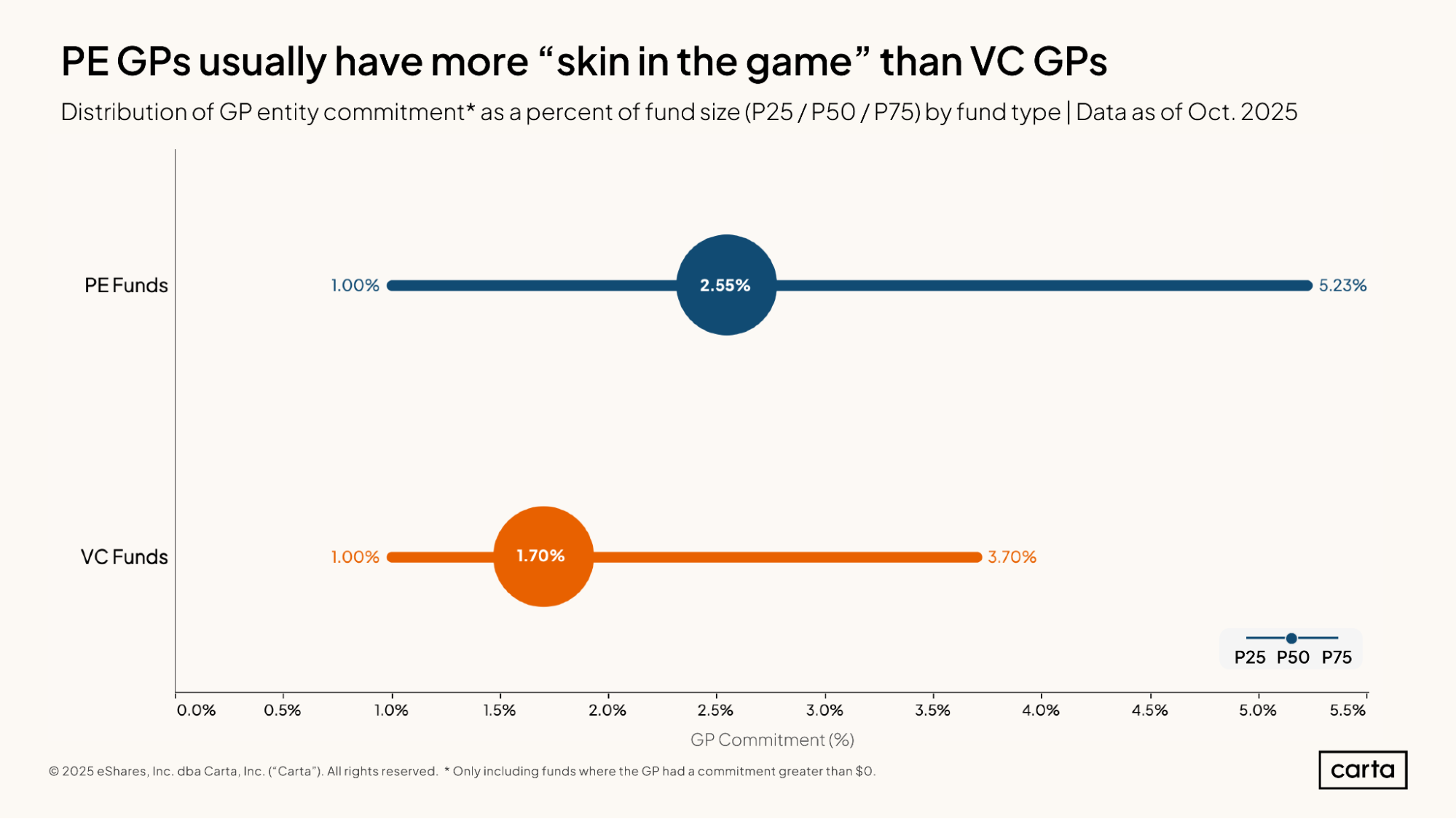

PE fund managers have more skin in the game: In venture capital, the median fund manager makes a GP entity commitment totaling 1.7% of the fund size. In private equity, the median GP entity commitment is 50% higher, at 2.55%.

Most capital calls are fulfilled on time: Across all recent fund VC vintages, at least 75% of capital calls to LPs are fulfilled at or prior to the given deadline. The longer the notice period given for a capital call, the more likely LPs will wire the capital earlier than requested.

Venture funds from 2022 are spending more slowly: After nearly four years, the median 2022 vintage VC fund had deployed 67% of its capital. Most other recent vintages had deployed around 80% of their capital at the same threshold in time.

Management fees and carry rates have remained steady: Across all recent VC vintages, the 2-and-20 fee structure remains the norm, with a median management fee during the investment period of 2% and the median GP taking 20% of a fund’s profits in carried interest.

Venture funds benefit from economies of scale: The median VC fund between $1 million to $10 million spends about 3.4% of its fund size on operating expenses within the first five years. The median fund larger than $100 million only spends 1% of its fund size on expenses in the same time frame.

Partner commitments

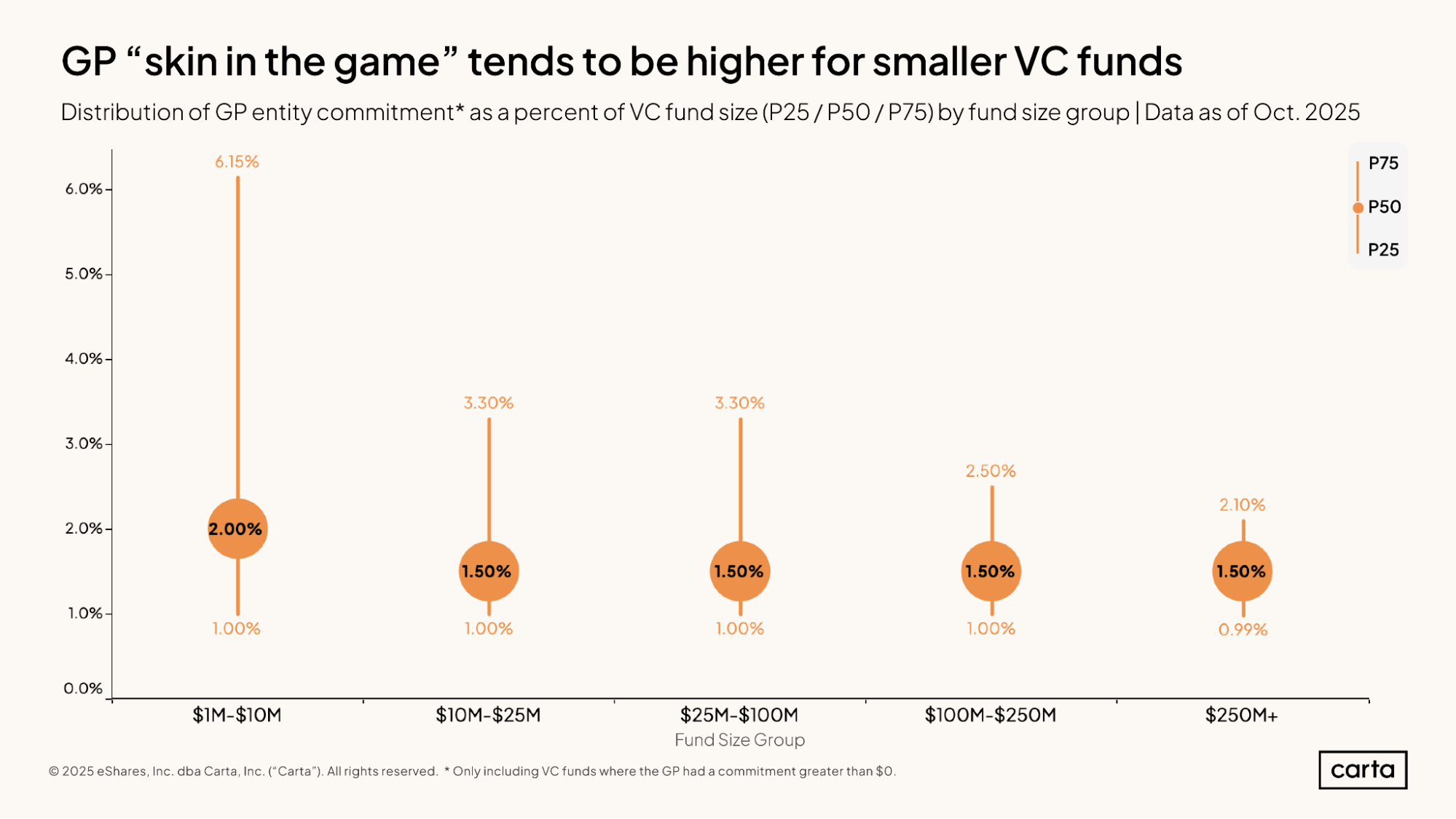

GPs managing smaller venture funds tend to have more skin in the game—measured by the size of their commitment as a percentage of total fund size—than GPs of larger funds. Smaller funds also tend to have a much wider range of common GP commitment sizes.

For instance, the median GP entity commitment on Carta among funds between $1 million and $10 million is 2% of the total fund size, while the 75th percentile for GP commitment is 6.15% of fund size. For funds between $25 million and $100 million, the median GP commitment drops to 1.5% of fund size, while the 75th percentile is 3.3%. At the upper end of the spectrum, there’s even less variability: The median GP commitment at VC funds larger than $250 million is 1.5%, and the 75th percentile is 2.1%.

On an absolute basis, however, larger funds typically have much larger GP commitments. For a $5 million fund, 2% of the fund (the median for vehicles of this size) equates to a commitment of $100,000. For a $250 million fund, a 1.5% commitment would total $3.75 million.

Private equity fund managers typically have more skin in the game than their peers in venture capital. Across venture funds of all sizes, the median GP entity commitment totals 1.7% of overall fund size. In private equity, the median GP commitment is 50% larger, at 2.55%.

For both VC and PE funds, the sizes of GP commitments follow a right-tailed distribution, with some managers having substantially more skin in the game than the median. But this distribution is wider in PE than in VC. The 75th percentile for skin in the game among PE funds is 5.23%, compared to 3.7% for VC funds.

Full report available: Start reading now for free

Our complete Fund Economics Report 2025 includes more than 20 additional charts on capital calls, capital deployment, management fees, carry and waterfall trends, operating expenses, and more.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.