After the record-setting levels of activity seen during the early 2020s, nearly every segment of the VC market has seen some kind of dealmaking slowdown during the past three years.

In the first half of 2025, however, the Series A market was particularly sluggish.

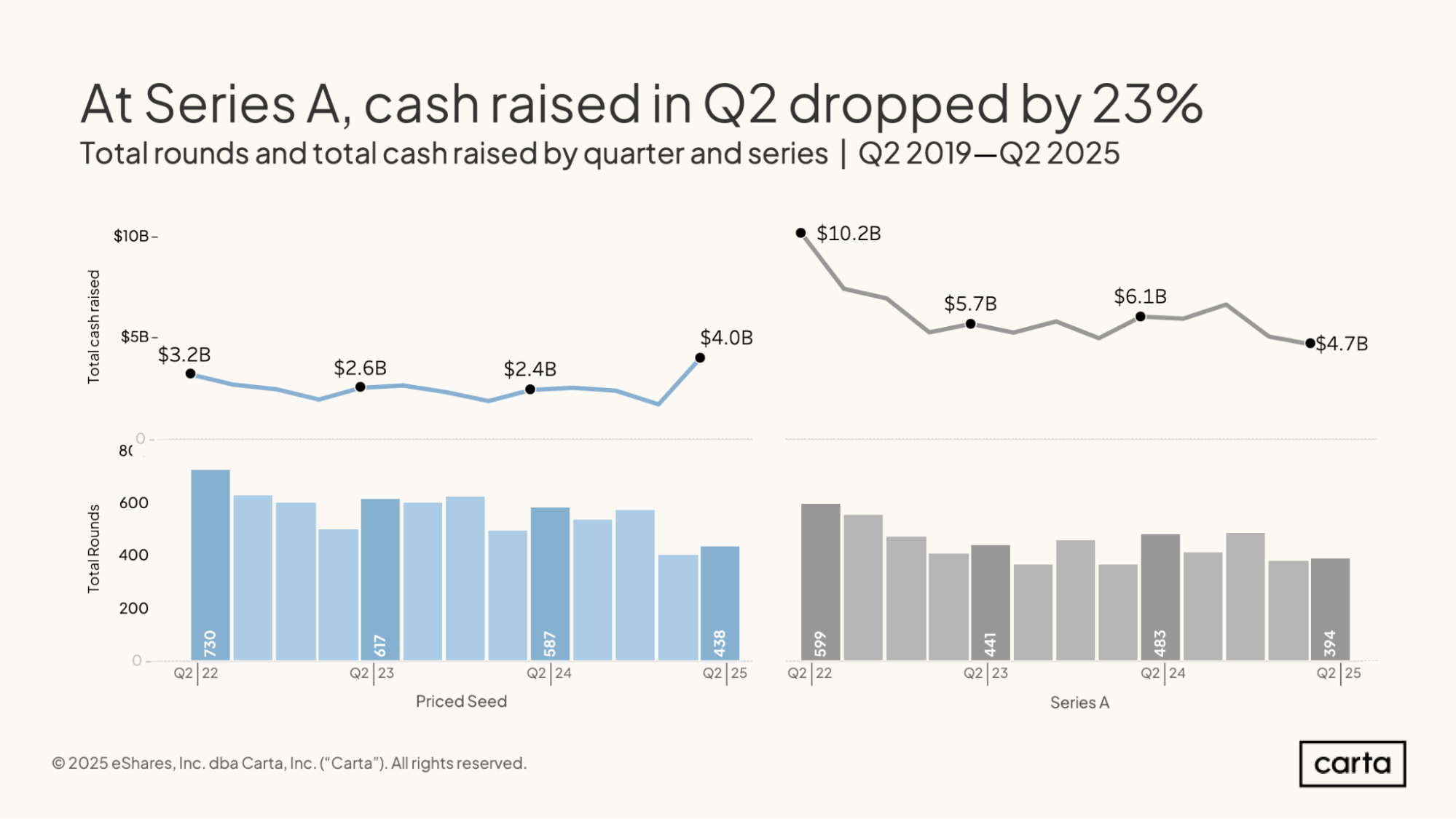

Series A deal count was down 18% year over year in Q2, according to Carta’s latest State of Private Markets report. And total cash raised was down another 23%, falling to $4.7 billion. A year ago, it looked like Series A activity was starting to recover after its post-pandemic dropoff: Deal count in Q2 2024 increased 10% year over year and cash raised climbed by 7%. This year, however, that progress reversed, and the dropoff has resumed.

Compared to Q2 2022—near the peak of the VC industry’s pandemic bull market—the changes are more severe. Over that timeframe, quarterly cash raised at the Series A stage has fallen by 54%, while deal count declined by 34%.

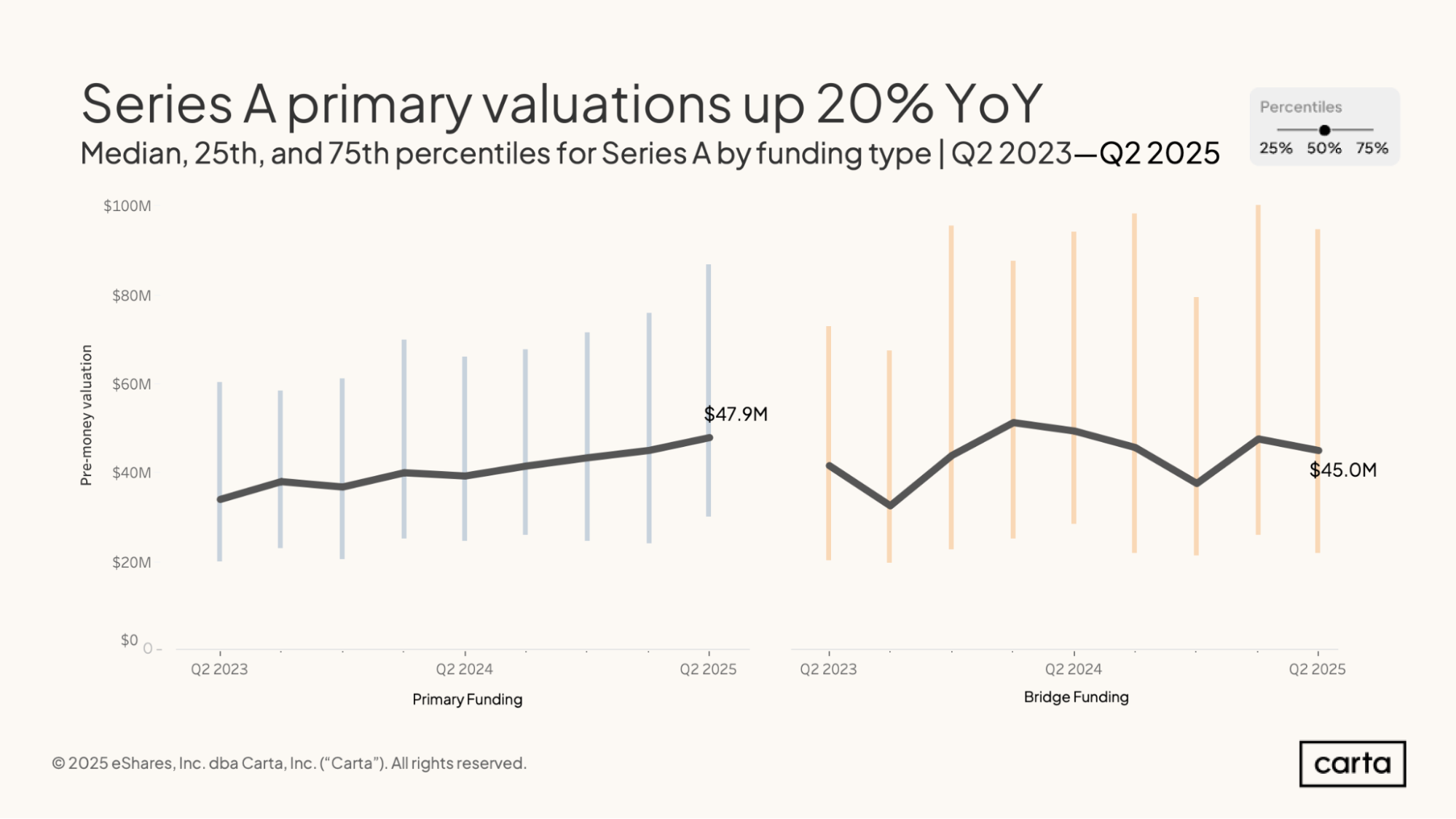

But the fundraising trends for Series A startups are not all pointing downward. At the same time that deal counts and cash raised have been falling, valuations on primary Series A rounds have been in a state of steady ascent. In Q2, the median Series A valuation rose once again, reaching a new high of $47.9 million.

Why the Series A market is shifting

Fewer deals, less cash raised, and higher valuations. What’s behind this ongoing transformation of the Series A fundraising market?

On some level, investors say it’s one version of a broader story that’s been playing out across much of the venture industry, regardless of stage or sector. Many investors have grown more patient and pickier about the deals they choose to pursue; for the right target, however, they’re still willing to pay a lofty price.

Two or three years ago, Marcos Fernanez saw companies with less than $1 million in annual recurring revenue successfully raising Series A rounds. Today, he might expect a Series A startup to be closer to $5 million or even $10 million in ARR.

“Quantity is down, and quality is up,” says Fernandez, managing partner at Fiat Ventures, an early-stage firm that invests in fintech startups. “There are fewer Series As taking place, but those that are taking place are raising capital at higher valuations.”

In some cases, valuations are much higher. As shown in the chart above, the 75th percentile for Series A valuations rose north of $80 million in Q2. Another 25% of all Series A valuations from Q2 were even higher than that.

Much of this increase is due to excitement in a few key sectors, according to Felix Hartmann, founder and managing partner of Hartmann Capital, an early-stage firm that invests in frontier technology. In some areas, such as certain subsets of robotics or AI, VCs see the potential for markets that could eventually be worth hundreds of billions of dollars—or perhaps even larger sums.

“The places where we see inflated valuations are the types of ideas that have the capacity to be trillion-dollar plays,” Hartmann says. “You’re seeing these outlier valuations in places like humanoids or AI research labs.”

The changing face of Series A

In other cases, rising valuations result from companies simply improving their strategic and financial position. Since the macro market shifted in 2022, investors have drilled into their founders the importance of growing efficiently in the early stages and delivering revenue and a path to profitability as soon as possible. In Hartmann’s experience, these lessons have sunk in.

“Most of our companies cut their burn in the last year,” Hartmann says. “Yet virtually all of them also increased their revenue.”

For Series A investors seeking companies poised for explosive future growth, that can be an attractive combination. In some cases, the ability of early-stage startups to operate efficiently and increase early-stage revenue has been aided by the rise of AI, allowing smaller teams to supersize their development capabilities.

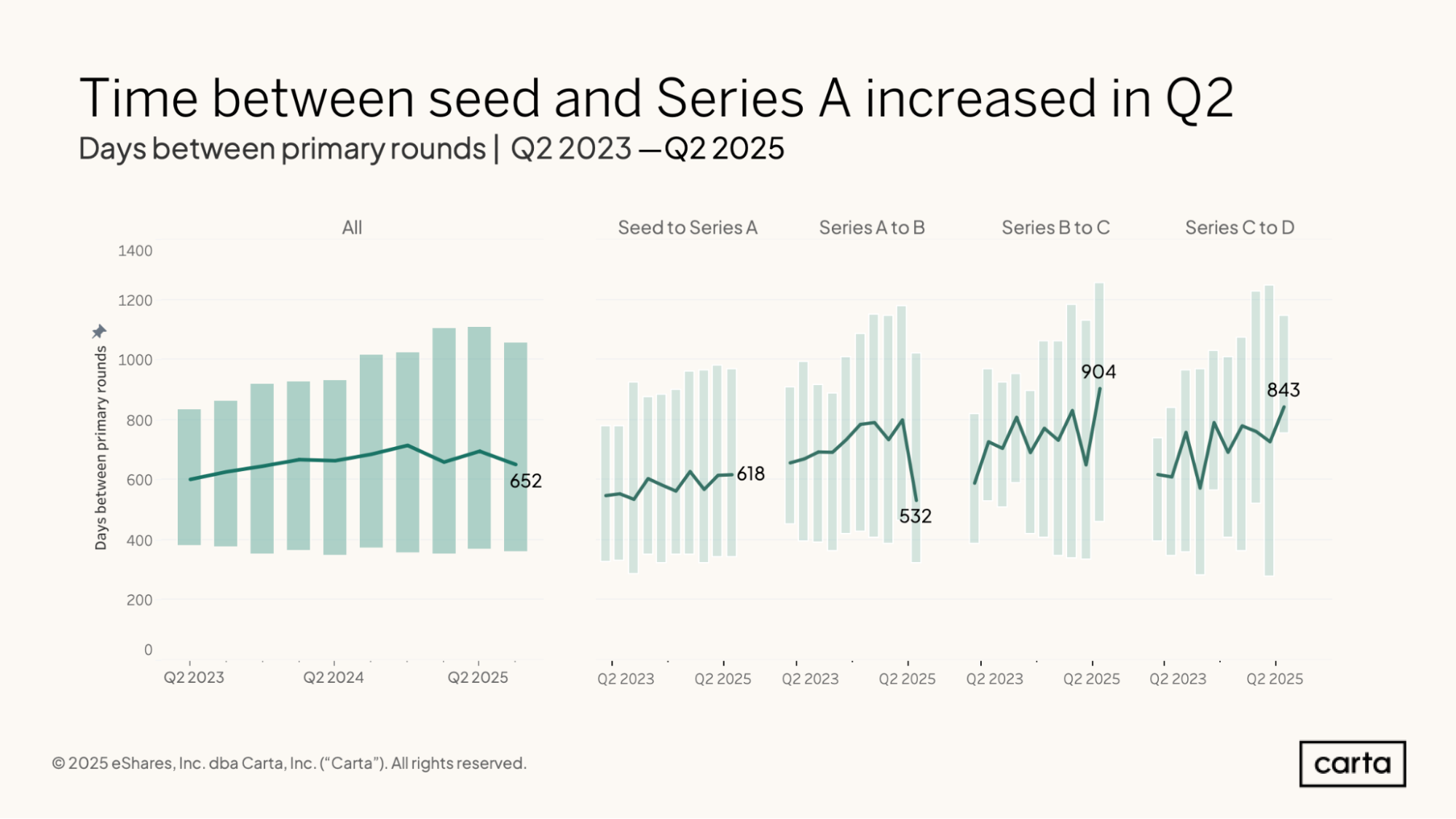

The timelines of Series A fundraising are also changing. In the past two years, the typical wait time between a seed round and a Series A has been trending up. The median interval reached 616 days in Q2, or a little more than 20 months. That’s more than two months longer than the median wait time between a seed and a Series A two years ago.

As investors raise their expectations for revenue and other financial metrics, some companies will take longer to reach the bar.

“Investors are being a lot more patient about when they deploy capital,” Fernandez says, “and expectations around what it means to be Series A-ready continue to stretch.”

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.