Executive summary

During the second quarter of 2025, the typical venture investment got a little bit smaller.

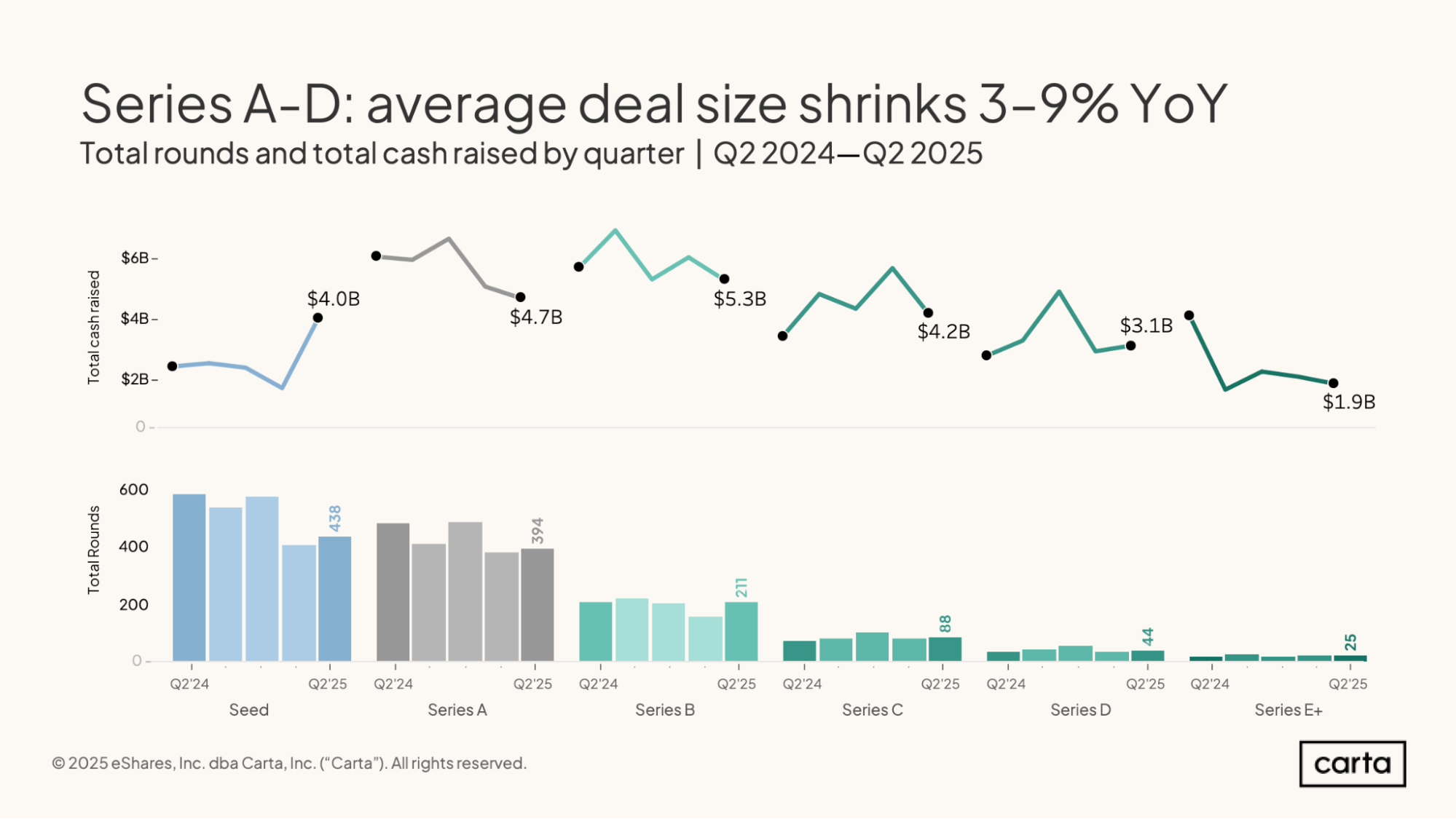

At every stage from seed through Series D, there were more new venture investments on Carta in Q2 than there were in Q1. At the same time, total cash raised declined quarter over quarter at Series A, Series B, and Series C, and increased slightly at Series D.

As a result, the average venture round size is shrinking across most of the startup lifecycle. Average check size in Q2 was down at every stage from Series A through Series D, with declines landing between 3% and 9%.

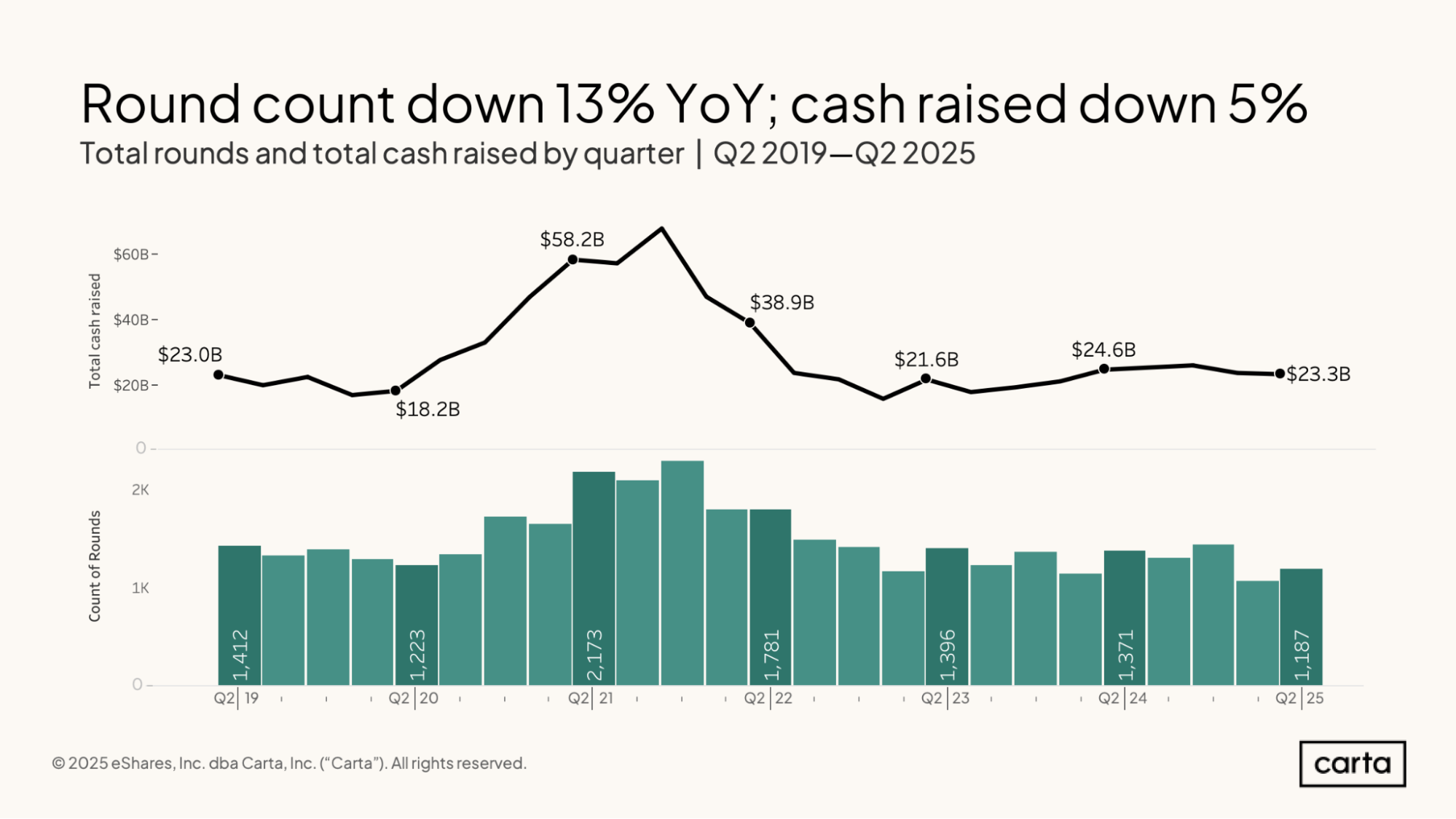

Venture deal counts were higher in Q2 than in Q1. But on a longer timeline, activity remains relatively diminished. Across all stages in Q2, startups on Carta closed 1,187 new venture rounds, down 13% year over year. Across the whole of H1, deal count is down 10% compared to 2024.

At the same time, startup valuations in new funding rounds continue to trend up, at least at the early stages. At both seed and Series A, the median valuation was higher in Q2 than it’s ever been before. In just the past year, the median valuation on primary rounds at Series A has risen by 20%.

Combine these various fundraising trends together, and a picture starts to emerge of how the venture capital industry is shifting in the early days of the AI age. Investors have grown more selective in their investments, leading to fewer deals. Aided by AI, many companies can do just as much (or more) with less funding, reducing the need for enormous checks. And the rising tide of valuations shows that VCs believe that many of these young, lean startups are poised for explosive, lucrative growth in the years to come.

Q2 highlights

SaaS, hardware see a funding surge: SaaS startups on Carta combined to raise $9.7 billion in Q2, a 91.2% increase from the same period two years ago. Over that same span, cash raised by hardware startups has risen by 110.4%.

Time between rounds ticks up: The median wait time between new funding rounds across all stages reached 696 days in Q2. That’s a slight increase both quarter over quarter (up 5%) and year over year (also 5%).

The Bay Area’s fundraising bump: In the past two years, the map of venture fundraising in the U.S. has tilted even further toward Silicon Valley. Startups in San Francisco raised $36.7 billion in Q2, up 138% from two years earlier. Fundraising in San Jose is up by 14% over the same span.

Key trends

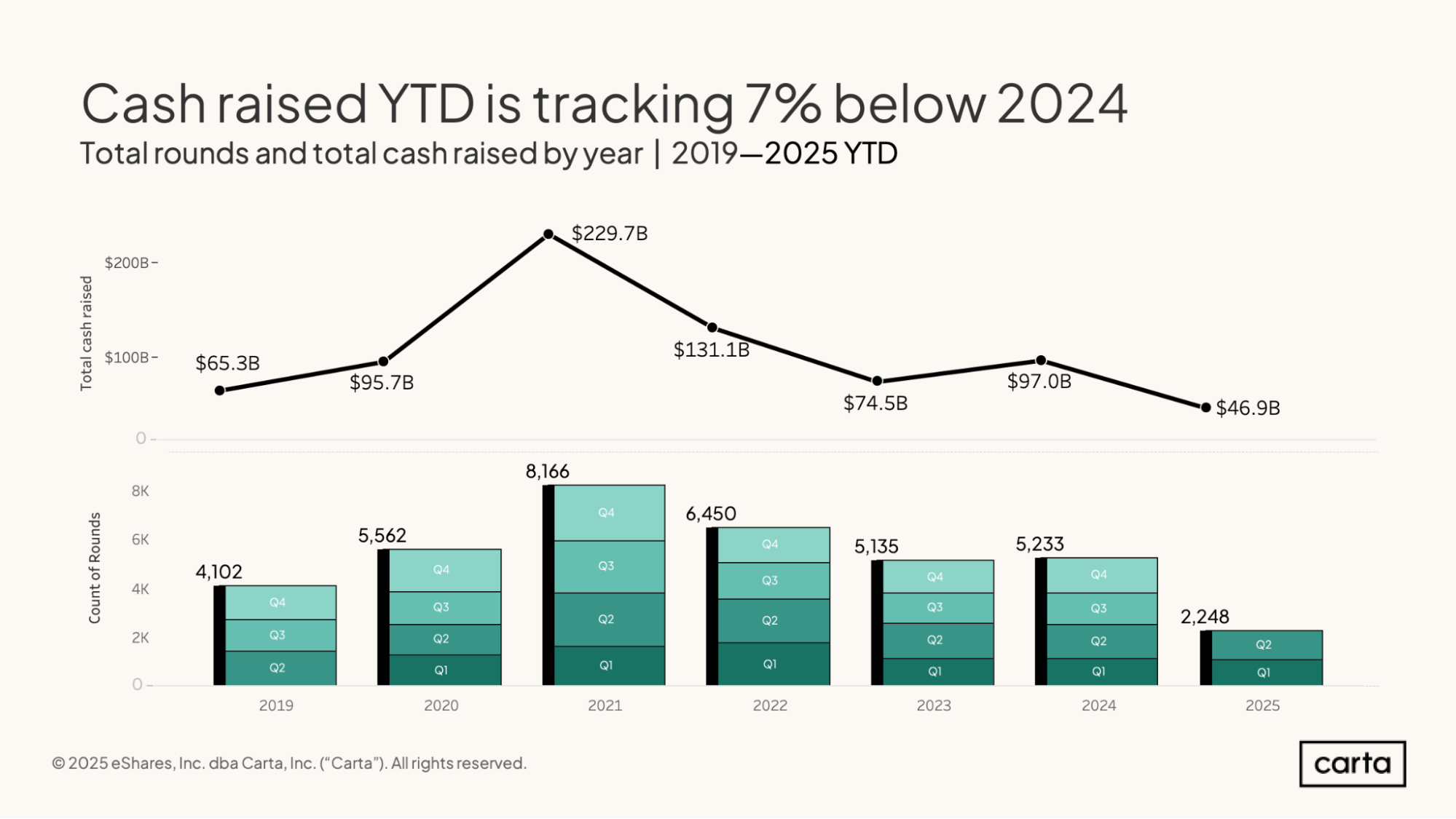

Through the first half of 2025, companies on Carta combined to raise $46.9 billion in new venture capital across 2,248 funding events.

In terms of cash invested, this year is pacing slightly behind 2024; if we extrapolate H1 2025’s total over the full year, we get $93.8 billion, just shy of last year’s $97 billion. The pace of new investments taking place has slowed down more substantially. Compared to H1 of last year, deal count in H1 2025 was down 10%.

Compared to a year ago, companies on Carta raised 13% fewer venture rounds this Q2. This marks the fourth consecutive Q2 in which the number of new investments has declined on a year-over-year basis. Total cash raised in Q2 also declined year over year, falling by 5%.

Despite this recent downward movement, both total round count and total cash raised by startups on Carta has remained relatively consistent over the past 10 quarters. Dating back to Q4 2022, most quarters have seen between 1,100 and 1,400 new investments and between $20 billion and $25 billion in cash raised.

Compared to the previous quarter, Q2 saw an increase in venture deal count at every stage from seed through Series D. At the same time, however, total cash raised in Q2 declined at Series A, Series B, Series C, and Series E+. While more venture investments were taking place, the amount of total cash going into those investments was shrinking.

The seed stage was a major exception to this trend, with cash raised spiking all the way to $4 billion in Q2. This is primarily due to a single large outlier investment—but even without that outlier, transaction value at the seed stage would have been slightly up in Q2 on a quarter-over-quarter basis.

Full report available: Start reading now for free

Our complete State of Private Markets Q2 2025 report includes 20 additional charts and analysis on fundraising and valuation at all stages, deal terms, dilution, geographical trends, and more.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.