Executive summary

By nearly every measure, 2025 was a strong year for startup fundraising, capping a multi-year recovery from the market reset of 2022 with capital, valuations, and deal terms all trending in founders' favor. But the interest in AI is not just infusing much-needed capital into the private markets; it's fundamentally changing what normal looks like.

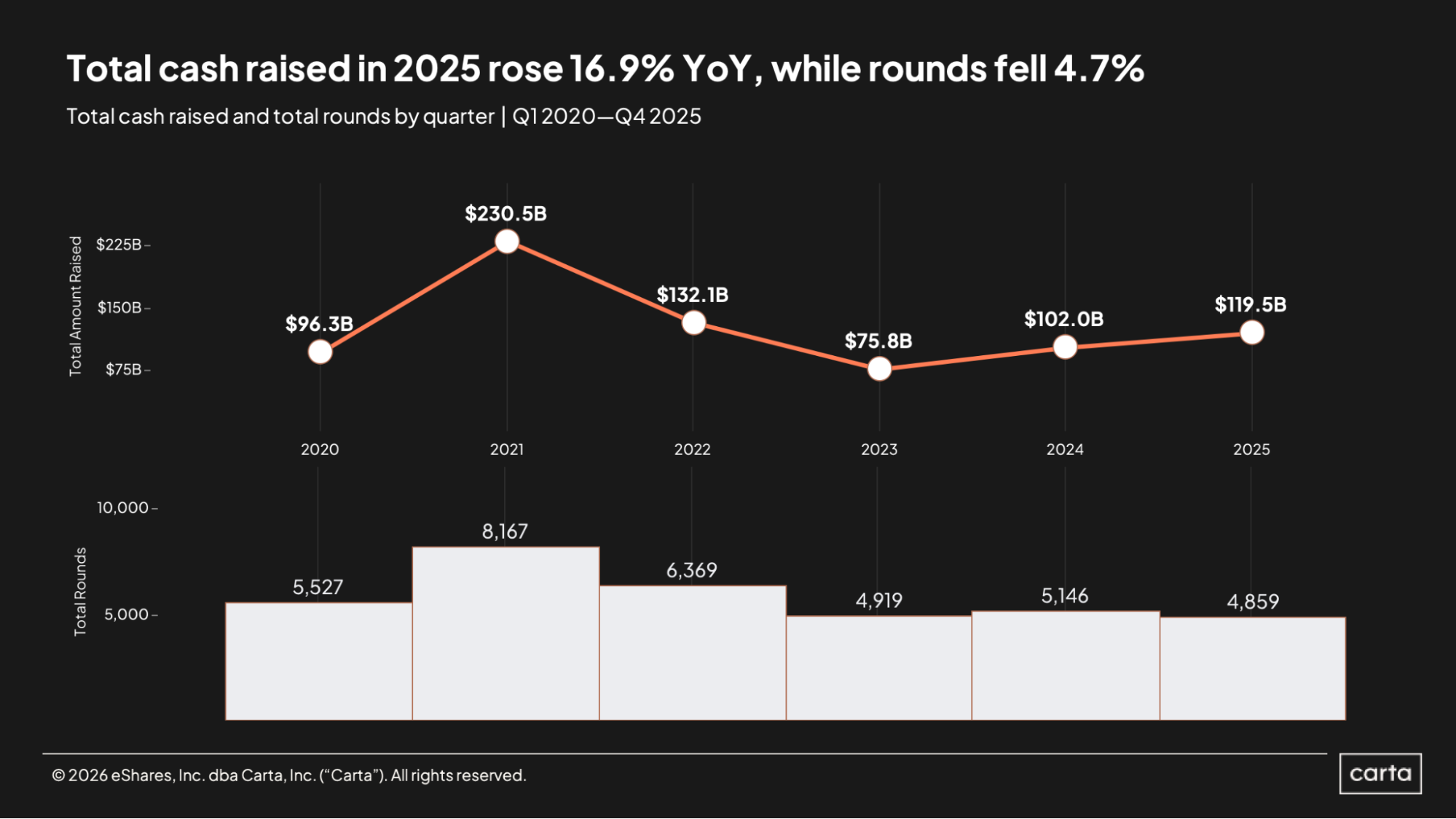

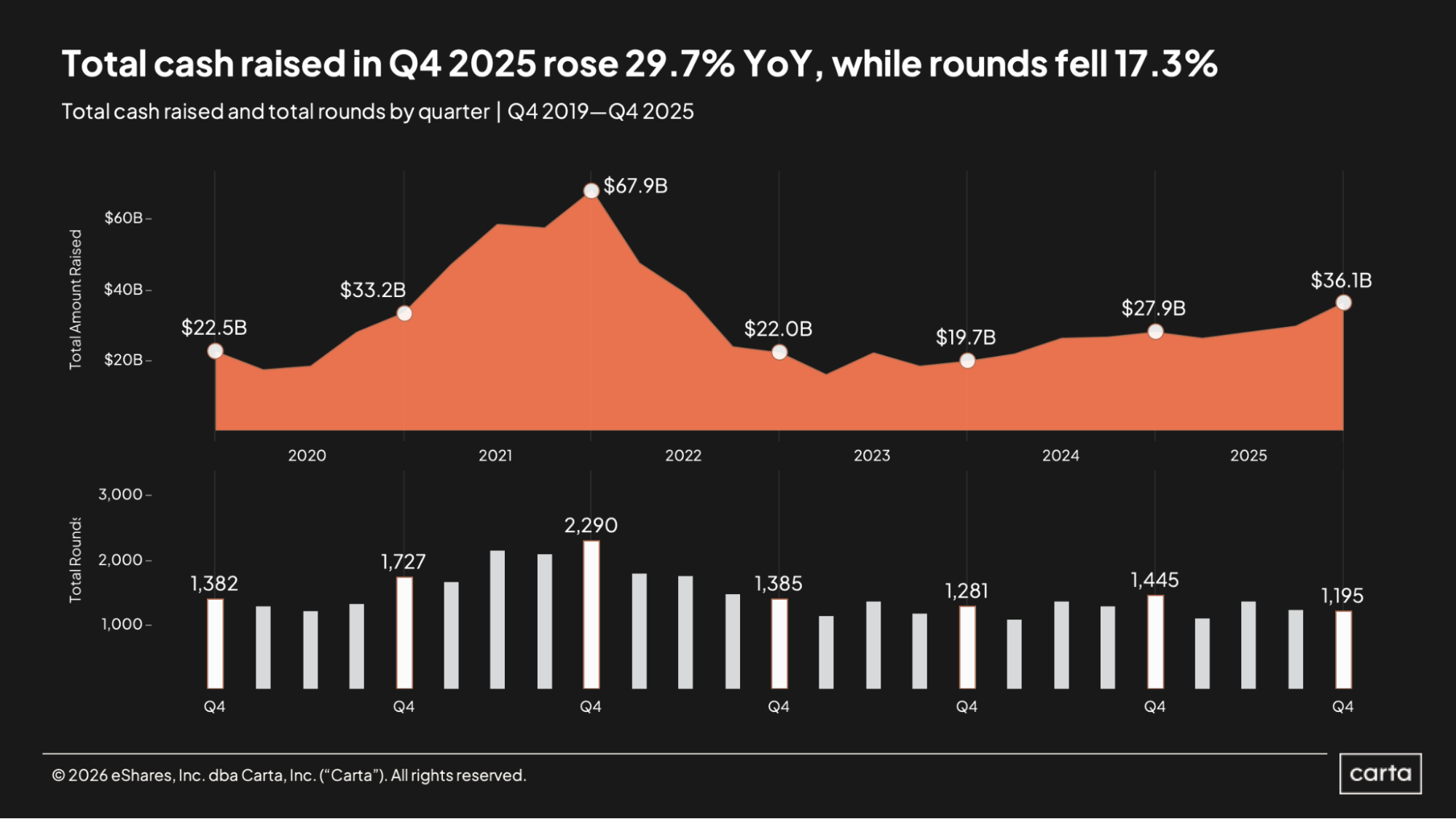

Startups on Carta combined to raise nearly $120 billion in new funding in 2025, up nearly 17% from 2024. And it ended on a particularly strong note. In Q4 alone, startups brought in $36.1 billion in new capital, the most lucrative quarter for fundraising since Q2 2022.

The hangover from the market reset that occurred in 2022 is over. Less than 14% of all new fundings in Q4 were down rounds, the lowest rate in the past three years. Startups have now either raised multiple rounds since the valuation climate began to shift, or they have achieved enough growth in the past three years to again justify a valuation increase, in many cases with the aid of new AI-powered tools and efficiencies.

The transformative effect of AI all across the startup landscape has resulted in an increasingly bifurcated market, with capital concentrating into fewer, bigger, and usually AI-dominated rounds. Total round count in 2025 fell to a six-year low. At Series D, 58% of all cash raised went to AI startups. And median valuations are up at every stage, including a staggering 667% year-over-year increase at Series E+.

One thing that’s remained the same over the past few years, however, is a challenging environment for IPOs and other forms of liquidity. As this trend continues, late-stage bridge funding is growing more common. And tender offers are on the rise. Startups on Carta combined to conduct 396 tenders during 2025—up 62% from 2024—with nearly 20% of these offerings coming from companies at Series E or later.

2025 highlights

Defining the AI premium: At every stage from Series A onward, AI startups raised larger rounds and garnered higher valuations than their non-AI counterparts in 2025. At Series A, the median AI valuation was 38% higher than the median non-AI valuation. At Series E+, the AI valuation premium reached 193%.

The Northeast strikes back: Startups based in the Northeast were responsible for 24.8% of all cash raised on Carta in the U.S. over the course of last year. During Q4, that proportion reached 33.1%, the region’s largest market share over the past three years. The West is still clearly the top region for U.S. fundraising, but the Northeast is gaining ground.

Dilution keeps dropping: Over the past year, median dilution on all rounds from seed through Series C has fallen from about 18% to 16%, continuing a years-long trend. Two years ago, median dilution across those stages stood at 19%. The biggest drop-off in 2025 came at Series B, where median dilution fell from about 15% to 12.9%.

Key trends

For the second year in a row, total capital investment on Carta increased significantly in 2025. Startups combined to raise $119.5 billion in new funding, a 16.9% increase year over year. Compared to two years ago, cash raised is up 58%.

This surge reflects an increasing concentration of capital into fewer rounds, driven in part by AI, a capital-intensive space that has absorbed a disproportionate share of recent mega-raises. Last year’s total of 4,859 new rounds was the lowest annual sum in at least the past six years, and it’s down 41% from the recent high point of deal activity in 2021.

The last quarter of 2025 was the most lucrative stretch for venture fundraising on Carta in several years, with $36.1 billion in total cash raised. That’s up 22% on a quarter-over-quarter basis and close to 30% year over year. The last time quarterly fundraising reached such a high bar was Q2 2022, at the tail end of the record-setting bull market of the early 2020s.

With just 1,195 transactions closed, capital in Q4 was spread across a relatively low number of rounds—the lowest total for any Q4 so far this decade. Across all industries and all stages of fundraising, average round size in Q4 climbed to $30.2 million, a notable increase from $19.3 million in the same period a year prior.

Full report available: Start reading now for free

Our complete State of Private Markets: 2025 in review report includes 27 additional charts and analysis on fundraising and valuation at all stages, deal terms, dilution, geographical trends, and more.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.