- Growth equity: Understanding the entire lifecycle

- What is growth equity?

- How growth equity differs from venture capital and buyouts

- The growth equity investment lifecycle

- Portfolio construction and deal sourcing

- Value creation and portfolio management

- Exit strategies

- The operational challenges of managing growth equity investments

- Complex valuation requirements

- Portfolio monitoring and LP reporting

- Managing the growth equity fund with Carta

- Frequently asked questions about growth equity

- What is the typical return on growth equity?

- Is growth equity a type of private equity?

- What is the difference between growth capital and growth equity?

What is growth equity?

Growth equity is a specific type of private equity (PE) investment strategy that provides capital to established, high-growth companies. In a growth equity deal, an investment firm provides expansion capital in exchange for a minority ownership stake in the business. This means the original founders and management team typically remain in control of the company's day-to-day operations.

Unlike other private investment strategies, the primary goal of a growth investing strategy is to help a proven company scale its operations, enter new markets, or fund a major acquisition. The investment is not intended to take control of the business or use heavy financial engineering to generate returns. Instead, the focus is on fueling the company's existing growth potential and momentum.

How growth equity differs from venture capital and buyouts

It occupies a middle ground between venture capital (VC) on one end of the spectrum and traditional leveraged buyouts (LBO) on the other. Each strategy targets companies at different stages of their lifecycle and uses capital for different purposes.

Venture capital focuses on companies led by early-stage founders that may not have revenue or a proven product yet. LBOs target late-stage, mature companies that are stable, often using a large amount of debt to finance the purchase, which significantly impacts the company's debt-to-equity ratio. Growth equity sits in between, backing established companies that are past the startup phase but are still in a high-growth period, often referred to as a growth stage.

The table below compares these three distinct investment strategies, highlighting the operational differences that are important for fund managers and their finance teams.

Aspect | Venture capital (VC) | Growth equity | Leveraged buyout (LBO) |

Investment type | Minority stake | Significant minority stake | Majority or full control |

Company stage | Early-stage, pre-revenue | Mature, revenue-generating | Established, stable cash flow |

Use of capital | Product development, finding market fit | Scaling operations, market expansion | Restructuring, operational improvements |

Use of leverage | Minimal to none | Little to no debt | Significant debt financing |

Operational focus | Tracking many small investments, high failure rate | Valuing high-growth private assets, managing complex cap tables | Managing debt covenants, driving operational efficiencies |

Reporting complexity | Simpler, focused on startup milestones | High, requires frequent re-valuation and performance tracking | High, focused on debt service and covenant compliance |

The growth equity investment lifecycle

From the perspective of PE firms focused on growth, the investment process follows a clear lifecycle with key stages, from making an investment to realizing a return. Each stage presents distinct responsibilities for the fund's managers.

Portfolio construction and deal sourcing

The lifecycle begins when growth equity investors identify suitable companies for investment. This stage is defined by a search for specific characteristics that set growth equity targets apart from other types of private companies and inform investment decisions. Firms source these deals through their professional networks, industry research, and by proactively reaching out to companies that fit their investment thesis, often highlighting their own successful track record to build credibility before beginning due diligence.

Growth equity investors typically look for a target company with the following attributes:

A proven business model with demonstrated product-market fit

A history of strong and consistent revenue growth rates

A business that is either profitable or has a clear path to profitability

A strong, often founder-led management team that remains in place after the investment

Value creation and portfolio management

Value creation in growth equity is a collaborative effort, not a controlling one, reflecting a broader industry shift away from financial engineering and minimizing market risk toward sustained operational transformation. The firm works alongside the company’s existing management team to help accelerate growth by providing resources and expertise.

As Shiv Narain, founder of the “How to SaaS” podcast, explains during Carta’s Value Creation through Employee Equity webinar: "Whatever value creation plan you build, the critical point of failure is if you have the right people... if you don't have the right leader for revenue or sales or marketing or product, your plans are going to fail."

Investors add value in several key ways:

Strategic guidance: The firm provides expertise and access to its network to help the portfolio company with strategic planning, market expansion, and preparing for an eventual exit. This could involve helping to refine pricing models or developing a strategy for entering international markets or specialized sectors like healthcare.

Operational support: This involves helping the company recruit key executives, refine its sales and marketing strategies, or identify potential bolt-on acquisitions to accelerate growth.

Exit strategies

The final stage of the lifecycle is the exit, where the growth equity investor seeks to realize a return on their investment in a market where the expected exit value of $413.2 billion in 2024 significantly outpaced the totals from 2022 and 2023.

There are three primary exit paths for a growth equity investment:

Initial public offering (IPO): The portfolio company becomes a publicly traded entity, allowing the firm to sell its shares on the open market.

Strategic acquisition: The company is sold to a larger corporation in the same industry, often facilitated by investment banking partners, which provides a clean exit for the investment firm.

Secondary sale: The firm’s stake is sold to another firm or institutional investor, sometimes as part of a co-investment opportunity, providing liquidity without a full company sale or IPO.

While IPOs often get the most attention, data on startup M&A activity shows that acquisitions are a far more common outcome. For example, 151 startups on Carta were acquired in the first quarter of 2024 alone, while U.S. stock markets were on pace for about 150 IPOs for the entire year.

The operational challenges of managing growth equity investments

While the growth equity investment strategy is focused on growth, the back-office operations present unique and complex challenges, from fundraising to final distribution. For a fund's CFO and finance team, managing a portfolio of growth equity investments requires specialized tools and expertise that are often overlooked by those outside the industry. These operational hurdles can impact everything from compliance to investor relations.

Complex valuation requirements

Valuing a minority stake in a private, high-growth company is notoriously difficult. Unlike public stocks, there is no daily market price to reference, yet auditors and limited partners (LP) require regular, defensible valuations to determine the fair value of assets. This isn't a simple task; it requires a deep understanding of the company's performance, market trends, and complex valuation methodologies.

This process demands specialized expertise and technology, and many firms rely on dedicated PE software to manage these complexities.

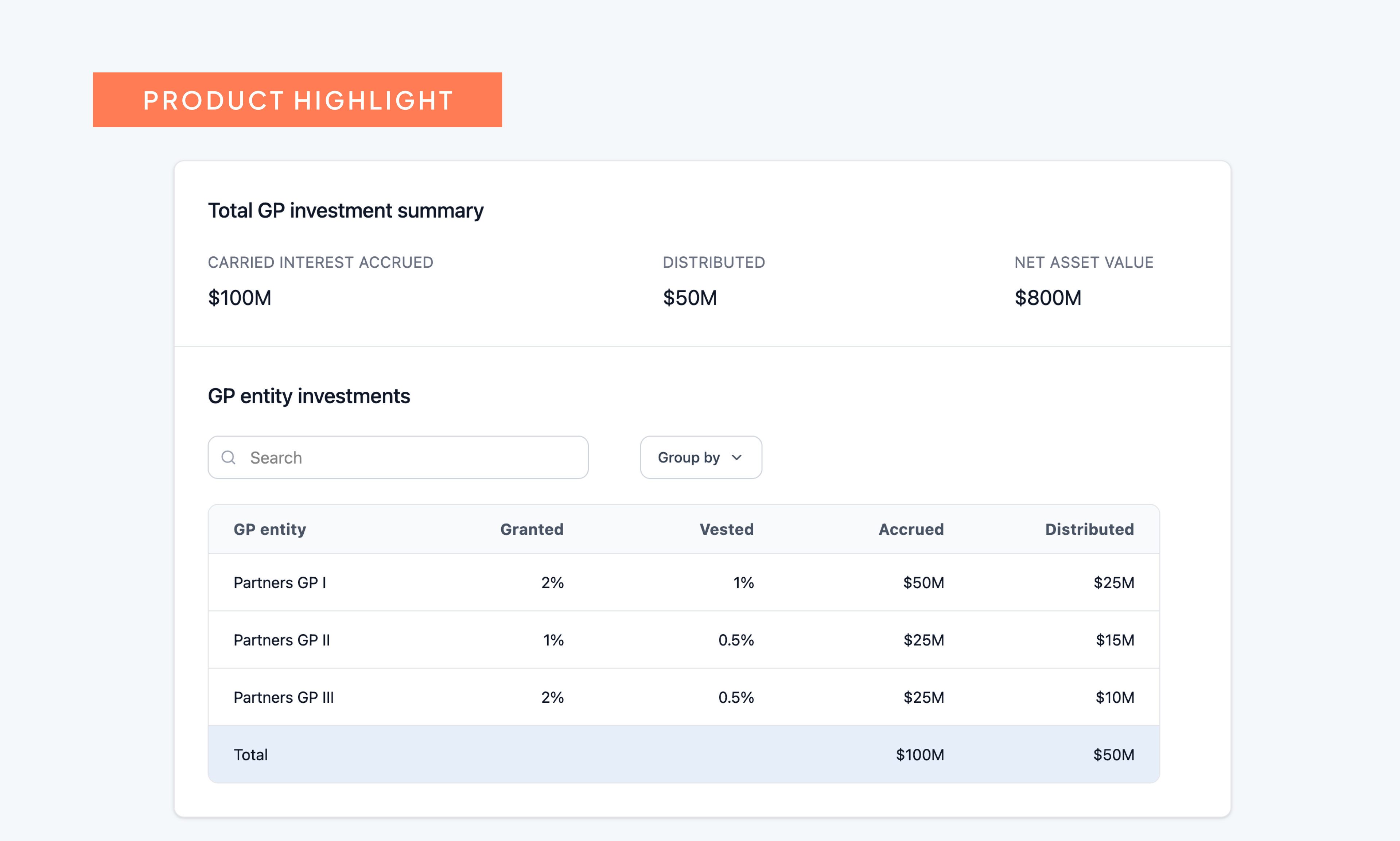

Portfolio monitoring and LP reporting

LPs who invest in growth equity funds have high expectations and often use benchmarks like the public market equivalent (PME) to gauge performance. They require frequent and detailed updates on how each portfolio company is performing, a demand codified by new regulations that mandate detailed quarterly reporting on fund performance, fees, and expenses.

Fund administrators are often stuck manually chasing down financial data from multiple portfolio companies via email and Excel spreadsheets. For venture funds, managing communications and reporting for dozens—or even more than a hundred—different LP relationships is a significant operational lift. The median LP count for a fund larger than $250 million is 104; without a technology solution, this manual reporting process is not only inefficient and time-consuming but also prone to errors. A single mistake in a spreadsheet can lead to inaccurate reports and difficult conversations with LPs about key metrics like distributions to paid-in (DPI).

A centralized platform like the Carta LP Portal provides LPs with secure, on-demand access to performance dashboards, financial statements, and all other fund documents. This transparency builds trust and dramatically reduces the administrative burden on the fund's finance team, freeing them up to focus on more strategic work.

Managing the growth equity fund with Carta

A modern growth equity strategy cannot be run effectively on outdated, disconnected systems. The operational complexity demands an integrated technology solution that provides complete visibility and control over the entire fund lifecycle. A fragmented approach using spreadsheets and multiple point solution providers creates inefficiencies and risks that can hold a firm back.

Carta Fund Administration serves as the purpose-built operational backbone for growth equity firms. By connecting fund accounting, portfolio valuations, portfolio company cap table data, and LP reporting on a single platform, Carta gives fund CFOs the real-time visibility they need. This allows them to move from back-office administration to a strategic role, surfacing insights and driving fund performance to exceed thresholds like the hurdle rate.

Request a demo today to see how.

Frequently asked questions about growth equity

What is the typical return on growth equity?

While the return on growth equity is often described qualitatively as targeting strong, consistent returns, a look at performance data for private funds can provide a more quantitative answer. For example, among U.S. VC funds from the 2017 vintage, the median net internal rate of return (IRR) was 13.5% as of Q2 2025, according to a recent performance report.

However, this return sits in the middle of a wide range of outcomes: Top-quartile funds from that same vintage reached an IRR of 18.7%, while the top 10% of funds achieved 28.3%, illustrating the significant variation in VC fund performance.

Is growth equity a type of private equity?

Yes, growth equity is a specific strategy within the broader PE asset class.

What is the difference between growth capital and growth equity?

Growth capital is money invested in a company to help it expand (often for new products, markets, or acquisitions). Growth equity is a specific type of PE investment that provides growth capital, typically to mature, profitable companies that need funding for expansion without giving up control.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.