Topline

2025 Carta Policy year in review

Senate Banking set to markup crypto market structure legislation

SEC releases report on capital raising trends

Quick hits

New year, new Carta Policy Weekly…well, at least a new distro day. We hope everyone enjoyed the holidays and that your new year is off to a strong start. 2026 is already shaping up to be an eventful year on the policy front, but before we dive in, we want to reflect on some major achievements in 2025.

2025 Carta Policy year in review

Policy is infrastructure: It can bind growth and innovation or unleash it. We built the Carta Policy team to serve as the connective tissue between the innovation ecosystem and policymakers. We aim to shape the policy infrastructure to bolster private capital and broaden its positive impacts to more—more entrepreneurs, more investors, and more communities. We also help educate and provide insights to the ecosystem to help them navigate the evolving policy landscape.

We have much to be proud of over this past year.

At the beginning of 2025, we faced a policy environment where key tax provisions were at risk, macro conditions created volatility and uncertainty across the board, and capital formation was at risk of becoming a backburner issue. Through engagement and advocacy, we secured big wins for the ecosystem on the tax and capital markets fronts. We also developed content and convened events for the ecosystem around the shifting policy landscape, covering topics from tariffs to artificial intelligence. We sought not only to shape the policy infrastructure but also help you navigate it.

2025 highlights

Tax reform wins for the innovation economy. As major provisions of the 2017 tax cuts were set to expire at the end of 2025, policymakers not only had to figure out how to extend these provisions, but also how to offset the $4.5T price tag. As part of that discussion, key provisions that benefit the innovation economy came under fire. So we acted; we went on offense. We built a strategy and coalition—the Innovator Alliance—to not only defend our key priorities, but also expand them. The results:

QSBS: Protected and expanded, enabling more businesses to qualify and more shareholders to benefit on a shorter time frame

Carried interest: Preserved to bolster fund economics for private capital fund managers

R&D: Restored full and immediate expensing, including on a retroactive basis for small businesses

Because of our efforts, we were able to secure these impactful wins for the innovation ecosystem, and engagement made the difference.

Capital formation legislation with bipartisan momentum. The House passed the INVEST Act, which will expand access to capital for founders and emerging managers and increase private market investment opportunities for more investors, including by:

Expanding qualifying VC investments to include secondaries and investments in other VC funds

Expanding the size and investor caps for qualifying venture capital funds

Modernizing the accredited investor standard by adding on-ramps though education and exams

But unlike recent capital formation packages, this effort has strong bipartisan support, which means there is a real shot at advancing these policies and getting them signed into law. Carta has been working over the past year to educate, shape the contours, and engage the broader innovation community to build consensus. In advance of the floor consideration, Carta led a coalition of 27 organizations from across the country and across the ecosystem in support of this important legislation. To be clear, we do not get this result without this engagement, but we need to amplify it to push these important policies over the finish line in the Senate, which will be a major focus in 2026.

SEC agenda focused on capital formation. A change in administration meant a shift in SEC posture, and Carta started engaging the agency early on to ensure innovation ecosystem priorities remain top of mind. To that end, the SEC has included many of our priorities in their rulemaking agenda and has already taken action to reduce barriers to raise private capital and expand investor access to private markets. More to come as the agenda kicks into full swing this year.

Building the connective tissue through ecosystem engagement. To serve as the connective tissue, we need to engage the ecosystem. And we stepped up our game this year. Carta Policy hosted dinners and participated in events across the country, including SuperReturn, RAISE Global, and DC Fintech Week. In addition to the Innovator Alliance, we broadened our advocacy efforts to include regional organizations to help our message resonate with policymakers on a local level.

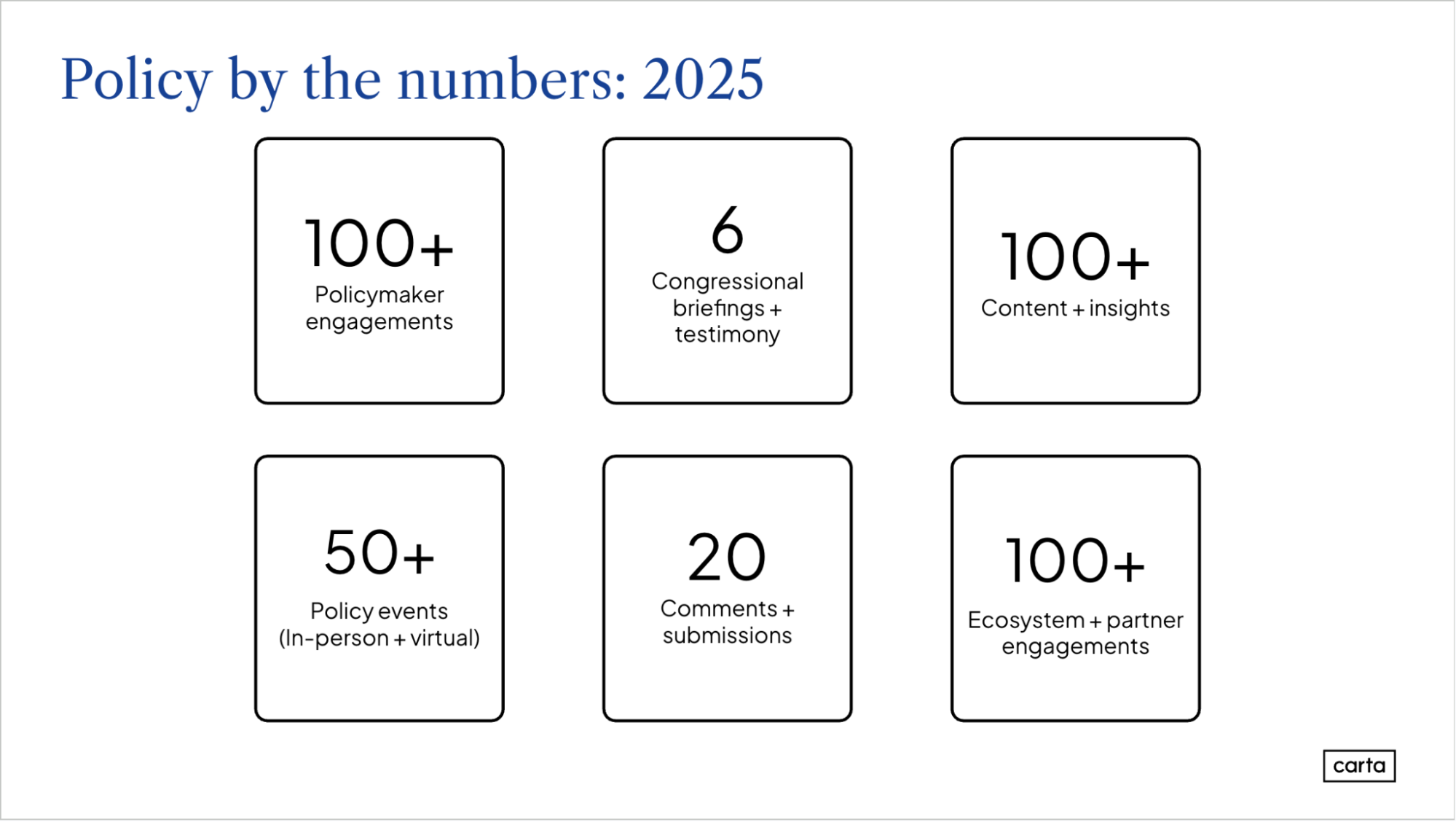

Education and advocacy. To make the case for policy changes like expanding VC fund parameters and QSBS, Carta Policy participated in over 100 policy meetings, hosted a series of Hill briefings for policymakers (VC 101), and our very own Anthony Cimino testified before Congress on the importance of the SBIC program and expanding access to capital.

We are proud of the work, but we could not do this alone. It took the entire ecosystem—the Innovator Alliance, fund managers, and entrepreneurs we’ve learned from at events and through social engagement, feedback from our customers, our law firm partners, and many more stakeholders.

Thank you for an incredible year.

Looking ahead, 2026 will be a pivotal year for private market policy. Congress will look to finalize a digital asset regulatory framework and pass a capital formation package (INVEST Act); the SEC’s rulemaking agenda will be in full swing, including expanding retail access to private assets; and everyone will continue to grapple with how to regulate AI. Needless to say, it will be a busy year.

Stay tuned to Policy Weekly to keep up to date on the latest private capital policy developments, follow us on LinkedIn, and don’t hesitate to reach out to policy@carta.com if you have questions or want to engage on these efforts.

Senate Banking set to markup crypto market structure legislation

After postponing action late last year, the Senate Banking Committee is expected to mark up its crypto market structure bill this week. Bipartisan negotiations have continued with industry input, and an updated draft is circulating with revisions aimed to attract broader bipartisan support. However, several policy disputes remain unresolved, with the biggest issues centered around these areas:

Stablecoin-linked rewards: The most significant outstanding issue is whether crypto platforms should be permitted to offer rewards or yield tied to stablecoin holdings. Banking groups argue these products function as deposit substitutes, while crypto advocates characterize them as consumer incentives rather than interest-bearing deposits. The issue of stablecoin “yield-as-rewards” emerged late in negotiations and has been a central sticking point, and policymakers are split over potential compromises, which could require reopening provisions tied to the already-passed GENIUS Act. The latest draft contains language that would bar crypto firms from paying interest or yield solely for holding a stablecoin, but would permit certain activity-based rewards.

Ethics: Democrats continue pushing for additional language restricting public officials and their families from endorsing, issuing, or profiting from digital assets while in office. The latest version does not include these restrictions, and while discussions are ongoing, their omission could present a hurdle to securing bipartisan support.

DeFi: A central challenge is determining which decentralized finance activities—such as token creation, issuance, or distribution—should be subject to federal regulatory standards, while avoiding rules that could be viewed as effectively prohibiting decentralized or non-custodial protocols.

Looking ahead: Additional amendments and revised drafts are expected ahead up to the markup as negotiations continue to reach bipartisan consensus. The Senate Agriculture Committee also initially planned to mark up its portion this week, but has delayed consideration to late January. Even if the legislation advances out of both committees, the framework will face significant hurdles, competing priorities, and a narrowing window to cross the finish line and become law before the midterm elections.

SEC releases report on capital-raising trends

The SEC’s Office of the Advocate for Small Business Capital Formation issued its FY 2025 staff report on capital-raising dynamics. Here are a few key takeaways and why they matter:

Private markets continue to dominate conversation, but concentration is rising. In VC, nearly 40% of dollars went to just 10 companies, and mega deals now represent over 50% of total deal value despite being a small share of deal count. Capital is flowing, but not broadly, raising concerns about access for first-time founders and emerging managers.

Early-stage fundraising is harder, slower, and more expensive. Seed rounds are larger, but harder to secure. The median time from seed to Series A has risen over 80% since 2021, and pre-seed and seed now represent less than 30% of VC deal count. Friction at the beginning of the pipeline is increasing, which could threaten startup formation and long-term innovation.

Emerging fund managers face mounting pressure. VC fundraising has slowed sharply. In 2024, 30 VC firms raised 75% of all VC capital, and for the first time in a decade, emerging managers closed fewer funds than established firms. Capital consolidation could narrow founder choice and reduce regional and sectoral diversity.

Liquidity is shifting from IPOs to secondaries. Companies are staying private longer, with the number remaining private more than 8 years after the first round quadrupling since 2014. The U.S. private secondary market reached $61B, accounting for more than 30% of VC exits. Secondaries are now the core market infrastructure for liquidity.

Why it matters: The private capital ecosystem remains robust at scale, but is increasingly difficult to access for early-stage companies, new managers, and founders outside traditional networks. The SEC report reinforces the case for targeted reforms to bolster and broaden the ecosystem, and that is exactly what we are pushing for in the INVEST Act.

Shoutout to the Carta Insights team for being featured in the report. Be sure to check out our Data Desk and sign up for the Data Minute newsletter for more private capital insights.

Quick hits

U.S. prosecutors launch criminal investigation into Federal Reserve’s Jay Powell. On Sunday evening, the Federal Reserve Chair revealed the Justice Department served the Fed with grand jury subpoenas and threatened him with a criminal indictment over testimony related to Fed headquarters renovation, which has been characterized by Powell and others as politically motivated threats to influence monetary policy and lower rates. But this is more than a political spat; it touches the foundational principle of U.S. monetary policy independence.

Trump targets institutional housing investment. President Donald Trump has threatened to ban or significantly restrict Wall Street investment in single-family homes, directing his administration to pursue an executive order that would limit additional purchases by large institutional investors, including private equity and real estate funds. The move, which is more closely aligned with progressive critiques of institutional ownership, is framed as part of a broader effort to improve housing affordability and expand homeownership. While the legal mechanics and enforceability of the proposal remain unclear, the signal is significant. Targeting a specific asset class and investor group marks a notable shift toward sector-specific economic intervention, and could set a precedent for greater political scrutiny of private capital in markets tied to household affordability.

Sign up below to receive Carta's Policy Weekly Brief

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.