Some venture capital funds manage just a few million dollars. Some manage a few hundred million. No matter the size, the goal of VC funds is typically the same: To invest in promising young companies that will eventually allow the fund to return a healthy profit.

Across the spectrum of fund sizes, however, some of the behind-the-scenes operational details can differ significantly.

Several of the ways in which differently sized funds can vary are related to fund economics, including things like capital calls, fee models, fund expenses, and carried interest. These financial structures of funds are a key consideration for fund managers—and for their LPs—who are looking to raise and put capital to work in the VC space.

Carta’s newly released 2025 Fund Economics Report presents a comprehensive breakdown of the market norms for fund structures across a wide range of closely watched variables. Here are five highlights from the report that demonstrate some of the key differences between the smallest VC funds and the largest.

1. Skin in the game

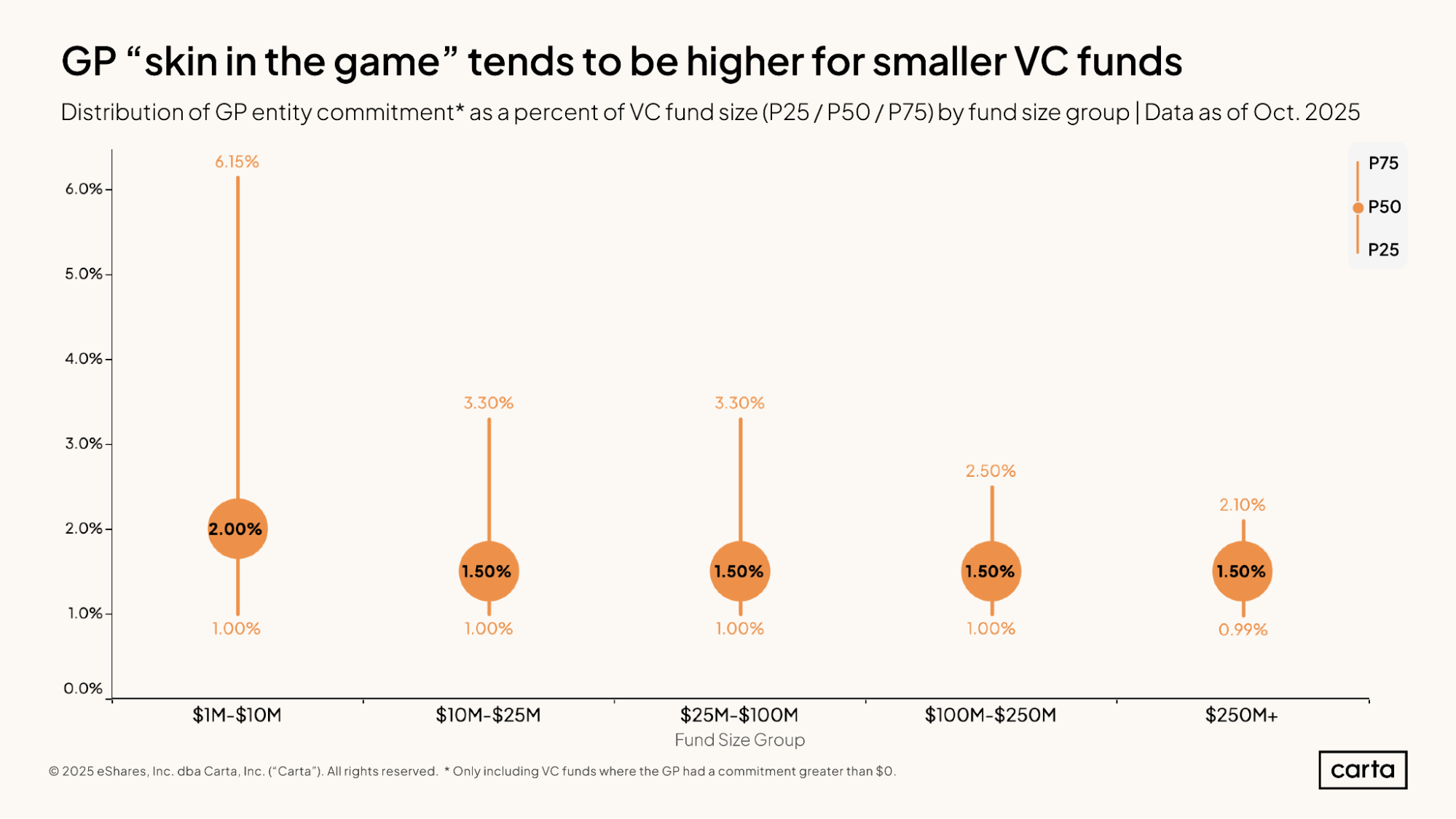

While fund managers—or GPs—generally raise most of their capital from outside LPs, they also generally contribute some of their own capital as well, which is referred to as “skin in the game.”

The managers of very small venture funds typically have more skin in the game than the managers of the largest vehicles. Among funds with between $1 million and $10 million in capital commitments, the median GP entity commitment is equivalent to 2% of the total fund size. For funds larger than $10 million, the median GP entity commitment is a little bit smaller, at 1.5% of fund size.

At the 75th percentile, skin in the game can differ to a greater degree. A top quartile fund between $1 million and $10 million sees a GP commitment equivalent to 6.15% of fund size. At the top quartile of funds between $100 million and $250 million, meanwhile, the GP entity commitment is 2.5% of fund size. For funds larger than $250 million, a top quartile GP entity commitment totals just 2.1% of overall committed capital.

Of course, in absolute terms, managers of larger funds usually contribute a larger sum of capital than the managers of smaller funds—6.15% of $10 million is a lot smaller than 2.1% of $250 million. But for managers of smaller funds, there’s a much wider range of commonly seen structures.

2. Capital calls

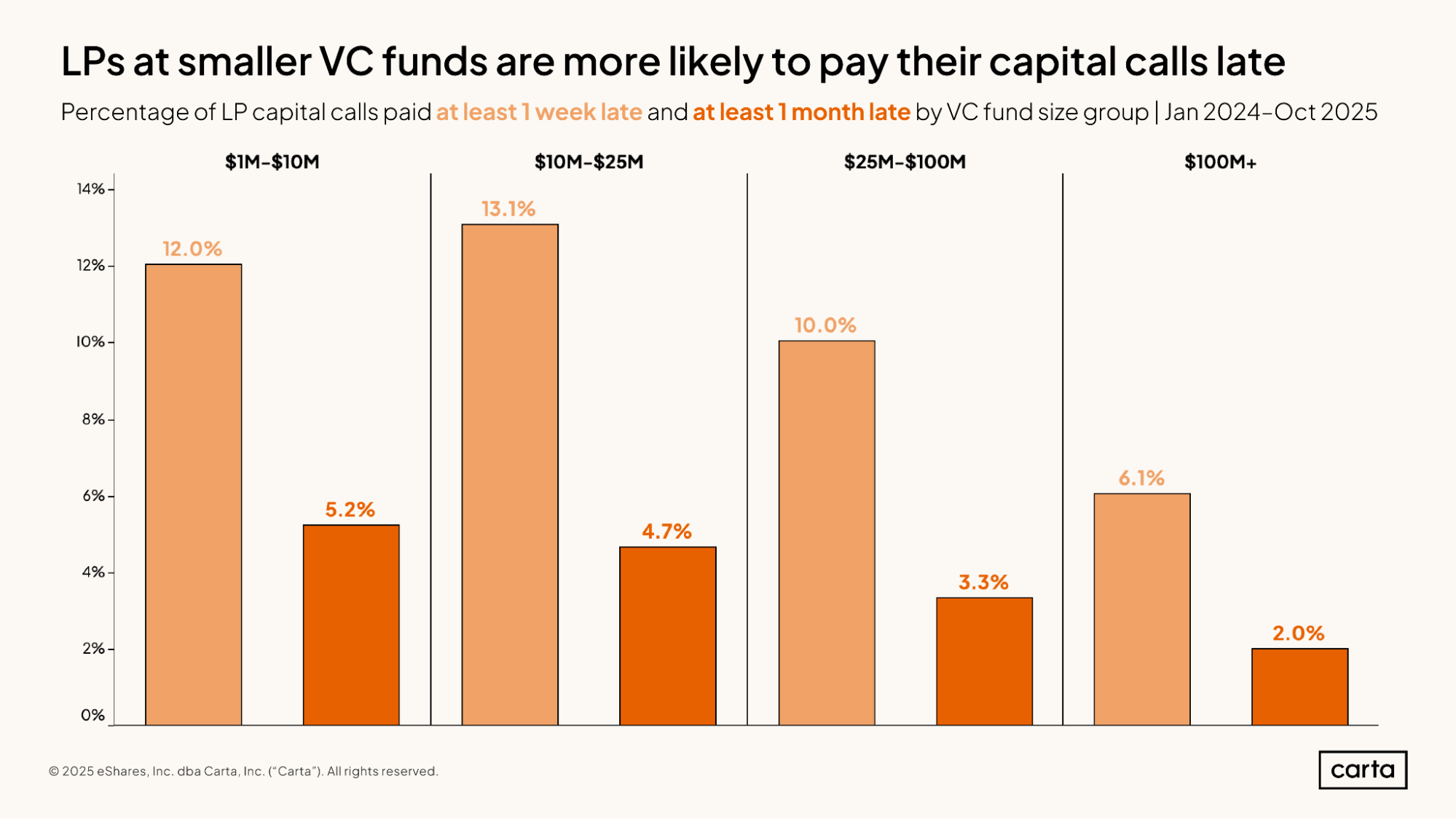

When fund managers issue a capital call to their LPs, it typically comes with a deadline for when the desired capital is due. The vast majority of capital calls across all fund sizes are paid on time. As a rule of thumb, though, the LPs in smaller venture funds are a little more likely to be late in meeting capital calls than the LPs of larger funds.

Among funds in the $1 million to $10 million interval, about 12% of capital calls are paid at least one week late and 5.2% are paid at least one month late. For LPs in the largest funds—those with more than $100 million in commitments—late payment is roughly half as likely. Within this interval, 6.1% of capital calls come in at least one week late, and 2% are paid at least a month after the initial deadline.

3. Carried interest

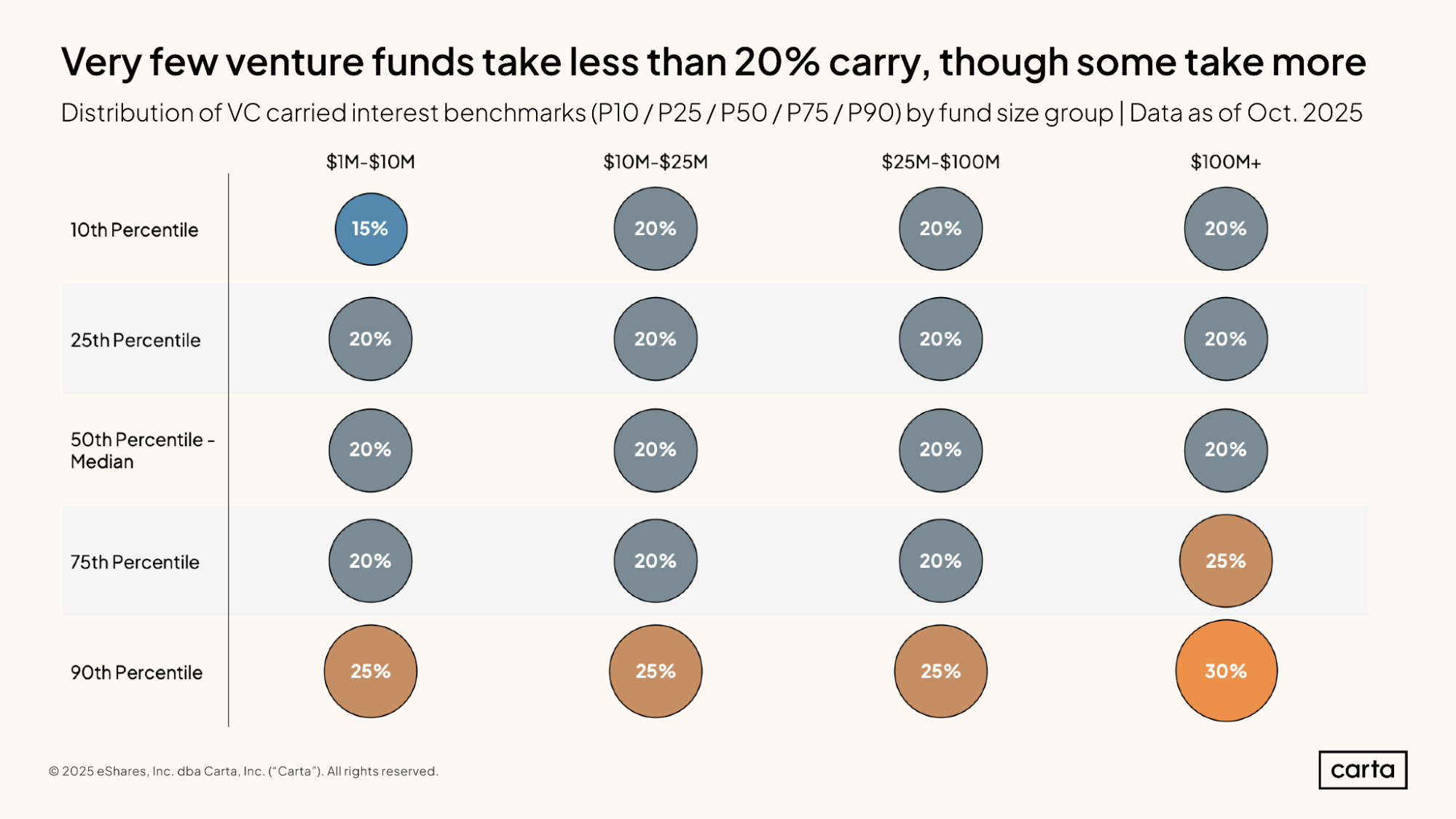

Across venture funds of all sizes, the classic 2-and-20 fee structure remains the industry norm. The median GP takes 2% of total fund size as a management fee and 20% of any fund profits as carried interest, also called carry, which is usually the primary generator of real wealth for fund managers.

Look beyond the median to other statistical benchmarks, however, and some variation emerges in carried interest rates between small and large funds. For VC vehicles between $1 million and $10 million, the bottom decile of carry rate lands at 15%, and the top decile is 25%. For funds with more than $100 million in commitments, the 75th percentile for carry rate is 25%, and the top decile climbs to 30%.

In general, $100 million-plus funds tend to be run by larger, more established managers than smaller funds. Their larger carry rate suggests that the managers of top-tier large funds have the leverage with their LPs to command a larger share of the fund’s profits. The lower carry at the bottom decile for the smallest funds, meanwhile, signals that some of these managers may be willing to reduce their carried interest rate as a way to attract LP interest.

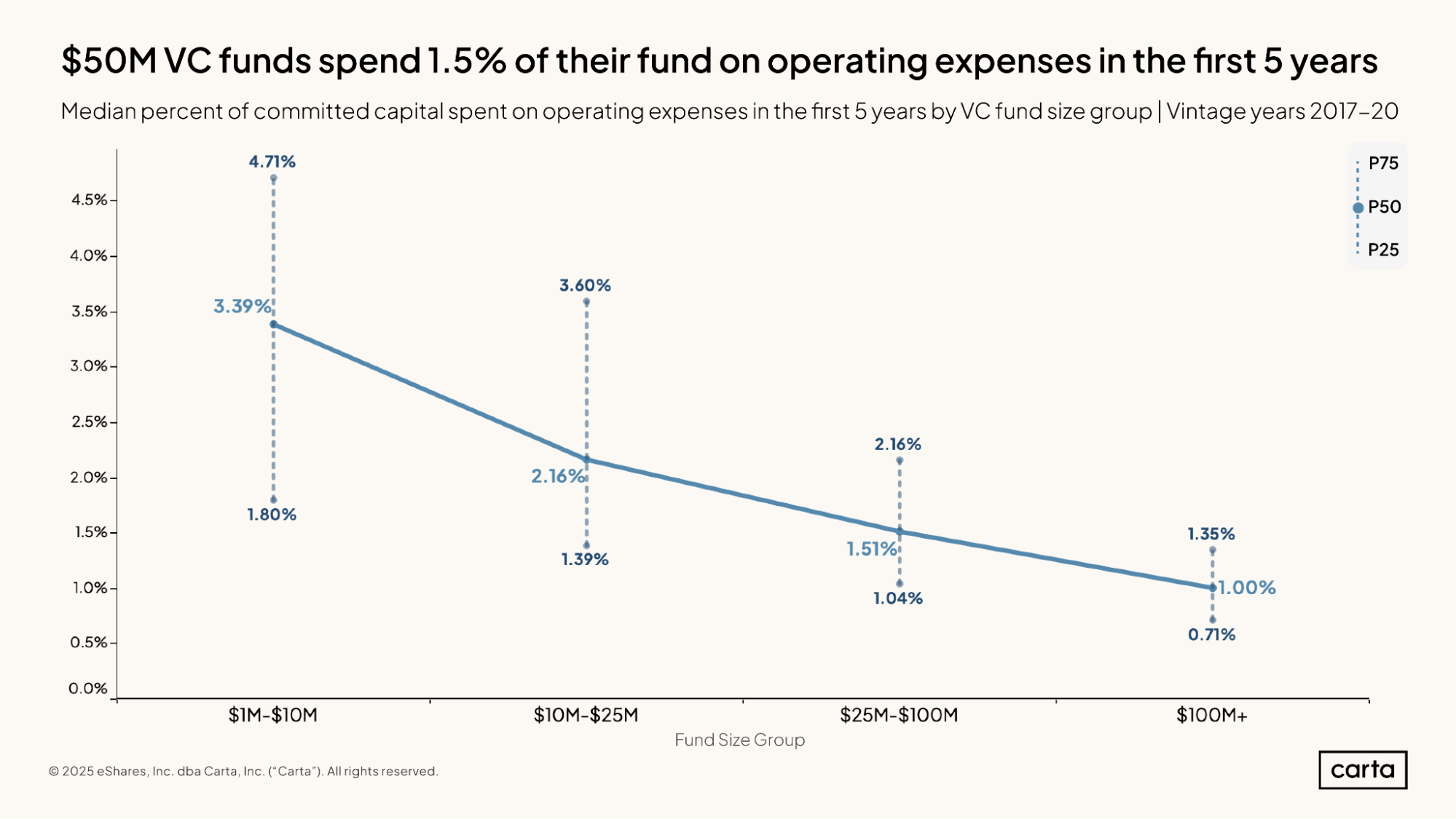

4. Operating expenses

The typical venture fund has an investment period of five years during which it will deploy the majority of its capital. During this five-year stretch, the median fund between $1 million and $10 million spends about 3.4% of its total fund size on various operating expenses. For the median fund larger than $100 million, just 1% of total fund size goes toward operating expenses.

As is the case with skin in the game, the percentage of fund capital that goes toward operating expenses varies more widely among smaller funds than larger funds. For $1 million to $10 million funds, the difference between the 25th percentile and the 75th percentile is nearly three percentage points; for $100 million-plus funds, that same gap is less than one percentage point.

This analysis considers only operating expenses that are attributable to the fund itself and are paid out of the fund’s available capital. In many cases, the management company—a separate legal entity set up by an investment firm that operates the firm’s business across multiple discrete funds—makes these initial expense payments and is then reimbursed by the fund. The management company is also responsible for several other critical fund expenses, such as salaries and rent payments for office space. Properly managing this interplay between the management company, the GP entity, and the specific fund is a key aspect of fund operations.

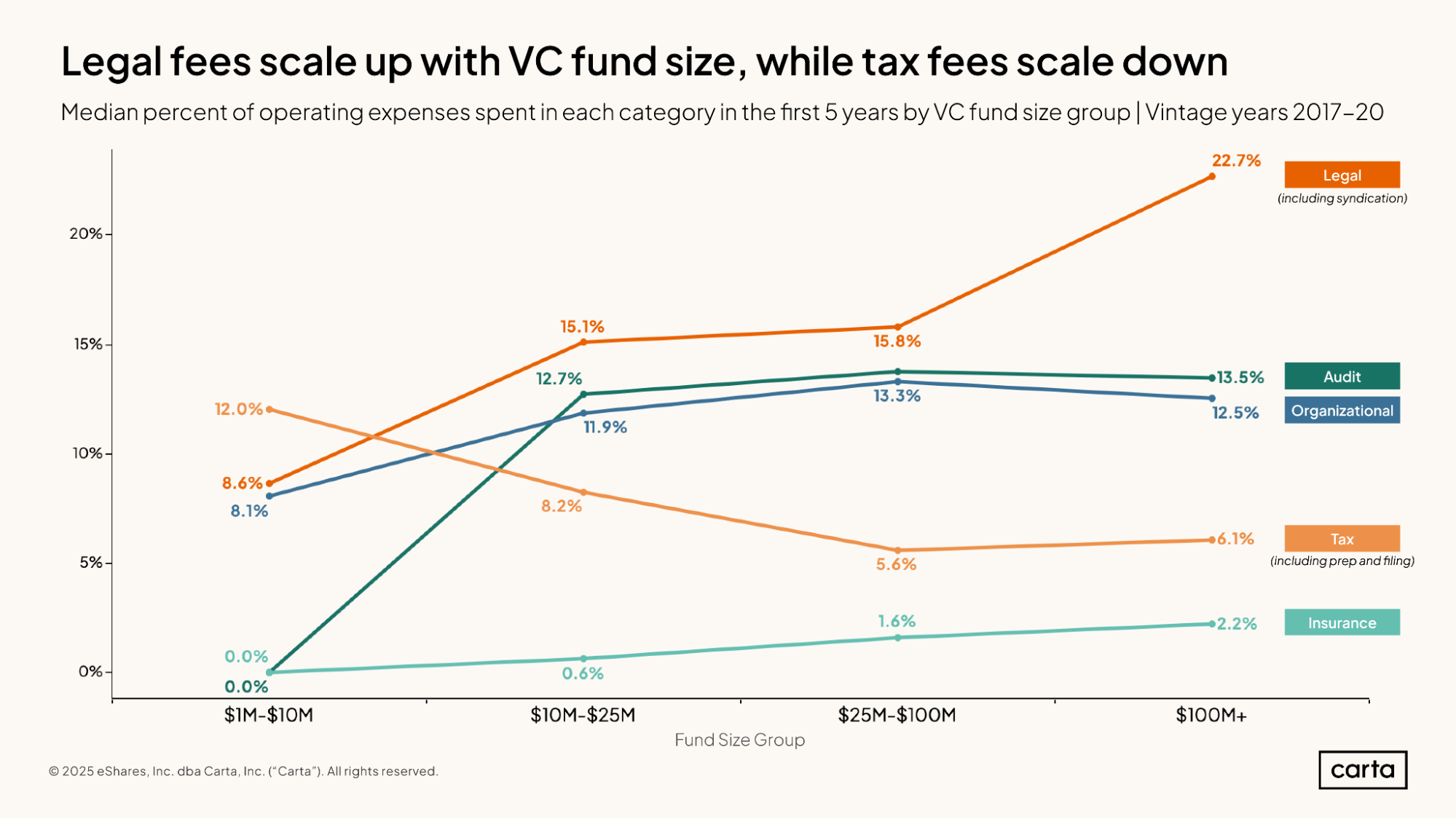

5. Legal fees and tax fees

For the median fund between $1 million and $10 million, some 8.6% of total operating expenses paid over a fund’s first five years go toward legal fees. As fund size increases, the percentage of expenses that go toward legal fees also climbs, reflecting the increased complexity—and, in some cases, the larger portfolios—of larger funds. For the median fund with more than $100 million in commitments, legal fees account for 22.7% of all operating expenses.

Conversely, the percentage of operating expenses that goes toward tax fees tends to decline as fund size grows. For the smallest funds, tax fees account for a median of 12% of operating expenses, higher than the percentage of expenses that goes to legal fees. For funds larger than $100 million, tax fees comprise just 6.1% of expenses, more than three times smaller than the share for legal fees.

These differences highlight one of the key factors in general for comparing fund economics across funds of different sizes: scalability. Compared to legal fees, the tax fees paid by VC funds are typically less scalable and more of a fixed cost.

Subscribe to the Data Minute newsletter

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.