- Dry powder in private equity and venture capital

- What is dry powder?

- Committed vs. called capital: The dry powder equation

- Why dry powder is a key metric for GPs and LPs

- Managing dry powder through the fund lifecycle

- Stage 1: Creating dry powder through fundraising and commitments

- Stage 2: Deploying dry powder during the investment period

- Stage 3: Managing reserves for follow-on investments and expenses

- The risks of idle dry powder: Capital drag and performance pressure

- How uncalled capital impacts IRR and fund performance

- How deployment history impacts future fundraising

- From manual tracking to strategic forecasting

- Frequently asked questions about dry powder

- What is the difference between dry powder and cash reserves?

- What happens if dry powder is not deployed by the end of the investment period?

- How do capital recycling provisions in an LPA affect dry powder?

What is dry powder?

In private equity (PE) and venture capital (VC), dry powder is the amount of capital that investors have committed to a fund but which has not yet been invested. It represents the deployable capital a fund has on hand to manage deal flow and make new investments, cover fund expenses, or provide follow-on funding to existing portfolio companies (portco). This pool of capital is a critical resource for fund managers, giving them the firepower to act on investment opportunities as they arise.

It is a common misconception that dry powder refers to a pile of cash on hand sitting idle in a fund's bank account. Instead, it is a binding promise from the fund's investors, known as limited partners (LP), to provide capital when the fund manager finds a suitable investment.

This distinction is important, as it highlights the dynamic relationship between a fund's commitments and its deployment strategy. Understanding this concept is the first step to understanding how private funds operate.

Committed vs. called capital: The dry powder equation

To understand dry powder, it helps to think of it as the result of a simple equation:

Total LP Commitments - Cumulative Capital Called

This formula breaks down the two core components that determine a fund's available capital at any given moment. Thinking about it this way simplifies a complex process into two main ideas.

Total LP commitments: This is the total amount of capital an LP agrees to provide to a fund over its lifetime. This agreement is legally binding and is finalized during the fundraising process through a document called the limited partnership agreement (LPA) and often accompanied by the private placement memorandum (PPM).

Cumulative capital called: This represents the total amount of money the general partner (GP) has requested from LPs to date. These requests, known as capital calls, are used to deploy capital into portcos, pay management fees, and cover other fund expenses.

When you subtract the money you've already called from the total money that was promised, the remainder is your amount of dry powder.

Why dry powder is a key metric for GPs and LPs

Dry powder is an indicator of a fund's health, strategy, and potential. Because it represents the balance between promised capital and invested capital, both GPs and LPs monitor dry powder levels closely throughout the fund's lifecycle.

For a GP, dry powder represents their investment capacity and ability to conduct due diligence on new deals. It provides the strategic flexibility to pursue attractive investment opportunities without needing to raise a new fund for every single deal. A healthy amount of dry powder means you are ready to act when the right company or deal comes along, even during periods of economic uncertainty and market volatility.

For an LP, the amount of dry powder signals the fund's remaining investment potential. They also watch it to ensure their committed capital is being put to work effectively and not sitting on the sidelines for too long. LPs want to see that their commitment is leading to action.

This need for visibility is a common pain point for LPs, especially as recent market conditions have delayed capital returns. For example, after five years of investing, more than three out of every five VC funds on Carta that closed in 2019 had not yet distributed any capital back to their LPs. As a result, LPs who often invest in multiple funds require investor updates that provide a clear, consolidated view of their commitments and performance. A dedicated solution like the Carta LP Portal addresses this by providing a single, secure login for LPs to access all their fund information, from capital calls to performance metrics, fostering transparency and trust.

When LPs have a clear view, they have more confidence in the fund's management. This transparency is key to building strong, lasting relationships.

Managing dry powder through the fund lifecycle

A fund's dry powder is not a static figure. It is a dynamic resource that ebbs and flows throughout the fund's multi-year journey, from its initial creation to its final investment.

Understanding how to manage this resource at each stage is a core responsibility of any fund manager. It requires careful planning and strategic investment strategies.

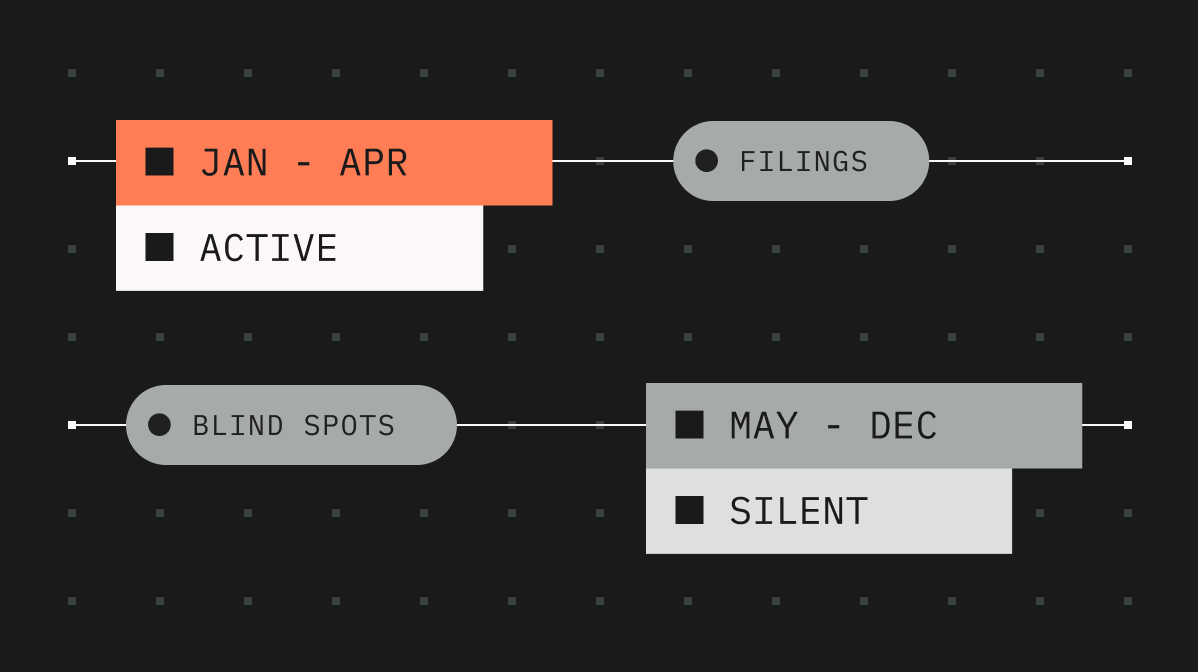

Stage 1: Creating dry powder through fundraising and commitments

Dry powder originates the moment a fund closes on its fundraising round. At this point, the commitments from LPs are legally secured through the LPA, and the fund's initial dry powder balance is officially established. This marks the beginning of the fund's investment period, the window of time during which the GP can make new investments.

Managing this closing process can be a significant operational burden for GPs, who often juggle disconnected spreadsheets, legal documents, and email chains to track investor commitments. This manual work is not only time-consuming but also prone to errors that can damage investor confidence from the start.

A professional and efficient onboarding experience, managed through a platform like Carta Closings, not only makes a strong first impression on investors but also creates a single source of truth for all capital commitments from day one. This sets a foundation of accuracy and trust.

Stage 2: Deploying dry powder during the investment period

Once the fund is established, the GP begins to put the dry powder to use. When the GP identifies an investment opportunity and is ready to deploy capital, they issue a capital call notice to their LPs, requesting a portion of their total commitment. This action reduces the fund's dry powder balance. Each capital call is a transaction that draws down the available pool of committed capital.

Moving money from LPs to portcos quickly and accurately is a critical operational function. Delays or errors in this process can jeopardize deals and harm relationships with both founders and investors.

Centralized platforms like Carta Fund Management that offer streamlined capital call workflows and banking integrations help accelerate this capital deployment process. This ensures that when a deal is ready, the funding is too.

Stage 3: Managing reserves for follow-on investments and expenses

Experienced GPs rarely deploy all of their dry powder on initial investments. Instead, they strategically hold back a portion of their capital as cash reserves for future use. For example, VC funds raised prior to 2021 have invested roughly 90% of their available capital, leaving about 10% as dry powder for follow-on investments and other strategic needs.

This foresight is essential for maximizing the fund's success over the long term. It's a sign of a disciplined and strategic fund manager. Properly managing these reserves ensures the fund has the resources it needs to support its best companies and maintain its operations.

These reserves serve two primary purposes:

To make co-investment opportunities or follow-on investments in the fund's most promising portcos, providing them with additional capital to fuel their growth and increase the fund's ownership stake.

To cover future fund expenses, management fees, and other required compliance items like annual reviews and audited financials over the fund's lifespan, which can often last a decade or more.

The risks of idle dry powder: Capital drag and performance pressure

While holding reserves is a prudent strategy, letting excessive dry powder sit idle for too long—especially as the average holding time for portcos has increased to 6.7 years—can create significant problems. "Aging" or idle dry powder is uncalled capital that remains un-invested late in a fund's designated investment period.

This creates immense pressure on GPs to deploy the remaining capital—navigating long holding periods and elevated levels of untapped dry powder—sometimes leading to rushed or suboptimal investment decisions.

This pressure can sometimes lead fund managers to make investments in lower-quality assets simply to avoid having to return the unspent commitments to LPs. As one expert noted, the sheer volume of available capital can influence market dynamics. As Arnie Fridhandler, partner at Weil, noted during Carta’s Lifecycle of a PE Deal webinar, the sheer volume of available capital can influence market dynamics. "Frankly there's a huge buildup of dry powder in the private equity world, but by and large, you know, most deals that certainly we see at Weil they do have a debt financing component to them."

This indicates that even with abundant equity capital available, the pressure to deploy it shapes how deals are structured, particularly in a landscape with fluctuating interest rates.

How uncalled capital impacts IRR and fund performance

When capital sits idle, it can create a phenomenon known as "capital drag." This is particularly relevant in the current VC landscape, which has seen notable slow capital deployment. For example, funds that closed in 2022 had deployed only 43% of their committed capital by the 24‑month mark—the slowest two-year deployment pace of any vintage in Carta’s dataset.

Therefore, undeployed capital that sits on the sidelines for too long can dilute the fund's overall performance and distributions to paid-in (DPI), even if the investments that were made turn out to be highly successful. The impact is tangible: while 25% of funds from the 2017 vintage had started generating distributions to LPs after three years, only 9% of funds from the 2021 vintage had produced any concrete results in the same timeframe. It's like a runner's time starting before they've left the starting block.

This makes it essential for a fund's CFO to have an accurate, real-time view of their fund forecasting and financials to manage liquidity effectively as part of a broader financial plan. An event-based general ledger, a core feature of Carta Fund Financials, provides the granular, up-to-the-minute detail needed to track the impact of deployment timing on fund performance.

This allows CFOs to move beyond stale, periodic reports and manage their fund with live data. This real-time visibility is essential for making informed strategic decisions.

How deployment history impacts future fundraising

The risks of mismanaging dry powder extend beyond a single fund's performance. When a GP goes out to raise their next fund, prospective LPs will scrutinize their tear sheets and track record of deploying capital from previous funds.

A history of significant idle dry powder can be a major red flag for investors, signaling potential issues with deal flow or investment strategy.

This makes operational excellence a key factor in building long-term investor confidence. For VC firm QED Investors, selecting a fund administrator that could scale with their growth was critical. As CFO Jamie Loving noted, the firm needed a partner with innovative technology to keep up with its needs.

Having a sophisticated, tech-forward back office demonstrates a commitment to professional management, which in turn helps build the LP trust necessary for future fundraising success.

From manual tracking to strategic forecasting

For years, fund managers have relied on a patchwork of disconnected spreadsheets and manual processes to track their dry powder. This approach is not only inefficient but also reactive and fraught with risk, making it difficult to plan strategically for a market downturn. The administrative burden of this approach is significant, especially as a fund's LP base grows. According to a 2024 report on VC fund managers, the median fund with between $1 million and $10 million in AUM raises that capital from 26 different LPs, while the median fund with more than $250 million in AUM has 104.

A modern, integrated platform offers a more strategic alternative, transforming how you manage your fund's capital.

Dry powder management | The manual way (Spreadsheets) | The strategic way (integrated platform) |

Tracking commitments | Manual entry from legal documents | Automated, single source of truth |

Forecasting reserves | Static models that quickly go stale | Dynamic, real-time scenario planning |

LP reporting | Periodic reports with lagging data | On-demand, transparent portal access |

Decision making | Reactive, based on outdated information | Proactive, based on live insights |

This strategic shift is enabled by tools like Carta Fund Forecasting. By connecting fund construction models and scenario modeling with live burn rate data and cash flows and portfolio data, it transforms reserve management from a guessing game into a data-driven exercise.

This allows GPs to model different scenarios, optimize their capital allocation and deployment, and ultimately work to maximize LP returns. It moves you from simply tracking your dry powder to strategically managing it.

Request a demo of Carta Fund Forecasting to learn more.

Frequently asked questions about dry powder

What is the difference between dry powder and cash reserves?

Dry powder is capital that has been committed by LPs but not yet called by the GP. Cash reserves, on the other hand, are liquid assets that a fund holds in its bank account after a capital call has been completed.

What happens if dry powder is not deployed by the end of the investment period?

If a fund's investment period expires, the GP typically loses the right to call the remaining dry powder for new investments. In this case, the LPs' unfunded commitment is usually extinguished.

How do capital recycling provisions in an LPA affect dry powder?

Capital recycling allows GPs to reinvest the proceeds or an early exit back into new deals. This can increase a fund's total investment capacity without drawing down its original dry powder balance. This is particularly useful for VC firms looking to support high-growth startups over a long-term horizon.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.