- Carta hits the Hill to expand retirement options for employees

- Topline

- Carta hits Capitol Hill in push to expand retirement options for employees

- SEC and CFTC propose sweeping Form PF rollback

- Treasury requests data from private credit firms

- Quick hits

- Upcoming events

- Sign up below to receive Carta's Policy Weekly Brief

Topline

Carta hits Capitol Hill in push to expand retirement options for employees

SEC and CFTC propose Form PF rollback

Treasury requests data from private credit firms

Quick hits

Upcoming events

Carta hits Capitol Hill in push to expand retirement options for employees

Carta CEO Henry Ward made the rounds in Washington, DC last week, meeting with SEC Chairman Paul Atkins, Acting Labor Secretary Keith Sonderling, House Financial Services Chairman French Hill, and other senior policymakers to discuss the evolving policy landscape for private capital. We discussed fundraising trends, employment, and productivity across startups and funds, and why the INVEST Act is critical to expanding access to capital for founders and fund managers in emerging ecosystems.

But Carta’s core message: Now is the time to modernize the retirement infrastructure to enable employees to contribute equity compensation to their 401(k)s.

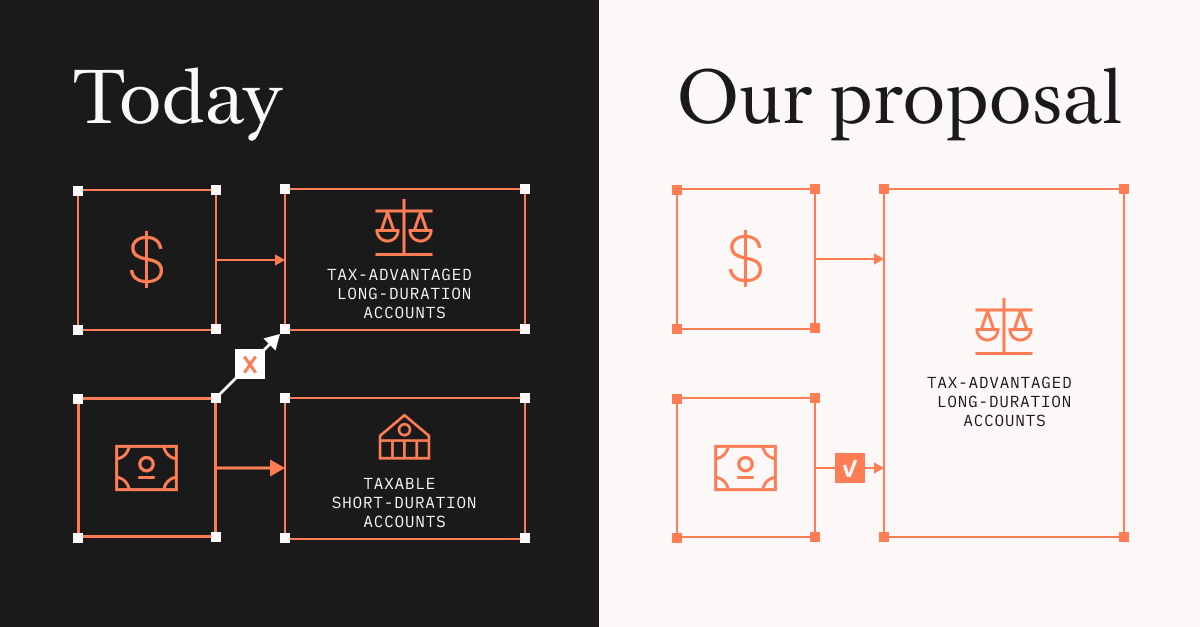

Background: The U.S. retirement system was built for a cash-wage economy, but that model no longer holds for a growing share of the workforce. At private, growth-stage companies, employees often receive a meaningful portion of their compensation in equity, sometimes rivaling or exceeding base salary. Yet there is no mechanism to contribute that already-earned, already-taxed, and already-owned equity into a tax-advantaged retirement account.

This creates a structural mismatch: Employees can contribute cash to a 401(k)—a long-duration account designed for long-term savings—but not their most valuable long-term asset. Private company equity is inherently long-duration, too. Employees typically can’t monetize it until an IPO, acquisition, or company-sponsored liquidity event—often years after the grant has vested. As companies stay private longer, more employee wealth is being created outside the public markets, while the retirement system remains tied to older assumptions.

Our proposal: Allow employees to contribute vested, exercised employee equity directly into their 401(k), subject to standard contribution limits. The income would be taxed at vest or exercise, so that any future appreciation, including liquidity event gains inside the retirement account, would be tax-free, consistent with how Roth accounts are designed to work.

Why it matters: Equity is how startups compete with large employers on pay. But without a retirement savings pathway, employees bear the illiquidity risk and miss out on the tax-advantaged growth that cash-compensated workers take for granted. This is a parity problem. Private company employees spend years building wealth outside the retirement system entirely. This proposal closes that gap without opening retirement accounts to new products or additional risk. It simply lets employees put compensation they already own into the savings vehicle best suited to hold it.

And for employees at earlier stages in their careers who may not have the ability to contribute cash, it would allow them to start saving for their future.

What’s next: Engagement is only the beginning. We will continue to build the case and pursue regulatory relief to modernize the retirement rules to reflect the modern economy.

In the meantime, we’d love to hear your thoughts on this idea. Reach out to policy@carta.com.

SEC and CFTC propose sweeping Form PF rollback

The SEC and CFTC proposed the most significant rollback of Form PF reporting requirements since the form was created under Dodd-Frank. Here are some notable highlights for private fund RIAs:

Filing threshold: Increases the general filing threshold from $150 million to $1 billion in private fund AUM.

Quarterly event reporting: Eliminates Section 6, the quarterly event reporting requirement added in 2023 covering adviser-led secondaries, GP removals, and fund terminations.

Private credit: Opens formal comment period on whether Form PF should be rebuilt around how private credit funds operate, including dedicated questions on leverage, loan maturity, credit quality, and investor liquidity.

Why it matters: Form PF has become a meaningful compliance burden, especially for smaller private fund advisers that lack scaled legal and operations teams. The threshold increase would take nearly half of current filers out of the regime while preserving most of the asset-level visibility regulators say they need. For larger PE managers, eliminating Section 6 would remove a sensitive quarterly disclosure requirement around fund lifecycle events, including continuation vehicles, at a moment when the secondary market is increasingly being used as a standard liquidity tool rather than a signal of distress. But the proposal is not simply deregulatory. By pairing broad relief with targeted questions on private credit, the agencies are signaling a shift away from one-size-fits-all reporting and toward a framework more tailored to where they believe risk may actually be building.

What’s next: There is a 60-day comment period following publication in the Federal Register. In the meantime, the October 1, 2026, compliance date for the existing 2024 amendments remains, though these proposals would likely supersede most of them with a separate 12-month transition window.

Treasury requests data from private credit firms

The Treasury Department has begun formally requesting detailed information from private credit firms regarding business models, recent performance, and relationships with banks and insurance companies. The outreach builds on months of closed-door meetings and now moves into structured data collection, with a particular focus on liquidity management practices and how firms are thinking about the DOL’s proposal to expand 401(k) access to alternative assets.

Why it matters: The ~$2T private credit market is navigating its first real stress test, with rising defaults in certain sectors, refinancing pressure, and growing tension between long-duration assets and periodic liquidity promises in retail-oriented vehicles. U.S. financial regulators have been clear that private credit does not currently pose systemic risk, framing recent dislocations as market events rather than stability concerns. But as the market moves closer to retail and retirement channels, regulators are aiming to build a clearer picture of how private credit behaves under stress, and whether existing structures can absorb losses without broader spillovers.

Expect Treasury to expand engagement with domestic and international insurance regulators as it assesses where risk ultimately resides in the system. The Fed is also pressing major U.S. banks for details about their exposure to private credit, while the SEC has requested comment on enhanced private credit reporting as part of its Form PF proposal.

Net/net: Retailization remains a priority, but it will likely come with a heavier emphasis on guardrails related to liquidity, valuation, and disclosure.

Quick hits

Private-equity holdings look overvalued. Who’s going to fix it? Valuation is becoming the pressure point for private markets as access expands toward retail and 401(k)s. Exits came in below paper valuations last year for the first time in recent history, secondary market discounts hit 13.9% in 2024, and an industry leader has claimed that “all the marks are wrong” on PE-backed software. The SEC has issued several valuation penalties this year and is forming a new unit to investigate audit firm misconduct. However, LPs claim they aren’t seeing meaningful changes from GP behavior. As private markets move closer to retail channels, valuation gaps shift from a performance issue to a core investor protection risk—putting pressure on audit standards, disclosures, and regulatory scrutiny in the next phase of market development.

White House and Anthropic hold ‘productive’ meeting, aiming for a compromise. Anthropic CEO Dario Amodei met with White House Chief of Staff Susie Wiles and Treasury Secretary Scott Bessent last Friday to discuss Mythos, the company’s new AI model capable of identifying—and potentially exploiting—software vulnerabilities. The White House called the meeting “productive and constructive.” The sit-down signals a potential thaw in the standoff between the administration and Anthropic, which has been locked in a legal and political fight with the Pentagon since Defense Secretary Hegseth declared the company a supply chain risk after Anthropic refused to allow its AI to be used for autonomous weapons and mass surveillance. A federal judge blocked the SCR designation from applying to civilian agencies in March, but the DC Circuit declined to bar DOD from cutting ties while litigation continues. On the access front, OMB has already told civilian agencies it is preparing to give them access to Mythos, and CISA is among the intelligence community components already testing it, suggesting a path forward that routes around the unresolved Pentagon dispute rather than resolving it. Anthropic is rolling out the model through Project Glasswing, a cybersecurity initiative with Amazon, Apple, Google, Microsoft, and JPMorgan Chase, with no plans for public release.

Senate sends Investing in All of America Act to President’s desk. The Senate passed the Investing in All of America Act, sending it to President Trump’s desk for signature. The legislation modernizes the Small Business Investment Company (SBIC) program by increasing standard debenture leverage limits and excluding investments in rural and low-income communities, critical technology, and small manufacturers from SBIC leverage calculations, enabling more private capital to flow to underserved markets and strategic sectors.

ICYMI: Carta’s former Head of Policy Anthony Cimino testified in favor of this important legislation.

What to know about tariff refund site that launches Monday. U.S. Customs and Border Protection (CBP) launched a portal system for businesses claiming refunds on Trump-administration tariffs the Supreme Court ruled illegal. More than 300,000 businesses paid an estimated $166 billion in tariffs, making the refund the largest in U.S. history. Importers of record and authorized customs brokers may apply, but the process is tiered and not all claimants eligible in phase one. Refunds process in 60-90 days if approved, but the timeline on forthcoming phases are unclear, signaling potential delays.

Upcoming events

Carta Webinar: Capital Is Up. Hiring Is Down. The New Rules of Startup Comp. - April 23 at 10:00 a.m. PT/1:00 p.m. ET

Carta Webinar: The Non-Dilutive Capital Stack - April 28 at 10:00 a.m. PT/1:00 p.m. ET

Carta Event: NYC Spring Policy Dinner - April 28 at 3:00 p.m. PT/6:00 p.m. ET

Carta Webinar: From First Meeting to Final Close: The Power of a Connected CRM - May 4 at 10:00 a.m. PT/1:00 p.m. ET

Sign up below to receive Carta's Policy Weekly Brief

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.