Topline:

Shutdown endgame

GP and LP considerations as retail investors come to private markets

SCOTUS signals skepticism over Trump’s tariffs

Quick Hits

Shutdown to the shutdown? Maybe.

Day 38 of the government shutdown. But there may be a deal in sight. The Senate plans to vote on a funding package that would extend the funding date of the House-passed continuing resolution until January and combine it with full-year spending bills for three departments. Senate Majority Leader John Thune does not know if it will pass with sufficient Democratic support, but is optimistic. Senate Democrats remain a bit skeptical.

Next steps: The Senate will consider the bill today and through the weekend. Even if it falls—which seems likely—it could open the door for more constructive talks. If the Senate passes it, the House should follow—barring a late revolt from the right flank or opposition from the president—to reopen the government next week.

Private markets are going public.

What does that mean for GPs and the LPs whose money they invest?

First, some background: Historically, policymakers sought to make it easier—and in some cases forcibly push—companies to go public. But even with the recent uptick, IPOs remain limited, and the growth of private capital and private assets remain strong.

So rather than bring private assets into public markets, policymakers and industry are focused on bringing public investors into private markets.

The how:

Accredited investor: Policymakers plan to expand on-ramps to overcome restrictions for retail investors to invest in private markets. More on that in the coming weeks.

Retirement accounts: President Trump signed an executive order to unlock portions of the ~$12.5T pool of capital in 401(k) retirement accounts to invest in private assets.

Investment products: Investment managers are increasingly filing for products that allow retail to invest in strategies that contain alternative assets. Those filings doubled this year; as approvals start happening, expect the number to grow.

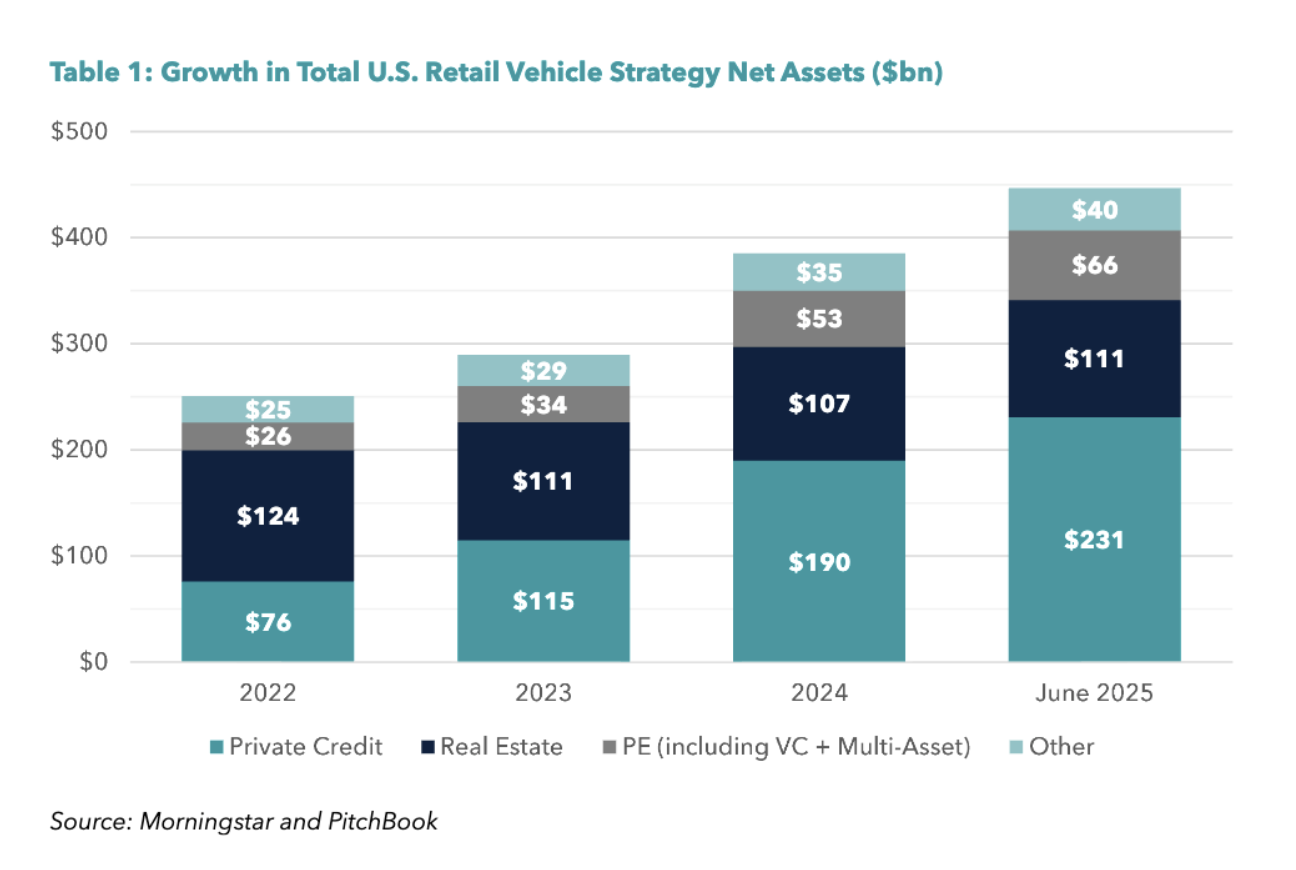

Distribution development: As more alternative asset offerings emerge, more distribution channels will feed them. While institutions hold ~20 - 50% in alternatives, private wealth portfolios hold only 2-5% in the asset class. Wealth managers will start to increase those allocations, and with each percentage point, $500B floods into the market.

The impact: More capital. More opportunities. More expectations. More scrutiny.

Retail investors control nearly half of global wealth, representing ~$140-150T. Not all retail investors will allocate into alternatives, but expanding the portion of investors who will and increasing the allocation for those who do, drives more capital and more opportunities into funds, companies, innovators. But that comes with more expectations and more scrutiny.

Why does this matter to GPs?

Retail investors will expect greater access to liquidity than their institutional counterparts. Although retail may have less influence on GPs given they are more fragmented and write smaller checks, retail will expect pertinent reporting and transparency. And importantly, as more investors get access to markets, regulators will scrutinize those markets more closely to protect investors. Below are some key impacts GPs may need to consider:

Performance, fees, and expenses: Private assets provide growth and diversification, but often come with higher fees. GPs should expect heightened scrutiny on this from investors in the near-term and from regulators in the long-term. That scrutiny will come in time with more complex compliance, as well as increased regulatory, litigation, and reputational risk.

Liquidity management: GPs accustomed to closed-end funds may need to adjust liquidity management practices as they create vehicles—interval, evergreen, etc—that create redemption opportunities. This strikes at strategic alignment and education with retail investors, but when an investor expects to pull capital and cannot, everyone suffers.

Disclosures: Funds will increasingly be expected to have credible, timely valuations and credible financial reporting. If only there were a platform — that also had an amazing policy team—to help with that. Check out Carta CEO, Henry Ward, talk about our valuations product.

What should LPs be thinking about?

As more retail capital comes to market, incentives between institutional and retail LPs may diverge, and as a result, getting clarity on LP-GP dynamics will be key. The Institutional Limited Partners Association (ILPA) released a report to mapped out areas LPs should consider:

Investment strategy and discipline: more capital and increased expectations around deal flow and liquidity may test a GPs investment discipline or alter how GPs think about their timing and long-term strategy.

Expenses and cost allocation: LPs should understand how their fees are allocated and whether they are allocated to the retail vehicle. This includes expenses on sourcing, warehousing, compliance, and other matters, but also personnel allocation.Co-investment: LPs increasingly focus on co-investment opportunities, but those could decline as GPs may have more expansive co-investment capital from retail capital to invest.

Incentive alignment: Carried interest is predicated on aligning GP-LP incentives. Understanding how that meshes and is computed alongside a retail vehicle is key, as a lower hurdle rate or calculations based on realized or unrealized net asset value could have a big impact for LPs.

The future is here. It is just not evenly distributed…

Retail expansion into alternatives will not be uniform across the asset class, but rather depend on the asset class and vehicle. For asset classes, adoption has and will continue to focus on private credit, real estate, and traditional private equity.

The reason? These investments tend to invest in assets that can be easier to value, have shorter duration (than say VC), and enable more predictable liquidity management. Translation: fund managers can better set valuations, duration expectations, and liquidity redemptions for investors.

Hot take from Carta Policy: Retail may not be too interested to invest in venture capital, and venture capital may not be too interested in taking retail capital right now. But we think that will change. Venture may be riskier and require longer-term holds, but investors like the idea of outsized returns. And venture GPs like the idea of more capital. So as we build better infrastructure to create more accurate and timely valuations, portfolio management, and financial reporting — which Carta is doing — expect venture to tap more into retail.

Bottom line: Private capital is the economic and innovation engine of this nation. We should expand investor access to enable more people to participate in the economic journey, as well as drive this engine forward. But as that landscape changes, the consideration of fund managers, their limited partners, and the regulators scrutinizing them will evolve.

If you are in New York next week, Holli Heiles Pandol will be discussing this and more at Kroll’s Private Investment Valuation and Compliance conference. Register here.

Tariffs do not please the Court

A majority of justices on the Supreme Court seemed skeptical of President Trump’s unilateral tariff regime, signaling they may overturn it. The administration argued the president has the authority to impose tariffs to regulate foreign commerce, and the related tariff revenue is incidental, but justices on both sides questioned the ability of the executive to unilaterally implement policy that functions like a tax. To date, President Trump’s tariffs have raised $226B, substantially higher than the ~$82B raised from tariffs at the same time last year.

Why it matters: If the Court holds the tariff regime is unconstitutional or significantly limits its scope, the consequences could include:

Revenue return: The administration may be on the hook to return billions of the revenue raised.

Deficit reduction: The tariff revenue was ostensibly going to offset a large portion of the deficit spending incurred by the recent tax bill, H.R. 1, which could increase pressure on the federal budget.

Trade: A reversal could effectively lift the tariffs on a go-forward basis — at least in their current or adjacent form — which could ease commercial burdens and alter supply chain incentives.

Geopolitical leverage: It would also strip the President of his preferred negotiating lever in navigating foreign policy, trade deals, and economic dynamics.

Carta Policy at The Big Exit

The Carta Policy Team was at The Big Exit Nashville this week to discuss how retailization and other policy shifts will create opportunities for small businesses and their investors. We discussed:

Key developments on the shifting regulatory landscape—from the government shutdown to tech policy

How the current environment is creating opportunities to drive successful exits and innovation

How to use policy levers like QSBS and employee ownership to maximize and enhance value and drive growth

Thanks to Bregal Sagemount for such a great event!

Quick hits

First Brands races to secure $600M to avoid “game over” liquidation. First Brands, the auto parts manufacturer that defaulted, kicking off questions of private credit practices is fighting to secure debtor-in-possession financing to stave off liquidation. This is happening in the background as lenders fight over $1.1B in court. Whether it does or not, expect increased scrutiny on private credit lending practices.

Nancy Pelosi to retire. The first—and only—female Speaker of House, leading Democrat, and San Francisco stalwart will not seek reelection.

Nvidia CEO believes China will win AI race. Nvidia chief executive Jensen Huang has warned that China will beat the US in the artificial intelligence race, thanks to lower energy costs and looser regulations.

Sign up below to receive Carta's Policy Weekly Brief

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.