For startups and their founders, it’s growing more and more difficult to raise a pre-seed round.

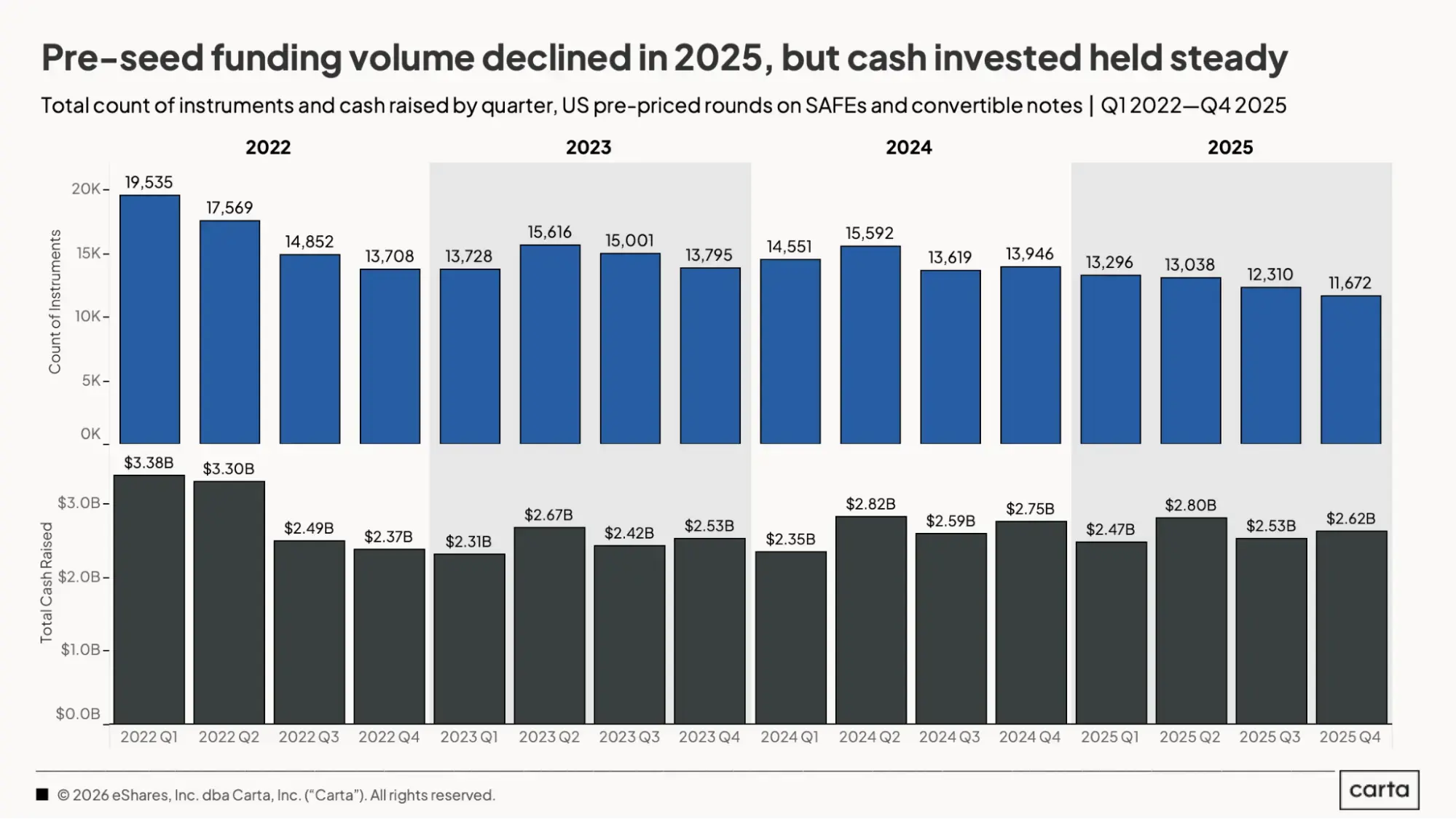

Over the past several years, the number of pre-priced rounds raised on Carta has been in a state of steady decline. In Q4 2025, startups closed 11,672 pre-seed deals, a 16% drop from the same period a year earlier. Compared to the first quarter of 2022, pre-seed dealmaking has declined by 40%.

As the pre-seed funding market tightens up, VCs say there are several ways that startups seeking early-stage funding can stand out. There’s no way to guarantee a successful fundraising; even the best companies are still dependent to some degree on timing, luck, and other factors beyond their control. But here are seven things founders can do to improve their odds in the pre-seed fundraising market.

1. Find the right co-founders

By definition, companies aiming to raise a pre-seed round are often in the earliest stages of attempting to turn their idea into a viable business. As such, these companies often lack proof points that are common among more mature companies, such as revenue. In some cases, pre-seed startups don’t yet have a minimum viable product.

Investors, then, must look at other variables. For Maria De Santis, a principal at Muse Capital who invests in early-stage consumer tech, one of the best clues about how pre-seed startups will fare is the makeup of their founding teams.

“When we’re investing at the very early stages, it’s really about the people and the team,” De Santis says.

Specifically, De Santis prefers founders who have started a company before or have been early employees at a young startup—those who have had a “front-row seat” to building a business from scratch.

If a company has multiple founders, she likes them to have complementary skillsets. And even if skillsets overlap, a team of co-founders is usually preferable to a single visionary trying to go it alone.

“We have a preference toward founding teams, versus solo founders,” De Santis says. “This is a long journey, and in our experience, we’ve seen founding teams do better.”

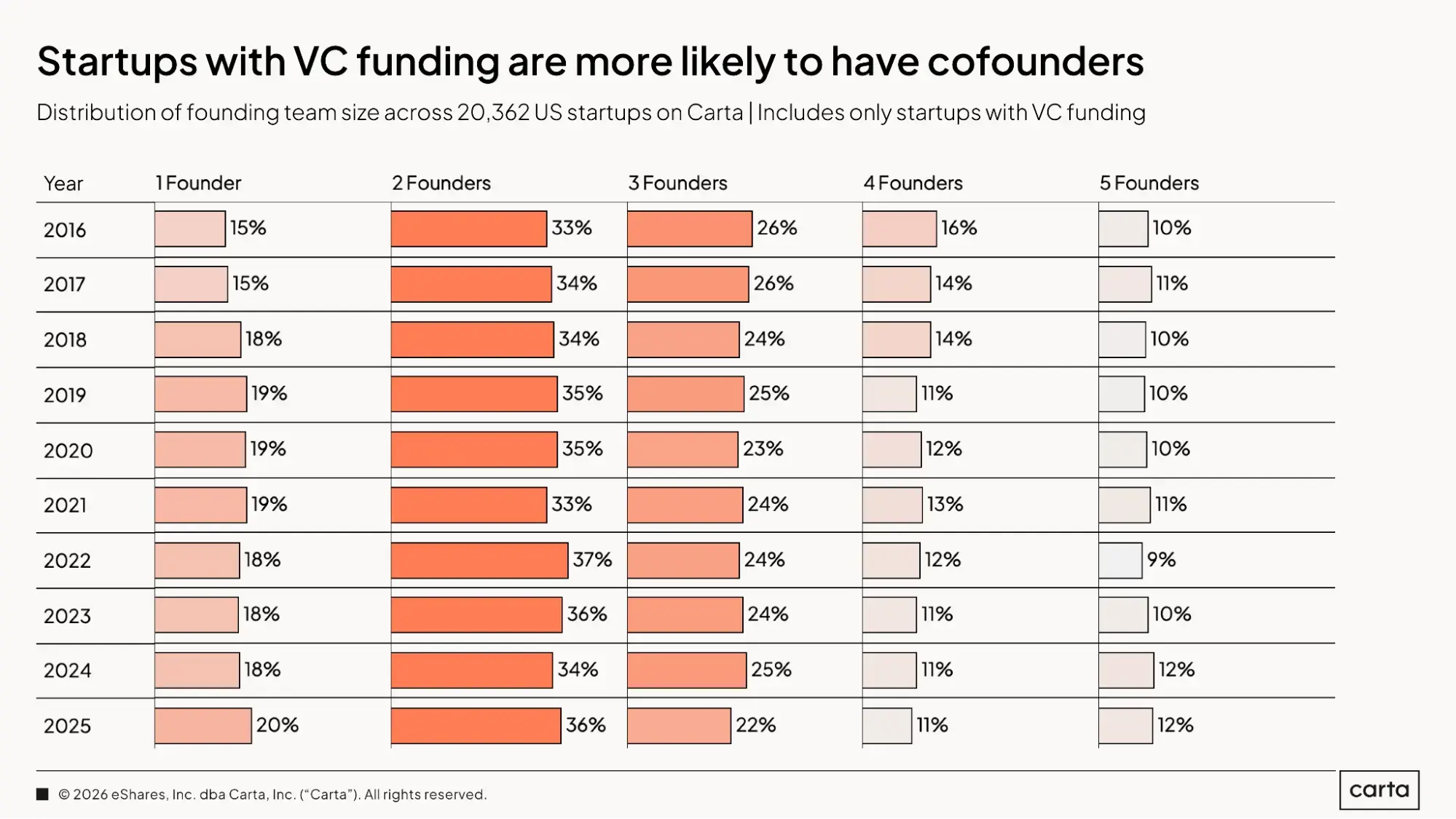

At later fundraising stages, this anecdotal evidence is backed up by the data. Last year, 80% of companies that successfully raised capital across all funding stages had multiple founders, with two-founder teams being the most common construction.

2. Know your market

So you have a plan for a new startup. Who’s going to buy your product? For early-stage founders, having deep knowledge of the market in which your company operates is a baseline necessity.

This market knowledge is important for multiple reasons. At a basic level, demonstrating expertise is one of the best ways to convince VCs that you know what you’re doing. De Santis, who has been investing in consumer tech for several years now, says she’s always looking for founders who know more about the space than she does.

But market knowledge will also help decide which VCs you spend your time trying to pitch to. A company with a smaller total addressable market (TAM) might appeal to different firms than one with a larger TAM, because the size of the TAM usually correlates to the potential financial return that an investment might produce.

Knowing your market can be particularly important in a climate of reduced deal activity. When investors are pickier about cutting checks, possessing the right expertise and pitching to the right VCs is more important than ever.

“The team and the market are the two most important factors when underwriting pre-seed opportunities,” De Santis says.

3. Know your comps

When your company might be little more than an idea and a dream, it helps to have other, more established ideas against which to compare it.

Pitching your vision is one thing. But Samyr Laine, co-founder of early-stage investment firm Freedom Trail Capital, says using comparables is the best way to make that vision come to life for investors. If VCs can see the link between your own startup’s plan and how other successful companies have executed, they’re more likely to be interested.

Startups can compare themselves to other peer companies in several different respects, ranging from key metrics like revenue and growth to potential pathways to an exit. Having an evidence-based argument for why your startup will succeed can be a powerful tool.

“The best pre-seed companies are looking at corollaries between other categories and other startups, and always have a defensible moat in mind,” Laine says. “They’re using analogies in comparison to other successful startups—for instance, ‘We’re trying to build the Uber of this space.’”

4. Have a plan—but know you’ll probably change it

No pre-seed founder can predict with much confidence the direction their company will go over the next 18 months, let alone the next decade. Pre-seed investors know the future is shrouded in uncertainty.

Still, they want founders to come into meetings with a business plan for how the company will proceed in the years to come, even as they know the plan will almost certainly shift.

“I like to see some initial analysis,” De Santis says. “But it’s not about the numbers that they’re showing me. It’s more about seeing how they think about it. We’re always looking at their business model, because we want to see how they are thinking about growing the business—what are the levers they’re pulling to scale?”

For Laine, a pre-seed business plan is more like an outline than a final draft. The specific details will certainly change, but the broader narrative needs to make sense.

“What we want is a realistic story,” Laine says. “Walk me through how we’re going to do this.”

5. Move fast to market

For pre-seed founders, perfect can be the enemy of good.

Conducting market research and iterating on initial designs are important steps in the process of going to market. But De Santis advises early-stage startups to remember that their initial launch will not be flawless. Sometimes, the best feedback on an early product comes not from internal processes, but from customers themselves. The faster a company can start learning what the market wants, the better.

“A mistake I’ve seen in the past is spending too much time trying to get this perfect product out, versus just getting it out and gathering initial feedback,” De Santis says.

This can be done more easily in some sectors than others. For instance, startups building SaaS tools or other software-powered products will likely find it easier to iterate quickly based on market feedback than startups making consumer goods or complex hardware.

6. Appeal to VCs’ bottom line

Investors, of course, don’t decide to write a check to a pre-seed startup because they’re feeling generous. VC investment decisions are typically based on the return they think a deal might generate, and whether that return fits into the larger economics of their specific fund.

Sometimes, Laine says, this seems like a fact that founders forget.

“A fund has its own investors,” Laine says. “They’ve got a return rate they need to clear in order to make the math work. What happens too often is a founder is looking for investors without thinking about what the investor wants and needs to make their money back.”

Pre-seed founders can increase their appeal to VCs by addressing this fact head-on. What’s your expected timeline for an exit? Based on your TAM and other comparable startups, what sort of return should investors expect? The answers to these questions will also inform your thinking about which VCs may be a good fit for your startup.

Again, VCs know even the best-laid plans of a pre-seed startup will probably go awry. Rather than producing accurate projections, addressing potential returns at such an early stage is more about proving to VCs that you’ve started to think about an end game—and that you’re thinking about raising capital as a two-way street.

“You have to think about alignment,” De Santis says. “Does what I’m building fit with this fund’s thesis? Does what I’m trying to build align with the returns that the investor is trying to target?”

7. Keep your eye on the prize

How much cash should a company try to raise in a pre-seed round? Most VCs agree that the answer is relatively simple: However much you think you’ll need to make it to a seed round.

Some of the key landmarks that investors tend to look for at the seed stage include early revenue, early signs of product-market fit, a minimum viable product, and some level of insight into customer-acquisition costs and how the company plans to lower them in the future.

In planning out early-stage spending, Laine advises founders to maintain a laser focus on these sorts of variables, or whatever other metrics a founder believes will allow them to reach the next fundraising checkpoint.

“We want to see as tight a budget as you can,” Laine says. “That will dictate the dollar amount that you need and what you’re going to use it for. It doesn’t mean that things don’t happen, surprises don’t pop up, and plans don’t change, but starting with a clearly defined plan is a great launch point.”

Subscribe to the Data Minute newsletter

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.