For private equity and venture capital firms alike, it’s been a quiet past 18 months for raising new capital.

In PE, the number of new funds closed by GPs was down 44% year over year in 2025, while total cash raised dipped by 24%. The first quarter of 2026 was even more sluggish. In VC, new fund formations dropped 41% year over year in 2025, and cash raised was down 37%.

Investors cite multiple reasons for this slowdown in the fundraising market. The primary cause is the relative dearth of IPOs and other exits in recent years. This limits the amount of capital flowing back to LPs, which in turn limits the cash those LPs have available to invest in new funds. The rise of AI has also caused turmoil in the markets, such as the so-called SaaS-pocalypse. That turmoil has led some LPs to pause and reconsider whether their previous investment strategies still make sense in a new, AI-powered age.

“There’s been little liquidity, and you add that to the contraction in general public SaaS—I think those two things, in tandem with all things AI, have created a lot of uncertainty,” says Bobby Ocampo, co-founder and managing director at Blueprint Equity, a growth equity firm that invests in tech companies. “You have uncertainty in what to invest in, and it’s just kind of making everyone nervous. I’m not surprised the slowdown has continued.”

“A flight to certainty”

In this uncertain environment, some LPs are defaulting to what they know best. For instance, at first glance, VC fundraising got off to a roaring start in 2026. It was the strongest Q1 for fundraising on Carta since 2022, with newly closed funds across the full breadth of the market totaling nearly $48 billion in commitments—already about 72% of the way to last year’s annual total. But more than three-quarters of that capital was concentrated in just six mega-funds raised by some of the largest names in VC. For the rest of the market, it’s not so rosy.

From Ocampo’s perspective, this sort of concentration is to be expected. When the ground under their feet is shifting, LPs are less likely to make new, risky bets and more likely to allocate capital to well-known managers with well-established track records.

“I don’t know if it’s a flight to quality so much as a flight to size, a flight to certainty,” Ocampo says.

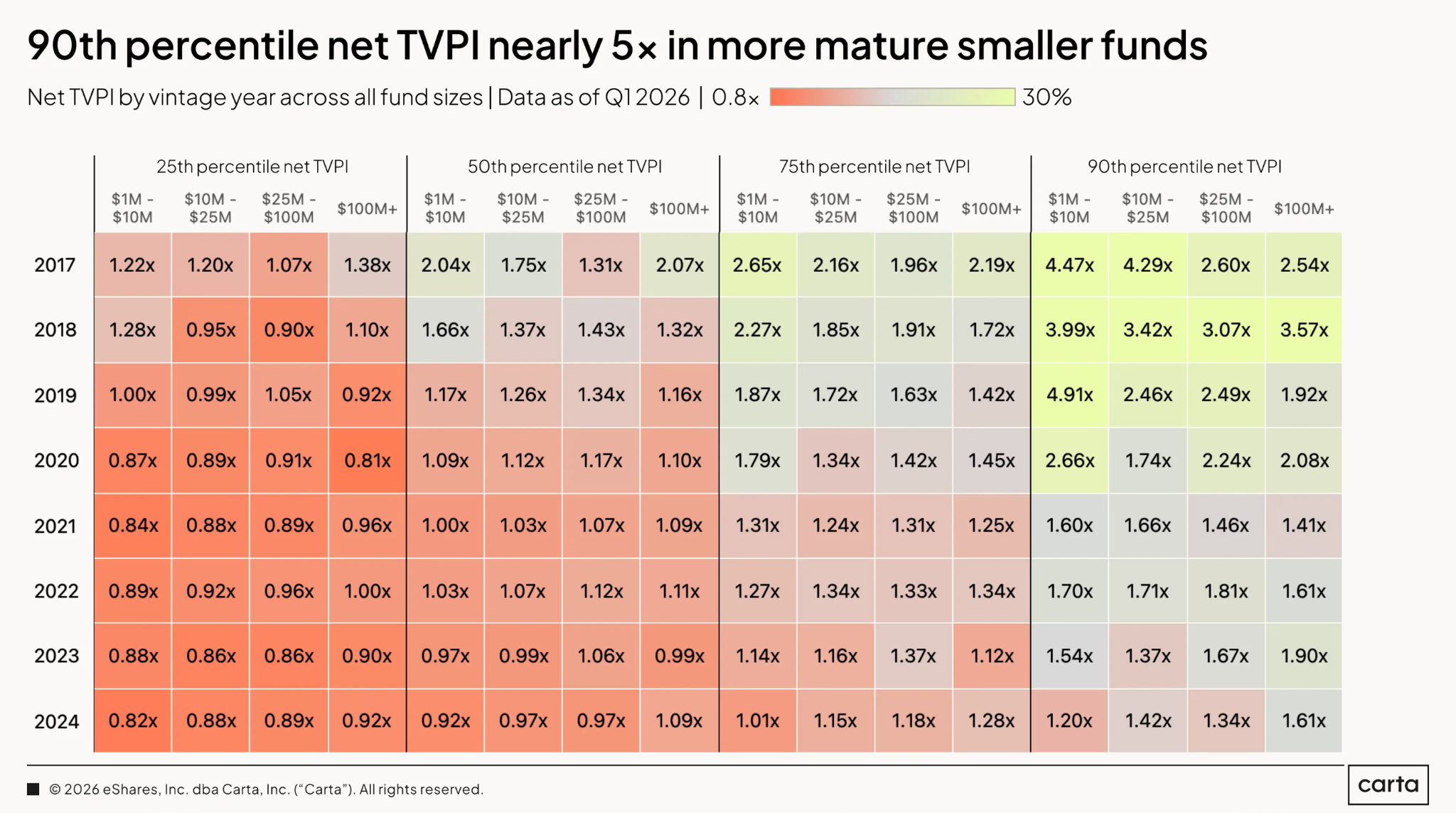

However, this inclination comes with a tradeoff. While large upmarket funds may be attracting the majority of LP capital, it will be difficult for many of those funds to produce the sorts of return multiples most LPs expect. The reason is simple math: It’s typically much harder to generate a 3x return on a $10 billion fund than a $10 million fund, because the amount of profit that must be created is also proportionally larger. There are plenty of scenarios in which a $10 million fund might produce a $20 million return. The opportunities to produce a $20 billion return, meanwhile, are few and far between.

There are certainly exceptions to this rule. In general, though, smaller funds tend to outperform larger ones as measured by TVPI, particularly at the top end of the market.

While large, established funds may present more certainty for LPs, they also offer less upside.

“Once you get to a certain size, it’s really hard to generate the kind of returns that LPs really want,” Ocampo says.

Why emerging funds are thriving

Some LPs, then, find themselves looking in the opposite direction. In addition to the industry’s biggest players, Ocampo says another group of firms is also finding fundraising success in recent months: emerging investors raising smaller, specialized funds that operate within a particular well-defined niche. They’re doing so by presenting a clear value proposition to investors, a differentiated strategy that allows them to stand out from the rest of the pack.

Jeff Barrington, founder and managing director at investment bank Windsor Drake, is witnessing the same dynamic. A barbell is emerging in the market, with some of the smallest and largest firms successfully raising funds while those in the middle face stiffer headwinds.

“We’ve definitely seen more interest in specialized funds with a very clear story. And they are typically smaller funds,” Barrington says. “Specialization really seems to be winning right now. It’s just hard to get investors excited if you don’t have a very clear value proposition.”

That value proposition might be around industry expertise. It might be around operators who can help companies achieve organic growth. It might be around access to deals. The details of the strategy aren’t necessarily the important part. What LPs want to see is a clearly defined, differentiated approach that other funds can’t imitate.

“With the right strategy and a specialized approach, we’re seeing some funds really doing very well,” Barrington says.

“The haves and have-nots”

But these specialized, emerging funds don’t present a perfect investment profile for every LP. Yes, their smaller size makes it more mathematically realistic for them to produce a large return multiple. On the other hand, that smaller scope also limits the amount of cash that LPs can invest.

For a major LP managing many billions of dollars, making a $1 million commitment to a small, specialized fund might produce a strong return. But even a 5x or 10x multiple barely makes a dent in their overall portfolio. Meanwhile, performing diligence on such funds and staying up to date on their performance takes time, effort, and money. For these larger LPs, investing in smaller funds may not be worth the effort, no matter how much alpha they generate.

But that’s a problem for the LPs, not for the managers of smaller funds. In Ocampo’s experience, these managers are still seeing plenty of demand, even if they’re not a perfect fit for every allocator.

“All the things in the middle are having a very tough time right now,” he says. “You’re not in the best companies. You’re a big fund, but with mediocre returns. It’s a tough spot to be in. But if you’re in this niche category, it’s actually a great spot to be in right now, because you’re generating true alpha.”

Ocampo is speaking from experience. In January, Blueprint Equity closed its third flagship fund within 12 days, a $333 million fund it says was significantly oversubscribed.

It’s not impossible to close a new fund today. But for those funds in the middle of this barbell-shaped market, it may be a challenge.

“Across every asset class,” Ocampo says, “it is very much the haves and the have-nots right now.”

Subscribe to the Data Minute newsletter

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.