- Private capital explained: How the ecosystem works

- What is private capital?

- How private capital differs from public markets

- What are the types of private capital?

- Venture capital

- Private equity

- Private credit

- Real estate

- Infrastructure

- How are private capital funds structured?

- Fee structures

- Special purpose vehicles

- Why private capital is attractive

- What are the risks of private capital?

- Managing the private capital lifecycle from fundraising to wind-down

- Fund formation and closing

- Capital deployment and portfolio management

- Reporting, distributions, and wind-down

- The evolution of fund operations: Then and now

- Building the operating system for private capital

- Frequently asked questions about private capital

- Who can invest in private capital?

- Why do investors allocate to private capital?

- What’s the difference between private capital and alternative investments?

- What is the role of a fund administrator in private capital?

- What is the difference between private capital and private equity?

- What is the difference between private credit and private capital?

- Is venture capital a form of private capital?

What is private capital?

Private capital is an investment made directly into private companies and alternative assets that are not traded on public stock exchanges, like the New York Stock Exchange (NYSE) or Nasdaq. This defining characteristic places these investments within what is known as the private markets, a space where deals are negotiated directly between investors and companies. This entire ecosystem operates away from the daily fluctuations and high visibility of public trading, allowing for a different approach to investment and company growth.

Private capital reaches companies through a variety of participants. While some investors participate as individuals—such as angel investors who invest their own capital directly into early-stage companies—the majority of private capital flows through professionally managed funds. In these funds, capital is raised from investors and deployed by professional fund managers into a wide range of private assets. These investments are typically held for many years with the goal of increasing their value before being sold. The eventual sale is how investors realize their returns.

Fund-based private capital is built around two key types of participants. General partners (GP) are the professional fund managers who raise capital and are responsible for finding, managing, and exiting investments. Limited partners (LP) are the investors—such as pension funds, endowments, family offices, and high-net-worth individuals—who commit their money to these funds.

This form of private investment is a vital engine for the economy, fueling growth by injecting massive amounts of capital into innovative companies. In 2025 alone, startups on the Carta platform raised nearly $120 billion in new funding, demonstrating the immense scale of this economic force. This empowers companies to focus on long-term strategy and innovation, which can lead to significant growth.

How private capital differs from public markets

To understand private capital, it’s helpful to see how it compares to the public markets. The primary differences relate to who can invest, the level of regulatory oversight, and how easily an investment can be sold. These distinctions create a different environment for investors and companies alike, with unique risks and opportunities.

Aspect | Public markets | Private capital |

Investor access | Open to the general public for buying and selling. | Typically restricted to accredited investors and institutions. |

Regulation | High level of regulatory oversight, with listed companies required to make extensive public disclosures of their financials and operations. | Fewer public disclosure requirements, offering more privacy. |

Liquidity | High, as assets can be bought and sold easily on an exchange. | Low, as investments are illiquid and typically held for many years. |

Transparency | Financials and operations are publicly disclosed. | Investor reporting is shared privately. |

What are the types of private capital?

While the term private capital sounds singular, it is actually an umbrella term for several distinct investment strategies, also known as asset classes. Each strategy shares the common thread of investing in private assets, but they all have unique approaches, risk profiles, and operational demands for the fund managers who run them.

Understanding these different types is the first step to grasping the full scope of the private markets. The most common forms of private capital are:

Venture capital

Venture capital (VC) is a specific type of PE that concentrates on making minority-stake investments in young, high-growth companies, commonly called startups. Unlike traditional PE, which targets stable businesses, VC funds embrace higher risk for the potential of much higher rewards.

VC operates on a power-law dynamic: within a single fund's portfolio, the expectation is that most investments will fail or return modest amounts, while one or two breakout companies drive the majority of returns. The fund's ability to capture those rare big wins ultimately determines its overall performance. This is measured at the fund level using total value to paid-in capital (TVPI)—a ratio of the total value returned to investors relative to what they put in. A TVPI of 3x is often cited as a benchmark for strong performance. Data from 2017 vintage funds shows the median net TVPI sits at just 1.76x, while the top 10% of funds reached 3.52x or higher—confirming that outsized outcomes are concentrated in a small number of top-tier funds.

Private equity

Private equity (PE) is an investment strategy that focuses on acquiring ownership—often a majority stake—in established, mature companies. The primary goal of a PE fund is to actively improve the company's operations, strategy, and financial health over several years. This hands-on approach is a key differentiator of the asset class.

After a period of creating value, the PE firm seeks to sell its stake at a profit. This final sale is known as an exit, which is how returns are generated for the fund's investors. EExits are a goal for all private capital investors, not just PE firms; they are the mechanism by which returns are ultimately realized and passed on to a fund's investors. For PE firms specifically, common exit routes include selling to another company, a buyout by another firm, or by taking the company public through an initial public offering (IPO).

Private credit

Private credit is a strategy that involves providing privately negotiated loans to companies, rather than buying ownership in them. This is a fundamental difference from PE and VC, as a private credit fund acts as a lender rather than an investor. Returns are generated from contractually obligated interest and principal repayments.

This asset class has grown as companies seek more flexible and faster financing than traditional banks can often provide, sometimes involving mezzanine financing or restructuring of the existing capital structure.

The focus on direct lending rather than owning creates a completely different operational workflow for the fund. Instead of tracking ownership, the fund administration team must manage loan operations, monitor interest payments, and ensure compliance with loan terms. This shift requires a specialized operational setup, like Carta's private credit solutions, to handle the unique demands of debt investing.

Real estate

This investment strategy focuses on acquiring, developing, or managing physical properties instead of buying shares in a company. These properties can include commercial offices, residential complexes, warehouses, or retail spaces.

Returns are generated through two primary channels: consistent rental income and the appreciation of the property's value over time. This dual-track return profile allows investors to use real estate as both an income-generating asset and a hedge against inflation.

Infrastructure

Infrastructure investing involves putting capital into the essential physical systems and services that support economic activity. This includes assets like toll roads, airports, power grids, renewable energy projects, and water or telecommunications systems.

These assets are often considered defensive because they can operate as natural monopolies or under long-term government contracts. This structure provides predictable, inflation-linked cash flows. These assets are vital to society, which is why they typically offer lower volatility and greater resilience during economic downturns, much like fixed income assets. This resilience is reflected in recent investment trends; in the two years leading up to Q2 2025, cash raised by hardware startups—a category that includes renewable energy and transportation—grew by 110.4%. This outpaced the 91.2% growth for SaaS startups over the same period, underscoring investor confidence in tangible, essential assets even after a market slowdown.

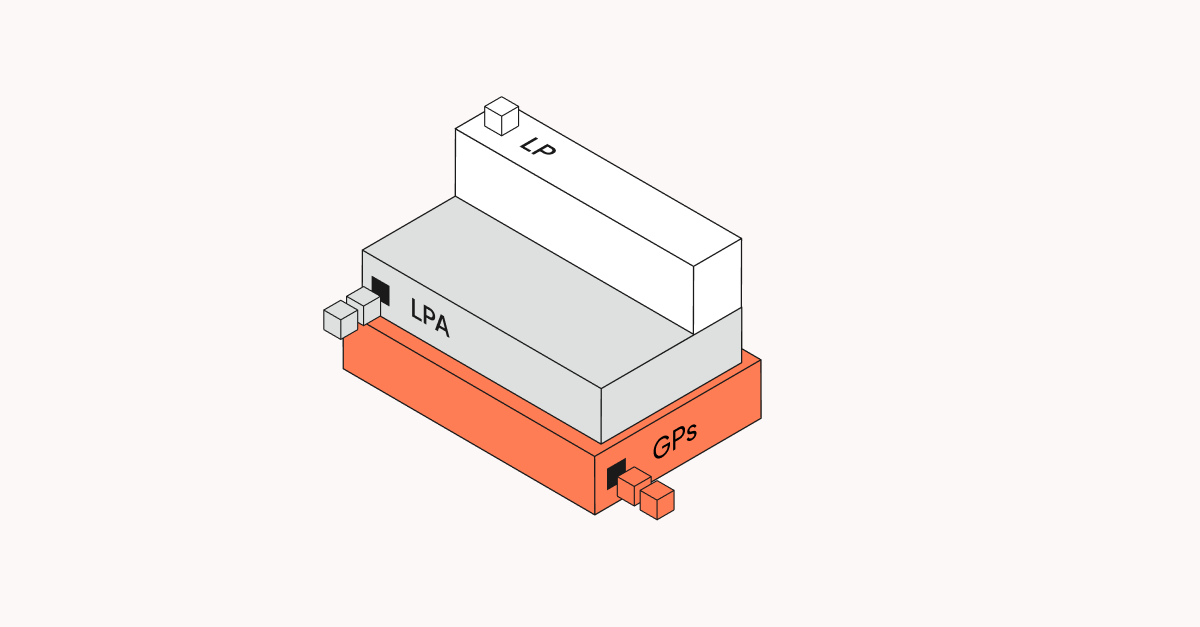

How are private capital funds structured?

The most common of the fund structures for a private capital investment is a traditional fund, which is a large, pooled investment vehicle. Typically formed as a limited partnership, these funds have a long-term investment horizon and invest in a portfolio of multiple companies. This diversification helps spread risk across different investments. This structure legally separates the roles and responsibilities of the active managers (GPs) and the passive investors (LPs). This protects the LPs from liability beyond their investment amount.

The foundational legal document for this structure is the limited partnership agreement (LPA). The LPA acts as the rulebook for the fund, defining the key terms governing the relationship between GPs and LPs—including fee structures, fund duration, governance rights, capital call procedures, and how profits will be distributed.

Fee structures

Across VC funds of all sizes, the classic "2 and 20" fee structure remains the industry norm. This includes a management fee, typically 2% of the total fund size, for making investment recommendations. Separate from the management fee, GPs also earn carried interest—typically 20% of any profits generated by the fund. This performance-based compensation is designed to align the GP’s incentives with those of the LPs: the GP only receives carried interest after investors have gotten their capital back. However, some variation emerges when looking beyond the median. For smaller funds between $1 million and $10 million, the bottom decile of carried interest is 15%. For the largest funds with more than $100 million in commitments, the top decile can climb as high as 30%, suggesting that managers of top-tier funds have the leverage to command a larger share of profits.

Special purpose vehicles

A more focused alternative to a traditional fund is the special purpose vehicle (SPV), a legal entity created to make a single investment rather than building a diversified portfolio. Like traditional funds, SPVs are often also structured as limited partnerships, but their narrow scope and simpler setup make them a popular tool for emerging managers executing their first deals. Data shows the majority of SPVs are small—more than two-thirds have less than $5 million in assets—and this segment includes most of the vehicles deployed by solo GPs before they raise their first institutional fund.

For aspiring fund managers, SPVs can be an effective way to build a track record before beginning fund formation for a larger, traditional fund. For example, High Circle Ventures used SPVs to execute several early deals, which helped it prove its investment thesis to LPs when it later launched its first fund. This approach allowed it to enter the market and begin building its portfolio without the overhead of a full fund structure.

Why private capital is attractive

Private capital holds distinct advantages for both the investors who fund it and the companies that receive it. These benefits are a primary driver of the asset class's continued growth and its increasing importance in the global economy.

For investors: The primary attractions are the potential for higher returns that are not directly correlated with public market volatility and the opportunity to invest in innovative companies before they become household names. As capital returns are picking up, recent data shows the median internal rate of return (IRR) for the 2017 VC fund vintage climbing to 13.5%, with a median net TVPI of 1.95x, underscoring the potential for strong performance in the asset class. This allows for portfolio diversification and access to growth that is not available in public equity markets.

For companies: The main benefit is access to patient, long-term capital from investment partners. This allows companies to focus on growth and execution without the short-term pressures of quarterly public reporting, enabling them to build more sustainable value over time.

What are the risks of private capital?

While attractive, private capital also comes with a unique set of risks and considerations that all participants must understand. The private nature of these investments creates challenges that differ from those in the public markets, turning high-touch investor relations into a manual and error-prone business function without modern tools.

As Holli Heiles Pandol, senior policy counsel at Carta, notes during the Navigating the Shifting VC Regulatory Landscape webinar, the environment is changing. "We're starting to see proposals and rules come out of the SEC that are imposing more of those public-like disclosure requirements on private markets," which increases the compliance burden on fund managers.

For LPs: The most fundamental risk is that investments may fail and capital may not be returned—private capital carries an inherently high risk of loss, as many companies never achieve the growth needed to generate positive returns. Beyond that, illiquidity means LP capital is locked up for many years with limited ability to sell; returns take longer to materialize than in public markets; and the limited transparency of private investments requires a high degree of trust in the GP's ability to manage the fund and report accurately.

For GPs: One of the most pressing risks is generating the returns needed to distribute capital back to LPs. In recent years, reduced IPO activity has created an exit liquidity challenge—with fewer pathways to take companies public, GPs have had fewer opportunities to realize gains and return capital to investors. This dynamic has contributed to the rise of secondary funds, which allow LPs to sell their fund interests before a traditional exit. Beyond return generation, GPs must navigate significant fiduciary responsibility, an evolving regulatory landscape, and the operational burden of managing a fund, its investments, and its investors.

Managing the private capital lifecycle from fundraising to wind-down

From a GP’s perspective, running a fund is not a series of disconnected tasks but a continuous process that requires a single, integrated operating system. The lifecycle of a fund spans many years, from its creation to its final investment exit.

This section walks through the chronological stages of a fund's lifecycle, highlighting the operational challenges at each step and how a unified platform provides the solution.

Fund formation and closing

The first stage is launching the fund, which involves fund formation, structuring the legal entities, drafting the necessary documents, and onboarding investors. This is often a slow, manual, and document-intensive process that can create friction for both the GP and their new LPs, with both fund managers and investors agreeing that paper-based subscriptions should be left in the past. A poor closing experience can damage an LP relationship before it even begins.

Modern solutions like Carta Fund Formations and Carta Closings digitize and streamline this work. By automating workflows and centralizing documents, they help ensure a professional and efficient experience for LPs from day one, setting a positive tone for the partnership.

Capital deployment and portfolio management

Capital deployment is the process of making a capital call to LPs to make investments into companies or assets. Once investments are made, the ongoing strategic work of portfolio management begins. This involves monitoring performance, making follow-on investments, and planning for future capital needs.

A common pain point for fund managers is relying on static, outdated spreadsheets for fund modeling and forecasting—tools that can no longer keep up with modern data and reporting demands. A dynamic tool like Carta Fund Forecasting provides scenario modeling capabilities, allowing fund managers to manage reserves and make data-driven decisions with confidence.

Reporting, distributions, and wind-down

The back office is defined by critical, recurring tasks like fund accounting, managing compliance, preparing for the annual audit, and calculating and sending fund distributions to investors. These processes are complex and leave no room for error, which is why modern platforms that enable smoother quarterly reporting and annual audits are key to maintaining LP trust.

For firms managing multiple funds and entities, having a single source of truth is essential. As Scott Holton, CFO of Next Frontier Capital, explains, using Carta as a "full back office tool" for all of Next Frontier’s funds, SPVs, and management entities provides the unified control needed to operate efficiently.

Carta Fund Management serves as a comprehensive solution that automates these workflows. Its event-based general ledger ensures accuracy, a dedicated Auditor Portal simplifies the audit process, and the LP Portal delivers the transparency and access that modern investors demand.

The evolution of fund operations: Then and now

The world of private capital has transformed dramatically. In the past, it was a smaller, relationship-driven industry where deals were managed on spreadsheets and back-office operations were largely manual. Fund administration was seen as a simple bookkeeping function, a necessary but low-value part of the process.

Today, the private markets are a major part of the global economy, with PE assets under management (AUM) continuing to grow and attract institutional-level capital despite macroeconomic headwinds. This evolution has professionalized the industry and dramatically increased the operational demands on fund managers. In this new era, fund administration is no longer just about recording transactions; it has become a strategic investment management function critical to a fund's success, impacting everything from investor confidence to regulatory compliance.

Building the operating system for private capital

Private capital is a dynamic and powerful force in the global economy, but its inherent complexity demands modern, institutional-grade infrastructure. To succeed in the modern private capital landscape, fund managers can no longer rely on a patchwork of disconnected systems. Thriving in this complex environment requires a single, integrated technology platform—an ERP for private capital. Carta's mission is to provide this infrastructure—a unified network that connects GPs, LPs, portfolio companies, and their employees on a single platform. A centralized operating system brings transparency, efficiency, and liquidity to the private markets.

This need for a unified system is a recurring theme among top-performing fund managers. As Brian Montgomery, CFO of private credit firm Legalist, explains, “Other admins build their own systems and they’re full of tiny errors... With Carta, if your inputs are correct, your outcomes are consistent.”

Ultimately, a strong operational foundation is a powerful competitive advantage. It enables firms to scale with confidence, maintain flawless compliance, and build lasting trust with their investors by delivering unparalleled accuracy and transparency.

To see how Carta’s platform can support your fund’s growth, request a demo.

Frequently asked questions about private capital

Who can invest in private capital?

Investment in private capital funds is generally limited to institutional investors and high-net-worth individuals who meet certain regulatory standards. These investors are often required to be either accredited investors—a status which can be met by individuals with a net worth over $1 million (excluding primary residence)—or qualified purchasers.

Why do investors allocate to private capital?

Investors are drawn to private capital for the potential to earn higher returns, to diversify their portfolios away from public markets, and to gain direct access to economic growth and innovation.

What’s the difference between private capital and alternative investments?

Alternative investments is a broad term for any asset class outside of traditional stocks and bonds, including hedge funds, commodities, and art. Private capital is a specific subset of alternatives focused on investing in non-public companies or assets.

What is the role of a fund administrator in private capital?

A fund administrator handles essential fund operations and back-office functions for a private fund, such as accounting, reporting, and compliance. This allows the GP to focus on making and managing investments.

What is the difference between private capital and private equity?

Private capital is the broad asset class of all investments not traded on public exchanges. PE is a specific investment strategy within that class focused on buying ownership in more mature companies.

What is the difference between private credit and private capital?

Private credit, also known as private debt, is a major strategy within the private capital asset class that involves lending money to companies. Other strategies, like PE, involve buying ownership instead of lending.

Is venture capital a form of private capital?

Yes, VC is a well-known form of private capital that specializes in providing funding to early-stage, high-growth startups. It is a subset of the broader PE asset class.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.